What started out as a lump of coal turned into a gift for bullish investors: a record for the S&P 500 index to end the week before the Christmas holiday.

But if you’ve got this market figured out, you’re among the few.

On Monday, the scene on Wall Street may have felt to many investors much like how former UFC champion Tyron Woodley’s week ended last Saturday in his contest against the YouTube-star-turned-prizefighter Jake Paul:

In Wall Street’s case, the omicron variant of the coronavirus, and a host of other worries, including looming monetary-policy tightening by the Federal Reserve, subbed in for Paul’s devastating sixth-round overhand blow, leveling the Dow Jones Industrial Average DJIA, +0.55%, the Nasdaq Composite Index COMP, +0.85% and the S&P 500 SPX, +0.62% in a bruising session last Monday to start the holiday-abbreviated week. U.S. markets were closed on Friday in observance of Christmas.

However, this is how some investors may feel the week ended, with spectacular aplomb shown by a stock market that had so recently seemed destined to be chopped down to size in the final few weeks of 2021.

On Thursday, the S&P 500 index booked its 68th record close of 2021, finishing the week up 3.6%, while the Dow Jones Industrial Average booked a 4.4% gain and the Nasdaq Composite registered a more quotidian 0.7% gain after sinking more than halfway toward correction level at its lowest point during the volatile trading stretch.

Data analysts at Dow Jones observed that the capping of Monday’s fall by an end-of-the-week record for S&P 500 also occurred on July 19 when the index fell 1.9% only to end the week at a record high.

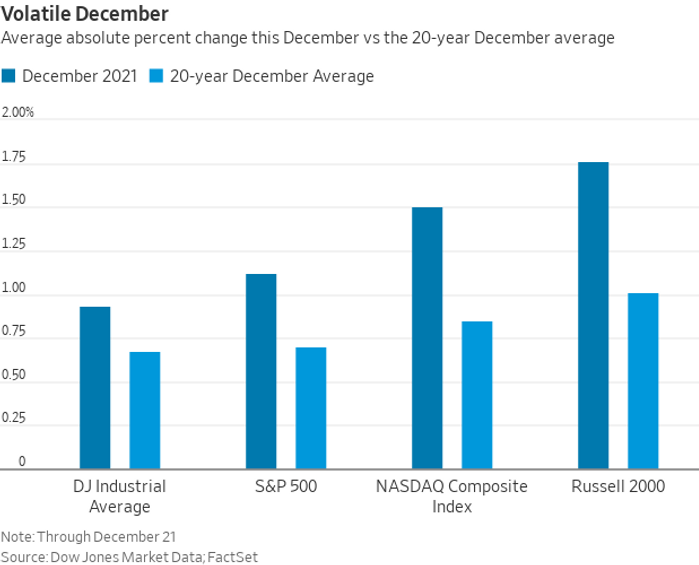

More broadly, the volatility this December so far has been stomach-churning. It’s been the choppiest since 2018, the last time interest-rate increases were on the table at the Federal Reserve.

And the so-called Santa Claus rally, a seasonally bullish period in the last five trading sessions of a year and the first two in the new year, is yet to commence. That’s if Santa deigns to dole out any additional gifts at all after the scintillation of the past three sessions.

The analysts at Leuthold Group write that, since 1972, the Santa Claus rally has produced an S&P 500 average gain of 1.26%, which is “60 basis points below the average for Santa Claus rallies from 1928 to 1972.”

Ryan Detrick, chief market strategist for LPL Financial, confirmed that there is an overwhelming tendency for the market to rally during that period, though it isn’t clear what to attribute the bullish uptrend to, other than Old St. Nick himself.

But we didn’t come here to marvel at the Santa Claus rally but rather the indefatigability of this market.

