Palantir stock is trading near all-time highs.

Data analytics software company Palantir Technologies (PLTR -2.23%) has experienced a lot of ups and downs since going public in late 2020. Shortly after its IPO, Ark Invest CEO Cathie Wood frequently tuned into financial news programs touting Palantir’s potential. Unsurprisingly, the stock soared.

But this rise to the top of the software arena was short-lived. The next couple of years proved tough for Palantir, as enterprise software in general witnessed declining growth on the backdrop of a troubled economy. By the beginning of 2023, Palantir’s stock price was a mere $6.

However, the technology sector has witnessed a sharp bounce back over the last year and a half due to rising interest in artificial intelligence (AI). Palantir has been a beneficiary of AI tailwinds, and investors are rejuvenating the stock. Since Jan. 1, 2023, shares of Palantir have rocketed by 575%.

Below, I’ll dig into Palantir’s $43 share price and analyze if the stock is too expensive right now.

What is fueling Palantir’s stock price?

Considering Palantir stock has risen by such outsize magnitudes, it’s natural to wonder what catalysts are fueling the stock. Tying the stock action purely to demand for AI services is not enough of an explanation.

Here are five core ideas that I think are pushing Palantir stock to new highs.

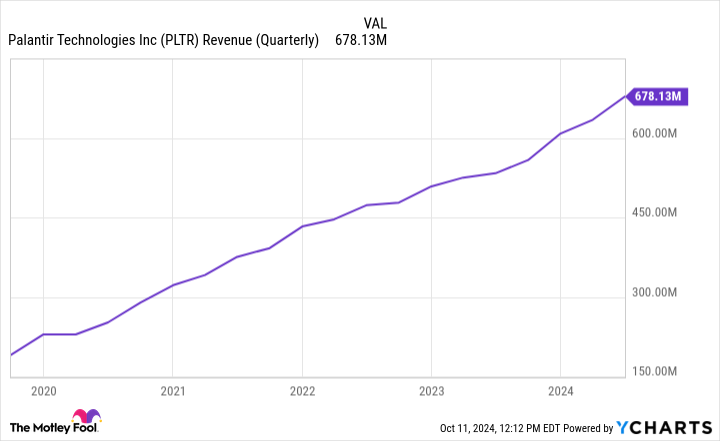

1. Revenue acceleration: The chart below illustrates Palantir’s quarterly revenue growth since going public. While the company’s top line has steadily risen, there are some notable time periods to call out.

Between 2021 and 2023, Palantir’s revenue managed to increase but in an inconsistent fashion. As the chart indicates, there are some noticeable periods of more protracted growth that left some investors questioning Palantir’s potential.

PLTR Revenue (Quarterly) data by YCharts

However, in early 2023 the slope of the revenue line began to steepen quite a bit. This is no coincidence. The company released its fourth major software suite, the Palantir Artificial Intelligence Platform (AIP), in April 2023. Since its release, Palantir’s growth has started accelerating again.

While AIP has been a success for Palantir so far, there’s more to the picture contributing to the company’s growth.

2. Use cases: For much of its history, Palantir relied mostly on government contracts — specifically with the U.S. military and adjacent agencies. The advent of AIP has changed this dynamic dramatically.

To help market the release of AIP, Palantir has hosted immersive seminars during which business leaders can demo the company’s products. The idea is for corporations to identify a use case leveraging Palantir’s AI software.

This approach has been a big hit so far. Over the last couple of years, Palantir has really diversified its business and is now growing significantly in the private sector.

Image source: Investor Relations.

3. Profitability: The combination of top-line acceleration and a successful penetration of commercial enterprises has led to wider operating margins and consistent profitability for Palantir.

By reaching consistent profitability, Palantir became eligible for inclusion in the S&P 500. The company officially began trading as a member of the S&P 500 in September, which I think is a nod supporting the company’s long-term outlook. In other words, if Palantir’s growth was only thanks to the AI boom then it likely would not have received inclusion in the index.

4. Institutional buying: Becoming a member of the S&P 500 is a respectable milestone. But I think the real tailwind of becoming part of the index will be the potential for more institutional investors to consider a position in Palantir.

5. Partnerships: The last idea I want to cover is Palantir’s relationship with big tech. Earlier this year, the company signed strategic partnerships with AI bigwigs Microsoft and Oracle. Moreover, the company continues to be a core player in the public sector — a particularly lucrative opportunity as AI becomes a more integral component of defense tech.

Image source: Getty Images.

What does the valuation suggest?

While all of the factors above suggest Palantir has a bright future, it’s imperative that investors take a hard look at the valuation fundamentals.

Right now, Palantir trades at a price-to-earnings (P/E) multiple of 256. Candidly, this is so high that it’s not really an appropriate measure. The bigger idea here is that even though Palantir is finally profitable, the company’s net income is still pretty small.

Although Palantir has several catalysts that could help expand its profits, I think it’s fair to say that the P/E ratio is disconnected from the current fundamentals of the business. Furthermore, even on a price-to-sales (P/S) basis Palantir’s valuation expansion cannot be denied when compared to other AI software-as-a-service (SaaS) peers.

PLTR PS Ratio data by YCharts

Is Palantir stock too expensive?

My honest opinion regarding Palantir is that the stock is a bit overbought at the moment. While I am a bull and currently own the stock myself, investors need to be careful buying into opportunities with outsize momentum.

A lot would need to go wrong for Palantir stock to go back to $6. But with that said, could a 20% sell-off happen? You bet.

At the end of the day, buying shares now or waiting for a more reasonable valuation is purely your preference. Above all else, keep in mind that trying to time the perfect moment to buy a stock is impractical.

Instead, you should be thinking about the long-term secular tailwinds fueling specific market themes and do your best to identify which companies will emerge as winners. To me, Palantir fits these criteria in terms of AI.

It’s important to remember that growth stocks carry outsize volatility, and no company is immune to macroeconomic forces. Although I still believe in Palantir, I think buying at this price requires the knowledge that you’re investing at a premium valuation. While that’s not a bad thing per se, investors need to be thinking long term with this opportunity.

Adam Spatacco has positions in Microsoft and Palantir Technologies. The Motley Fool has positions in and recommends Microsoft, Oracle, Palantir Technologies, ServiceNow, and Snowflake. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.