U.S. consumers might have their pick of employment in today’s robust job market, but that doesn’t mean everyone is getting financed for a car.

A Federal Reserve Bank of New York survey of consumer credit released Monday showed a spike in the rate of auto-loan rejections, to 8.1% in October from 4.5% in the same month last year.

And for the full year, the average rate of car-loan rejections was 7.1%, up from 6.1% for 2018, even through applicants reported fewer denials in other parts of the record $14 trillion consumer debt market for the same 12-month period.

“The reported rejection rates for credit cards, mortgages and mortgage refinancing applications all declined compared to 2018,” according to the Fed’s snapshot of its annual survey, which covers consumer experiences when applying for auto loans, credit cards, credit-card balance increases, mortgages and mortgage refinancing.

November saw a surprise dip in the U.S. unemployment rate, to 3.5% from 3.6%, matching a 50-year low and fueling optimism that a strong American consumer can help keep the economy chugging along beyond its record 11th year of expansion.

Still, a decade of easy auto credit has fueled concerns that U.S. households could be on the verge of yet another financing bubble, only a few years after many borrowers emerged from the worst foreclosure crisis since the Great Depression.

Last month, a report from the Wall Street Journal highlighted how one 40-year-old electrician took out a $45,000 loan on a $27,000 Jeep Cherokee, while other lenders also have been loosening their underwriting standards.

But while consumer debt grew 4.8% in October versus a year earlier, analysts at BofA Global Research see a more stable picture forming next year.

“We believe consumer debt will continue to grow but the pace will continue to moderate, with expectations for slower growth in consumer spending (+2.3% YoY in 2020) and relatively stable lending standards,” wrote a team of analysts, led by Chris Flanagan, in a weekly note to clients.

That comes in contrast to the U.S. housing market, where Moody’s recently said it expects competition among lenders to result in slipping standards for home buyers with spotty credit.

Check out: Lending standards to slide for homeowners with spotty credit, Moody’s warns in 2020 outlook

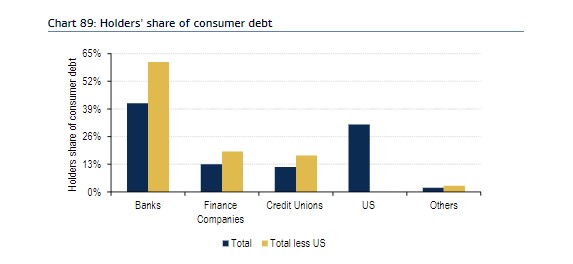

In the run-up to the 2008 financial crisis, toxic subprime mortgages were bundled by banks into mortgage-bond deals and sold to investors without government backing.

But this chart from BofA Global Research shows that the U.S. government and banks are the biggest holders of consumer debt in this credit cycle:

BofA Global Research

BofA Global Research