Predicting when the next bear market will occur is notoriously difficult. Just ask stock-market timers. But what about predicting the severity of the next bear market?

That has become a pressing question of late, since Wall Street has shifted from whether a U.S. recession will occur in the next 12-18 months to when. A bear market for stocks is almost certain to accompany an economic downturn. By one measure, the Dow Jones Industrial Average DJIA, -0.07% would suffer a particularly steep decline.

To find out whether a bear market’s severity can be forecasted, I analyzed all bear markets since 1900 (according to a bear market calendar maintained by Ned Davis Research, the quantitative research firm). U.S. stock investors have experienced a total of 36 bear markets since then, by their count.

The first hypothesis I tested is that a bear market’s severity is a function of the prior bull market’s length. Some have worried that this might be the case, since many assume that the current bull market is the longest in U.S. market history.

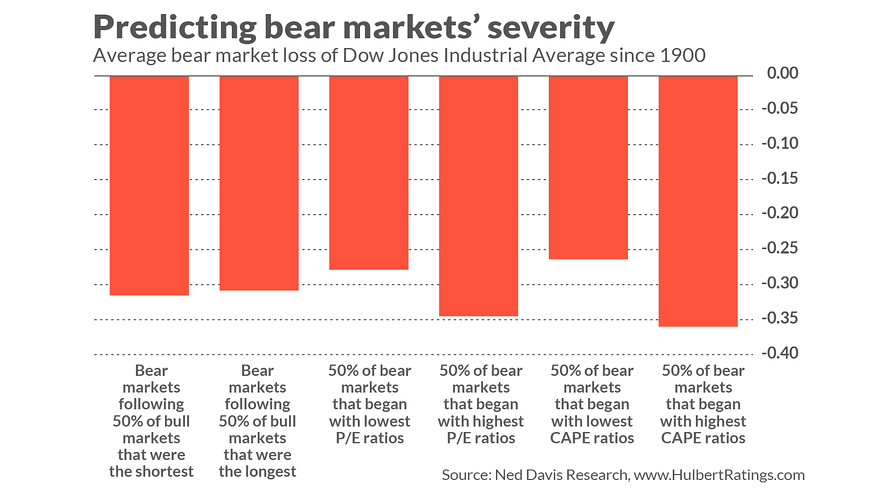

Fortunately, there is no correlation between bull-market length and subsequent bear-market severity, as you can see from the chart below. Consider first those bear markets that followed the 50% of bull markets that were the shortest: In those bear markets, the Dow fell by an average 31.5%. Following the 50% of bull markets that were the longest, in contrast, the Dow lost a nearly identical average of 30.8%. Other tests of this hypothesis reached similar results.

Somewhat more promising is the price/earnings ratio. Specifically, I tested the hypothesis that a bear market’s severity is correlated with the overall market’s P/E ratio at the start of that bear market. As before, I divided the 36 bear markets since 1900 into two equal-sized groups: One contained those for which the P/E ratio was lowest when they began, and the other containing those with the highest ratios.

The chart shows that the Dow’s average loss in the first group of bear markets was 27.8%, versus an average loss of 34.5% for the second group of bear markets. Unfortunately, given the relatively small sample size and the variability in the data, this difference is not significant at the 95% confidence level that statisticians often use when determining whether a pattern is real.

What about the Cyclically-Adjusted P/E ratio (or CAPE) that was made famous by Yale University finance professor (and Nobel laureate) Robert Shiller? It did somewhat better still than the traditional P/E ratio, as the chart also shows. Yet even for the CAPE ratio we cannot conclude, at the 95% confidence level, that the pattern is genuine. Other statistical tests reach similar results.

Read: Stock bulls are telling themselves a lot of lies about this market

Whether you take this last result as good or bad news depends on your perspective. On the one hand, given that the CAPE currently is extremely high (30.2, versus an average of 15.8 since 1871), you might be relieved that this does not guarantee — in a statistical sense — that the next bear market will be especially severe.

On the other hand, there’s a historical tendency for bear markets to be more severe when they begin from higher CAPE levels. Just because something is not significant at the 95% confidence level doesn’t mean it has no significance whatsoever. Our best guess, given the limited data, is that bear markets are more severe when they begin from higher CAPE levels.

How severe? A simple econometric model whose inputs are past bear markets and CAPE values predicts that, if a bear market were to begin from current levels, the Dow would tumble 35.3% Though that’s less severe than the 2007-2009 bear market, it still would sink the Dow below 17,000. Bulls take note.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

Read: Small-cap stocks are flashing a caution signal

More: Why international stocks just can’t compete with the U.S. market right now