Given the choice between an exchange-traded fund and an open-end mutual fund that are otherwise identical, which would you choose? If you’re like most investors, you’d choose the ETF. But I’m not so sure that’s the best choice.

This debate is not new, of course. The reason to revisit it now is that Dimensional Fund Advisors (DFA) earlier this month converted a number of its mutual funds into ETFs. For years the firm eschewed ETFs in favor of open-end mutual funds that were available only through a select group of financial planners, sometimes with high initial investment minimums and minimum holding periods.

ETFs, in contrast, enjoy many advantages over traditional mutual funds. They are more tax efficient, can be bought or sold at any time during the trading session, have no investment minimums other than the price of one share, have no minimum holding periods and can be sold short.

Given these considerable advantages, it’s little surprise that the ETF industry has mushroomed in size over the past couple of decades. DFA, whose funds collectively in 2020 suffered net redemptions, was undoubtedly feeling the pressure to extend diplomatic recognition to the ETF arena. Lawrence Tint, the former U.S. CEO of BGI, the organization that created iShares (now part of BlackRock), said in an interview that he has little doubt that this business motive played a big role in DFA’s decision.

Double-edged sword

Some of ETFs’ theoretical advantages are a double-edged sword, however. The unlimited ability to trade encourages self-destructive behaviors on the part of many short-term traders, for example. The resultant costs can outweigh ETFs’ other benefits.

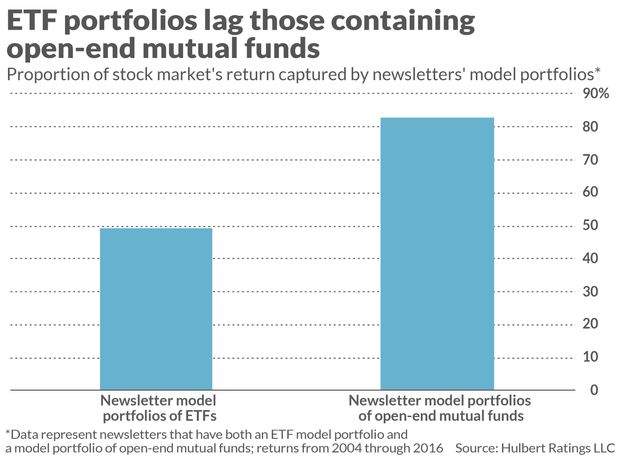

That certainly appears to be the case among many investment newsletters. Consider the results of a study the Hulbert Financial Digest conducted several years ago of 15 newsletters that at any point between 2004 and 2016 simultaneously maintained two separate model portfolios — one containing only open-end mutual funds and the other containing only ETFs. Any difference in these portfolios’ returns should be a function of the type of fund, since each pair of portfolios would have been informed by the same market-timing judgments, industry and sector bets, and so forth.

The results appear in the chart below. Because not all portfolios were tracked over the entire period, the chart averages their returns relative to that of the overall market. The average ETF model portfolio captured about half of the market’s annualized return, while the average open-end mutual fund portfolio captured 83%. That’s significant, equivalent to a several percentage point difference in annualized return.

Some academic studies have reached similar findings. One that appeared in Oxford University’s Review of Finance in 2017 is entitled “Abusing ETFs.” Upon analyzing the trades made by close to 8,000 clients of a German discount brokerage firm, the authors found that those who introduced ETFs into their portfolios had lower returns than those who did not.

Transaction costs

For additional thoughts about DFA’s decision to convert some of its funds into ETFs, I reached out to Ken French, a Dartmouth College finance professor whose academic work (with Eugene Fama of the University of Chicago) is the theoretical foundation of DFA’s mutual funds. French also is a member of DFA’s board of directors.

French pointed out that one significant benefit of DFA’s conversion to ETFs is that it imposes on the trader the bulk of the transaction costs associated with trading. This was not the case previously with DFA’s open-end mutual funds, for which transaction costs were partially borne by all investors in that fund, including long-term, buy-and-hold investors. That’s not fair, he argued.

While acknowledging that ETFs might encourage self-destructive behaviors, French says he nevertheless takes a libertarian approach: so long as a self-destructive investor doesn’t harm anyone else, it’s inappropriate to try to prevent that behavior.

But that doesn’t mean you should ignore the potential for you personally to engage in self-destructive investing behaviors. ETFs undeniably have great advantages — in theory. But you must be disciplined in order not to fritter away that theoretical advantage. Just because you can trade ETFs at any time doesn’t mean you should.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: Here’s how the rise of the retail investor is powering some ETF moves

Also read: ‘Meme’ stock-market trend around AMC, GameStop may be more persistent than you think, says report