Surging mortgage rates and sky-high home prices have splashed cold water on the roaring U.S. housing market.

Yet a big question still facing investors, lenders and anyone trying to navigate the still-hot housing market is whether the Federal Reserve will start selling its trove of mortgage holdings to fortify its inflation fight. The central bank is so far trying to counter inflation by more traditional means: raising benchmark interest rates.

No doubt, housing data has been volatile recently, skewed by evolving Fed policy and a dearth of homes to buy. But with 20% annual home price gains, the central bank must weigh concerns about a potentially dangerous bubble forming in housing.

“If they really want to sound like they are committed to price stability, selling MBS could be something to explore,” said Priya Misra, head of global rates strategy at TD Securities, by phone, about the Fed’s $2.7 trillion holdings of mortgage-backed securities.

“But I don’t think they will,” she added.

Instead, Misra expects the Fed to first use higher rates and a smaller balance sheet to keep a lid on the housing market, avoiding a potential bubble burst, specifically by more aggressively raising its policy rate from its current range of 1.50%-1.75%.

“We expect that inflation slows later this year, and the economy, too,” Misra said. “If they are getting the Fed funds rate to 4%, and inflation’s not slowing, then they will talk about using other tools. Not before that.”

Funds flee housing debt

The Fed jolted the housing market in early June by firing off its biggest rate hike since 1994, in a bid to pull inflation back from a four-decade high.

It also began shrinking its nearly $9 trillion balance sheet, not through outright sales, but by letting assets mature and roll off the books.

Selling its mortgage assets into the market, however, could be a tricky next step.

The Fed roughly owns about 32% of the nearly $8.4 trillion agency mortgage-backed securities market, a key artery of housing finance. The sector has come under sharp pressure this year as the central bank raised rates and talked about pulling back its supportive policies.

Like other parts of fixed-income, performance in the mortgage sector has been hit hard, with the Bloomberg U.S. MBS (30-year) index pegged at a negative 9.8% total return on the year to date, according to FactSet data.

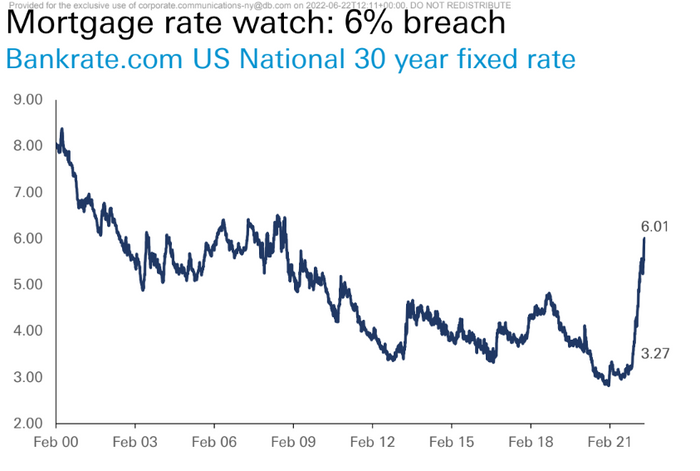

A similar story has unfolded for bond funds and exchange-traded funds tied to home finance, particularly as the 30-year mortgage rate recently topped 6%, before slightly pulling back.

30-year mortgage rates top 6%

Deutsche Bank

What’s more, outflows from mortgage-backed funds have neared the $20 billion mark this year, according to EPFR data, signaling a desire among many investors to avoid further carnage.

‘60% probability’

In Capitol Hill testimony this week, Federal Reserve Chair Jerome Powell was asked if the central bank would consider selling its mortgage holdings at a loss by Republican Sen. Bill Hagerty, who estimated the Fed’s current loss exposure at roughly $500 billion.

Powell said potential losses have played no role in the decision-making, and that they are not a consideration now.

On the other hand, higher rates have slowed refinancing activity, meaning old mortgages in existing bond deals could be slower to repay, a dynamic that Citi Research analysts led by Ankur Mehta said may slow the Fed’s balance-sheet runoff plans, and prompt the sales Powell was pressed on.

“We would assign a 60% probability to the Fed selling in Q4’22/Q1’23, a 10% probability of the Fed selling after that and a 30% probability to them never selling MBS,” the team wrote, in a Friday note.

‘Dire affordability’

Fed Gov. Michelle Bowman on Thursday said she supports another 3/4-point rate hike in July, and eventually wants the central bank to stop intervening in the U.S. housing market.

BofA analysts, however, pointed to the Fed potentially “worsening already dire home affordability” and it having “less experience using its balance sheet as a tightening mechanism than, say, rate hikes.” It’s these factors that raise doubts for any outright MBS sales by the Fed, at least for now, the analysts said in a recent client note.

Given the backdrop, Alex Pelle, U.S. economist at Mizuho, said it is a tough environment for the Fed to consider selling its mortgage bond holdings.

“Could it be a 2023 issue? Sure,” Pelle told MarketWatch. “However, the mortgage market is already experiencing significant adjustment. It would be an error for them to lean into that in the immediate future.”