Earnings momentum strategies are a risky way of navigating the upcoming corporate earnings season, which begins in mid-January.

I’m referring to strategies that favor the stocks of companies whose earnings growth is accelerating. According to theory as well as history, shares of such companies should outperform those with declining growth rates.

A perfect recent example is Tesla TSLA, +7.84%. Its earnings have been growing for several quarters now: From a loss in 2019 to profit of 25 cents a share, 44 cents a share, and 76 cents a share, respectively, in the first three quarters of last year. For the fourth quarter of 2020, which Telsa is slated to report on Feb. 3, FactSet reports that the consensus of Wall Street analysts is that the company will report EPS of 96 cents.

I need not remind you that Tesla’s stock price has shot up in concert with its earnings, with a trailing 12-month gain of more than 737% (according to FactSet).

There are two major reasons why I nevertheless caution against relying on earnings momentum strategies for picking which stocks to buy or sell in the upcoming earnings season.

The market reacts almost instantly to earnings surprises

The first is practical: Wall Street reacts almost instantly to earnings surprises. By instantly I mean a matter of seconds. By the time you or I read about unexpectedly good earnings, it will almost certainly be too late to profit from the news.

Imagine, for example, if Tesla reports a quarterly EPS in its Feb. 3 earnings report that is much higher than the current consensus of $0.96. You can bet that the stock will rally almost instantaneously. That rally would largely discount any remaining upside potential that earnings momentum strategies used to be able to exploit.

This is what efficient market theorists tell us is inevitable with any strategy that has shown great historical promise. As more and more investors pile into a strategy, they kill the goose that lays the golden egg.

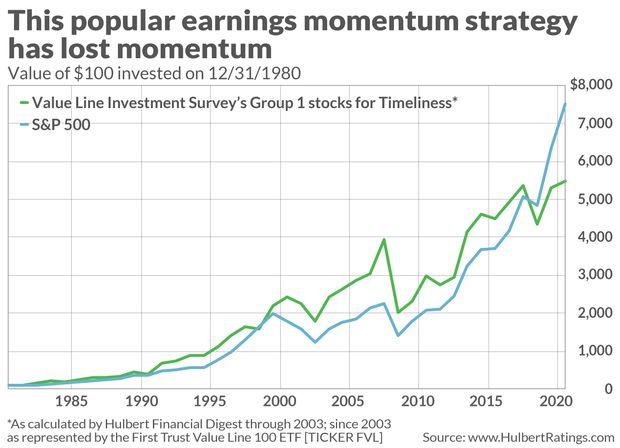

This helps to explain the deteriorating performance of what used to be the newsletter industry’s most successful earnings momentum strategy. I’m referring to the stock ranking system published by the Value Line Investment Survey. Each week, the newsletter reports the 100 stocks (out of a universe of 1,700 widely-followed issues) that have the greatest appreciation potential over the coming year. Though the newsletter’s ranking system is proprietary, we do know that it is based largely on earnings surprise.

As you can see from the chart below, a portfolio of these 100 favored stocks from Value Line beat the S&P 500 SPX, +0.55% by a wide margin over the period from 1980 through the early part of this century, but has lagged ever since. (Full disclosure: Value Line is not one of the newsletter publishers that contracts with my performance-monitoring firm to audit its returns.)

Value might be on the verge of outperforming growth

Another reason not to rely on earnings momentum strategies is that momentum strategies typically perform poorly when, as some are forecasting will take place in 2021, value stocks outperform growth stocks.

The negative correlation between value and momentum was documented a number of years ago in research published in the Journal of Finance. Last year was a case in point: Growth trounced value and, sure enough, momentum performed well: The iShares MSCI USA Momentum Factor ETF MTUM, +1.65% beat the S&P 500 by 10 percentage points.

Contrast that with what happened in 2016, the last year in which value did really well relative to growth. In that year the USA Momentum Factor ETF lagged the S&P 500 by 7 percentage points.

To be sure, there’s no guarantee that value will outperform growth this year. There have been similar predictions of value’s resurgence in each year since 2016, and so far they have not come to pass. But value typically beats growth when the economy emerges from periods of economic weakness, and many now the economy will blast off this year as the pandemic is largely put behind us.

In fact, according to fund flow data for the month of December, there is evidence that this rotation into value from growth may have already started.

The bottom line: Be my guest if you want to bet on which companies will beat the Wall Street consensus in their upcoming earnings reports. You’ll turn a quick profit if you’re right. But not if you wait until those earnings are actually reported.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: How to make money in 2021 — follow these three stock market takeaways from last year

Also read: Why focusing on short-term results can short-circuit your investments and financial advice