It takes guts to be a value investor these days. But the top-performing investment newsletters have no shortage of courage. By value, I’m referring to stocks that are out of favor, trading for relatively low ratios of price-to-earnings, book value, sales, and so forth. Value’s opposite is growth: Stocks in this latter category typically trade for high valuation ratios.

I’m not kidding when I say that value investing takes guts. According to a recent analysis from Research Affiliates, value has lagged growth now for more than 13 years — the longest stretch in recorded U.S. market history. This has led to a seemingly-endless series of pronouncements in recent years that value investing is dead.

Read: What’s happened to value stocks?

Try telling that to the top performing investment newsletters tracked by my Hulbert Financial Digest performance-auditing firm. These four stocks are tied for being the most recommended right now by those newsletters:

• Walt Disney DIS, -2.10%

• FedEx FDX, -0.33%

• IBM IBM, -1.17%

• JPMorgan Chase JPM, -1.32%

Notice the absence of any of the so-called FAANG stocks that have been leading the market in recent weeks.

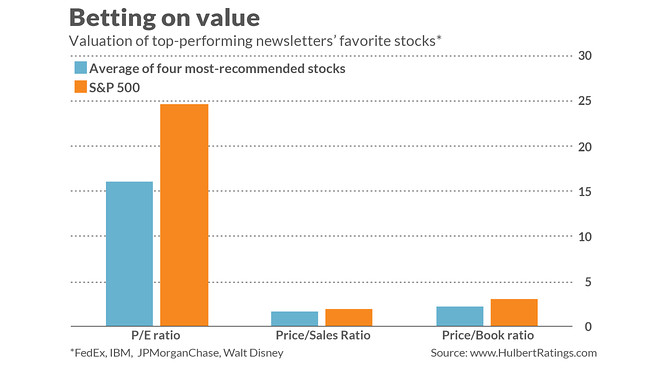

All four of these stocks are instead solidly in the “value” category: Their average trailing 12-month PE ratio, for example, is 35% lower than the S&P 500’s SPX, -0.63% . Their average price/book ratio is 26% lower, and their average price/sales ratio is 10% lower. (See chart below.) And given their status as value stocks, it is not a surprise that they have been lagging of late.

The newsletters recommending these four stocks have excellent long-term performance. I calculate that, over the last 20 years (through April 2020) they have outperformed the S&P 500 by 3.2 percentage points annualized. (These figures take dividends and transaction costs into account.)

“ A chance to buy good-quality stocks at a discount. ”

The newsletters’ rationales for buying these stocks are the same in all cases: Despite shorter-term disruptions because of the coronavirus pandemic, each of the four companies have excellent long-term prospects. Their current struggles give investors a chance to buy good-quality stocks at a discount.

This is, and always has been, the classic refrain of the value investor, of course. Is there reason to believe that the newsletters’ faith in these stocks will be rewarded, even though value has lagged for the last 13+ years? Yes, and one reason is these newsletters’ excellent long-term records.

Another is what was found by the Research Affiliates study mentioned above, which was authored by Rob Arnott, the firm’s founder; Campbell Harvey, a finance professor at Duke University; Vitali Kalesnik, a senior member of Research Affiliates’ investment team, and Juhani Linnainmaa, a finance professor at Dartmouth College. They subjected to statistical scrutiny all the explanations they were aware of for why value has lagged growth for so long, including:

- The value effect never really existed in the first place, and evidence to the contrary was the result of data mining;

- The economy has changed in fundamental ways making the value factor irrelevant going forward, such as technological innovation, low interest rates, and the growth of private equity;

- Too many investors tried to follow the value factor, thereby discounting away what would have been its outperformance over growth;

- Investors have shown a preference for growth stocks, thereby making them more expensive and value stocks cheaper than ever;

- Intangibles that are not counted as part of book value have become increasingly important to a company’s profitability;

- Bad luck.

It’s beyond the scope of this column to review the statistical tests that the authors used in analyzing each of these explanations, but you should read their report if interested. They rejected those hypotheses that would imply that value is permanently dead and concluded instead that “the stage is set for potentially historic outperformance of value relative to growth over the coming decade.”

If so, the top-performing investment newsletters will have every right to say “I told you so.”

(Full disclosure: All the newsletters tracked by my performance tracking firm pay a flat fee to have their returns audited. Note that because all newsletters pay the same fee, my firm had no incentive to report that services recommending value stocks had better long-term performance than those that are recommending growth stocks.)

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: Dud stock picks, bad industry bets, vast underperformance — it’s the end of the Warren Buffett era

Plus: Warren Buffett hasn’t lost his touch and Berkshire Hathaway’s critics — as usual — are short-sighted