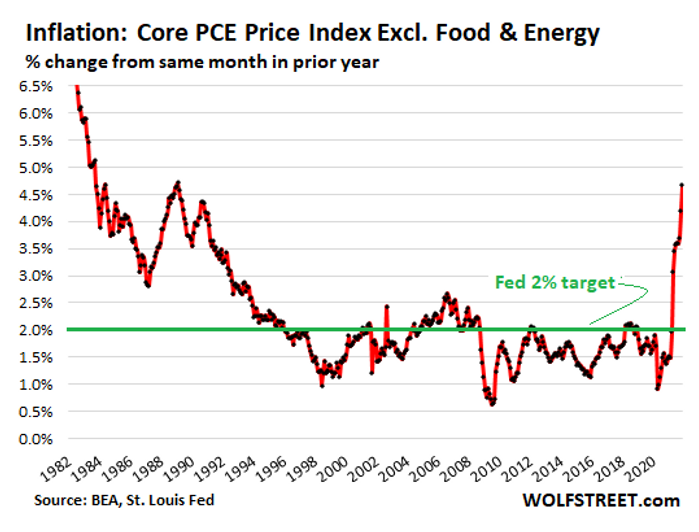

Nothing has changed about the market dynamic besides investors’ ability to fade negative headlines, including those centered on omicron and the outlook for inflation in years to come. On Thursday, data showed that the 12-month increase in the U.S. PCE index, the Federal Reserve’s preferred inflation gauge, had jumped to 5.7% in November from 5% in the prior month. That’s the highest rate since 1982.

Wolf Richter of the popular financial blog Wolf Street sounded as befuddled as many have been about policy from the Federal Reserve in a recent column.

Inflation is shooting higher even as this Fed is still repressing short-term interest rates to near 0% and is still printing money hand over fist, though less than it did two months ago. And the Fed has finally backed off its ridiculous claims that this inflation, caused by enormous historic amounts of money printing and interest rate repression, is just temporary and due to bottlenecks and supply chains.

The Fed announced in mid-December that it is cutting back on its bond buying at a faster clip, and projections from members of the central bank’s policy-setting panel of late point to three interest-rate increases in 2022. That move was meant to deflate some of the market’s bullishness, but investors continue to read the Fed’s hawkish policy pivot as dovish.

Rex Nutting: The Fed’s big surprise: All those inflation doves have suddenly become hawks

Market Extra: Why hawkish Fed moves to calm inflation aren’t likely to cause a sudden drain of liquidity from markets

Are fears about the spread of the omicron variant of the coronavirus causing the disease COVID-19 unwarranted because vaccines and remedies can handle it? Are people just too fatigued to consider the impact of lockdowns and mobility restrictions? Has inflation peaked, or is it already priced into stocks and bonds? Who knows?

Breaking news: U.K. data support view that omicron causes fewer hospitalizations, but also shows boosters wane

Jeremy Siegel, a noted professor of finance at the University of Pennsylvania’s Wharton School of Business, told CNBC on Thursday that he envisioned the Fed raising rates around eight times from its current range of between 0% and 0.25% for benchmark rates.

“Believe it or not, we have to get to 2% on fed funds,” Siegel speculated in conversation with the business news channel. The Wharton professor still saw the possibility of stocks booking low double-digit gains, even if the Fed needs to be more aggressive.

“Stocks are still the place to be,” Siegel said. He said that a rotation in value is what he’s betting will play out in 2022 as investors position for higher borrowing costs against a backdrop of richly priced large-cap and growth-oriented investments.

Sign up for our Market Watch Newsletters here.

What’s ahead for New Year’s week?

Monday

No U.S. economic data expected.

Tuesday

- S&P Case-Shiller U.S. home-price index for October at 9 a.m. ET

Wednesday

- International trade in goods, advance report for November at 8:30 a.m. ET

- Pending home sales index for November at 10 a.m.

Thursday

- Initial jobless benefit claims for the week ended Dec. 25 at 8:30 a.m.

- Chicago PMI for December 9:45 a.m.

Friday

- No government data scheduled in New Year’s Day observation

- U.S. stock markets operate under regular hours

- U.S. bond market closes early at 2 p.m. ET