C3.ai stock has been flat so far this year, but the company is making notable strides in artificial intelligence.

When it comes to artificial intelligence (AI), smart investors know that there are many lucrative opportunities outside of big tech. One company emerging as a highly coveted name in the AI realm is C3.ai (AI 3.29%). Yet despite the company’s progress, its shares are basically flat through the first half of 2024.

Could now be a good time to pounce on an underappreciated AI opportunity?

How is C3.ai performing?

C3.ai develops a host of enterprise software solutions that it sells to both the public and private sectors. The company has an impressive roster of strategic partnerships with cloud network providers Alphabet, Amazon, and Microsoft. Moreover, C3.ai works closely with high-profile consulting company Accenture, as well as defense specialist Raytheon.

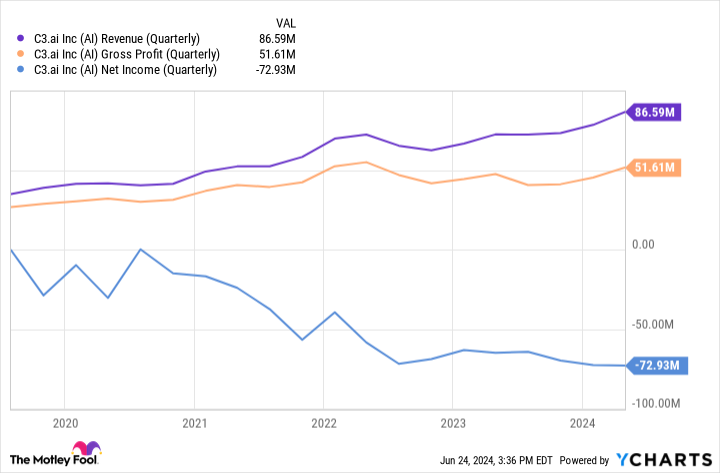

AI Revenue (Quarterly) data by YCharts.

The chart above illustrates some important financial metrics for C3.ai over the last several years. On the positive side, revenue is beginning to show some meaningful acceleration.

However, some issues come to light when looking at the company’s gross margin profile. For the fiscal year ended April 30, 2024, C3.ai reported gross margin of 57%. By comparison, the company’s gross margin was 68% for fiscal 2023.

Unsurprisingly, the deterioration in margin has contributed to mounting operating losses. Despite the company’s newfound revenue growth, these increases have come at a steep price.

What does the competitive landscape look like?

C3.ai competes with other AI enterprise software developers including Palantir (PLTR 4.65%), Databricks, and Alteryx. Palantir has an enormous presence in the federal landscape, working with many U.S. defense agencies and other government institutions.

Furthermore, as I expressed previously, Palantir’s recent alliance with Oracle could unlock even further growth across both the public and private sectors. On top of that, Palantir is consistently profitable. The company now has posted positive net income for six consecutive quarters.

This provides Palantir with a high degree of operating leverage and an enviable level of financial flexibility. The reason is the company is able to reinvest its profits back into the business and double down on research and development efforts, as well as customer acquisition strategies.

Moreover, Databricks is one of the most valuable start-ups in the world. With investor support from Microsoft, Nvidia, Salesforce, and more, Databricks is well-positioned to fend off competition in the AI and data analytics markets.

Image source: Getty Images

Is now a good time to buy C3.ai stock?

C3.ai is an interesting company to analyze. On the one hand, the company is demonstrating some real momentum and has proven that it can compete in the AI environment.

But on the other hand, the company’s growth is coming at a steep cost, and this dynamic doesn’t appear to be changing. While management is guiding for up to 27% annual revenue growth in its current fiscal year, it’s also forecasting operating losses of up to $125 million.

As long as C3.ai continues to burn cash, I’m hard-pressed to understand how the company can compete in the long run. Alternatively, competitors like Palantir are already consistently profitable, while Databricks has the luxury of strong institutional support from some of the tech sector’s largest constituents.

Right now, I’m sitting on the sidelines when it comes to investing in C3.ai. I think there are more opportunities in the AI realm with established players. While C3.ai is building a respectable business, growth investors have far better options.

A prudent approach could be to monitor C3.ai’s earnings calls and assess if the company is building a path to profitability and continuing to penetrate its target markets. Should this be the case, there’ll be ample opportunity to scoop up shares for investors with long-term horizons.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool has positions in and recommends Accenture Plc, Alphabet, Amazon, Microsoft, Nvidia, Palantir Technologies, and Salesforce. The Motley Fool recommends C3.ai and RTX and recommends the following options: long January 2025 $290 calls on Accenture Plc, long January 2026 $395 calls on Microsoft, short January 2025 $310 calls on Accenture Plc, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.