The stock-market narrative over the last week centered on the escalating trade battle between the U.S. and China, but it’s the U.S. consumer that will steer the path ahead for equities.

As corporate tax-cut stimulus fades and the market continues to digest higher interest rates imposed last year, persistent job growth and wage gains are key to sustaining the current market rally, and pushing the S&P 500 SPX, +0.37% and Nasdaq Composite Index COMP, +0.08% above all-time highs notched in April, investors and strategists said.

“The consumer is really healthy and that’s key to the U.S. economy,” Aaron Clark, portfolio manager at GW&K Investment Management told MarketWatch. “There’s strong job growth, wealth creation with stocks and real estate, and broad-based wage strength, making this one of the better environments for the consumer in a long time.”

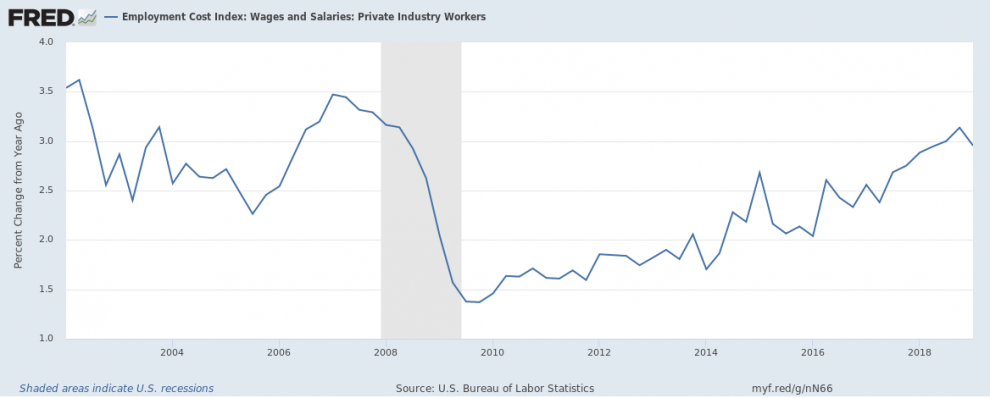

Over the past three months, the U.S. economy created 169,000 jobs a month, on average. While that number has trended down since January, it is still high enough to put downward pressure on the unemployment rate, and theoretically keep wage growth trending higher.

Federal Reserve Bank of St. Louis

Federal Reserve Bank of St. Louis

Clark argued that the recent trend of healthy, but not inflationary, wage growth is one of the best reasons to be bullish about the stock market, given that consumption accounts for more than two-thirds of U.S. GDP.

He also pointed to recent earnings results, including Mastercard Inc. MA, +0.86% which saw its U.S. gross dollar volume charges rise by 8% in the first quarter compared with the year-ago period, suggesting a strong U.S. consumer ready to borrow and spend. Other consumer-facing firms that saw better-than-expected domestic sales growth in the first quarter include Starbucks Inc. SBUX, +0.67% and McDonald’s Corp. MCD, +1.14%

Mike Loewengart, vice president of investment strategy at E-Trade agreed that rising wage growth is a key for the U.S. equities, but he cautioned that the trend is well below levels one would expect given the low unemployment rate. Meanwhile, he pointed out that retail sales growth has been surprisingly weak since December, despite the bounceback in March.

“There are a lot of positives right now for consumers, but we don’t have a clear picture,” Loewengart told MarketWatch, given subdued retail sales and that consumer confidence levels, while still high, have come down from last year’s levels.

“Consumer confidence is not exactly on an upward trend, it just seems to me that people are cautious,” he added. “The numbers are ok, but many consumers are apprehensive and that’s coming through in the consumer spending figures [in the latest GDP report], which were not encouraging. There’s no clear picture on that front.”

Meanwhile, an escalating trade fight, which has so far left the American shoppers largely unscathed, could start to crimp spending as the effects of Friday’s tariff hike begins to make its way through the economy, and especially if President Trump follows through on threats to drastically widen the number of products that will face a 25% import duty in the coming weeks.

Read: Here’s how hard the escalating tariff fight will hit the economy

Atlanta Fed President Raphael Bostic said Friday the central bank might have to cut interest rates if consumer spending suffers as a result of tariffs, potentially creating a counterweight to the effects of the trade skirmish.

Stocks ended on a positive note Friday, clawing back losses to finish in positive territory after upbeat comments surrounding trade talks. But it wasn’t enough to prevent the S&P 500 and the Nasdaq Composite from posting their biggest weekly declines of 2019, with the S&P off 2.2% and the Nasdaq off 3%. The Dow recorded a 2.1% weekly fall, its biggest since early March.

The week ahead will provide investors a series of reports that could be clarifying. On Monday, the Federal Reserve will release its quarterly survey of consumer expectations. On Wednesday the all-important retail sales report for April will be released, which could give investors a clue as to whether the slump that began in December was a temporary blip or the beginning of a worrisome trend.

On Thursday, weekly jobless claims figures will be released, and on Friday the University of Michigan will release its consumer sentiment index for May.

Other economic data on tap include the NFIB small-business index, to be released Tuesday morning, industrial production and capacity utilization figures on Wednesday, and housing starts and building permits figures on Thursday.

First-quarter earnings season is largely over, but the week ahead still features retailer results that will also help paint a clearer picture of consumer health. Retail giant Walmart Inc. WMT, +2.38% set to report first-quarter earnings before the start of trade on Wednesday, and on Tuesday morning Ralph Lauren Corp. RL, -1.12% will deliver its first-quarter results.

Other major companies reporting earnings this week include Tencent Holdings Ltd. and Take Two Interactive Software, Inc. on Monday, Alibaba Group Holding Ltd. BABA, -0.58% and Cisco Systems Inc. CSCO, +0.83% on Wednesday, Nvidia Corp. NVDA, -0.80% on Thursday and Deere & Co. DE, +0.37% on Friday.

Fed officials will also be out in force. Highlights include speeches by Boston Fed President Eric Rosengren and Fed Vice Chairman Richard Clarida at a Boston event Monday morning, remarks by New York Fed President John Williams in Switzerland early Tuesday, and a speech by Kansas City Fed President Esther George in Minneapolis on the same day.

Fed Vice Chairman for Supervision Randal Quarles testifies before the Senate Banking Committee on Wednesday morning. Fed Gov. Lael Brainard is scheduled to deliver a speech on the economy and monetary policy on Thursday.

Providing critical information for the U.S. trading day. Subscribe to MarketWatch’s free Need to Know newsletter. Sign up here.