Being a leader in an industry is no guarantee of success.

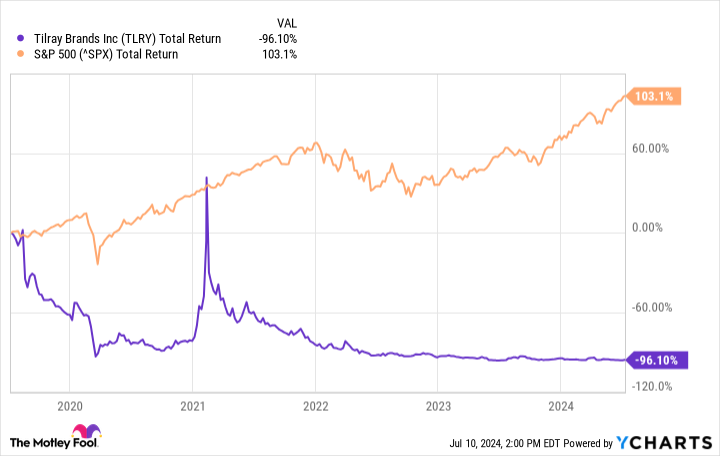

Sometimes, the next big thing ends up being not so big. Case in point: The cannabis industry grew in prominence after the substance was legalized in Canada in 2018. Some analysts expected it to lead to outsized returns for the industry leaders, perhaps making many millionaires of many investors in the process. Things haven’t turned out that way — quite the opposite. Cannabis stocks have turned in an abysmal showing during the past five years. Tilray Brands (TLRY 1.05%), one of the leaders in the field, hasn’t been an exception. But with improving financial results and exciting legal and regulatory developments, is now a good time to invest in the stock?

TLRY Total Return Level data by YCharts.

Tilray’s growth through acquisitions

Tilray’s revenue has been on an upward trajectory in the past half a decade.

TLRY Revenue (Quarterly) data by YCharts.

But there is more to the story. Much of the company’s growth came from buying out other cannabis players. It now stands as the leader in the Canadian market. As of the end of its fiscal 2024 third quarter, which concluded on Feb. 29, Tilray had the top market share in the country, standing at 11.6%. The company was also the leader in Germany. There is nothing wrong with growing through acquisitions. But Tilray’s impressive-looking, top-line trajectory obscures the fact that organic-sales growth hasn’t been impressive, and the Canadian market has been an unprofitable mess.

Tilray, like other players in the field, has had to deal with a challenging regulatory landscape and stiff competition from illegal channels. Can Tilray get around these challenges? The company is attempting to do so by diversifying. Its business also includes a pharmaceutical unit, an alcoholic-beverages segment, and a hemp-focused wellness segment. Tilray’s higher-margin beverage segment looks particularly exciting. Thanks (again) to acquisitions, it is now the fifth-largest craft brewer in the U.S. Beyond the sale of the drinks it offers, Tilray likely hopes that cannabis legalization in the U.S. at the federal level will open up a world of opportunities in the cannabis-beverages market.

Tilray will be better positioned to take care of this opportunity if it comes to pass.

Will a better regulatory landscape help?

Things are changing for cannabis companies. In the U.S., marijuana seems close to being rescheduled from a Schedule I substance to a Schedule III. Drugs in the latter category are considered less dangerous, less prone to dependence and abuse, and have at least some accepted medical uses. If it goes through, this change would make it much easier for Tilray and its peers to operate in the U.S. But that’s not all. Germany legalized limited recreational uses of cannabis earlier this year, opening up a $3 billion medical-cannabis opportunity, according to Tilray.

Will these moves help the company bounce back, register strong organic financial results, and deliver outsized returns? My view is that Tilray’s prospects remain dim. Let’s assume that cannabis isn’t just rescheduled but legalized in the U.S., which would be even better. The Canadian experience has shown that legalization is by no means a guarantee that companies will suddenly start performing well. If anything, the market will attract dozens of new players, competition will heat up, and many consumers who have been obtaining the substance illegally for years will continue doing so.

It’s not clear that Tilray will perform well in this environment. Though Germany’s new laws are a step in the right direction for Tilray, there is a long list of rules consumers will have to abide by. For instance, those who want to obtain cannabis legally in the country will have to grow it themselves or join cannabis clubs. These clubs (and it’s not legal to join more than one) aren’t stores that sell weed. They grow and share it among the club’s members. Many more rules will make it challenging for consumers, many of whom will likely continue to do what they have been doing for years.

Again, it’s not clear whether these developments will benefit Tilray. With unclear prospects, a challenging market, and a poor track record of results, Tilray isn’t worth the trouble.