Palantir may face tough competition in the software space from this AI titan that made its name selling AI hardware.

Palantir Technologies (PLTR 0.56%) is quickly becoming the go-to provider of artificial intelligence (AI) software platforms for companies and governments around the globe. Evidence of this can be seen in the recent acceleration in the company’s growth as well as its improving revenue pipeline. Both metrics point toward better times ahead.

Investors are noticing and have been buying Palantir stock hand over fist. The stock is up an impressive 76% so far in 2024, and the following discussion offers clues as to why that has been the case.

Palantir’s AI software platform has gained impressive traction

When Palantir released its second-quarter results last month, the company reported a year-over-year increase of 27% in revenue to $678 million. That was a solid improvement over the 13% year-over-year growth the company delivered in the same period last year, as well as an acceleration over its Q1 revenue growth of 21%.

There was a nice jump in the company’s customer base, as well as the size of the deals that it has been striking with customers. Palantir management credited its improving growth profile to the growing adoption of its Artificial Intelligence Platform (AIP). This is a software platform that helps enterprises and governments integrate generative AI into their processes to help improve operational efficiency.

From helping customers build their own large language model (LLM)-powered applications to helping them accelerate their daily workflows with the help of generative AI, the usefulness of Palantir’s AIP seems to have struck a chord with customers. This explains why the company raised its 2024 revenue growth forecast and expects its top line to increase by 24% this year to $2.75 billion.

More importantly, Palantir seems capable of sustaining its outstanding growth in the long term, considering that it ended the previous quarter with $4.3 billion in remaining deal value (RDV). The metric refers to the total remaining value of Palantir’s contracts at the end of a period, and it rose 26% year over year in Q2.

This AI hardware giant is making strides in the AI software market

So, Palantir seems well on its way to making the most of the huge end-market opportunity available in the generative AI software market. However, there is another way for investors to capitalize on the booming demand for AI software, and a closer look could lead investors to think that it may be a better AI software stock than Palantir.

Nvidia (NVDA -4.08%) has been the go-to choice for companies looking to purchase high-end AI hardware so that they can train AI models, resulting in outstanding growth in the company’s revenue and earnings in recent months. What’s interesting is that CFO Colette Kress’ comments on the recent earnings conference call suggest that Nvidia is starting to make a dent in the enterprise AI software market as well. According to Kress, “We expect our software, SaaS, and support revenue to approach a $2 billion annual run rate exiting this year, with Nvidia AI Enterprise notably contributing to growth.”

CEO Jensen Huang also commented, pointing out that customers can deploy Nvidia AI Enterprise software for $4,500 per graphics processing unit (GPU) per year. Given that Nvidia’s AI GPUs are priced at $30,000 or more for a single chip depending on the configuration, enterprise customers looking to build and deploy AI models are getting a good deal through Nvidia’s AI software platform.

Nvidia provides customers with multiple AI software offerings. For example, the company’s AI Foundry platform, which was launched in July this year, is an end-to-end solution with which customers can build and deploy custom generative AI models. Nvidia offers popular foundation models that can be tweaked by its customers and quickly move AI applications (including chatbots, content creation tools, and document processing tools) into the production phase.

Nvidia also provides pretrained customizable AI workflows that can be used for extracting data from PDFs or deployed for creating customer service workflows, accelerating drug discovery in the field of medicine, or building custom generative AI apps suited to an organization’s needs. What’s worth noting is that the adoption of Nvidia’s software solutions is increasing at a terrific pace thanks to AI.

In its February earnings conference call, Nvidia management pointed out that its software and services offerings reached an annual revenue run rate of $1 billion in the fourth quarter of fiscal 2024. So, the company’s software and services revenue run rate is set to double in the space of just one year. That’s significantly faster than the pace at which Palantir’s top line is set to grow this year.

Throw in the fact that Nvidia benefits big time from the booming demand for its AI chips, which led to 122% year-over-year growth in the company’s revenue in the second quarter of fiscal 2025 to $30 billion, and it is easy to see that the chipmaker is the more diversified play on AI. Another point worth noting here is that Nvidia stock trades at 28 times sales, which is lower than Palantir’s sales multiple of 29.

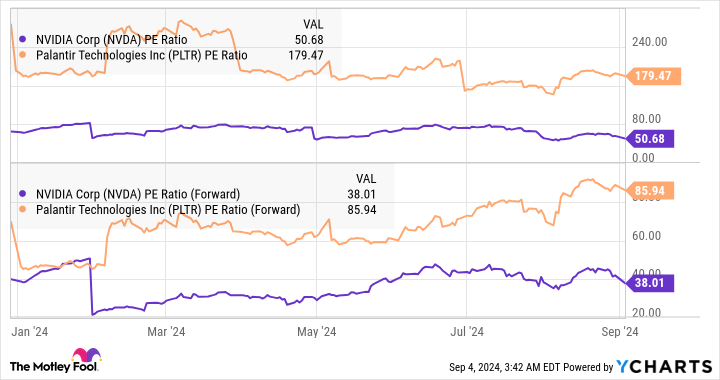

What’s more, Nvidia is the more attractive AI stock when we compare the earnings multiples of both companies.

NVDA PE Ratio data by YCharts

So, investors looking for a cheaper alternative to Palantir to take advantage of the AI software market’s growth would do well to take a closer look at Nvidia, especially considering that the latter already has a flourishing AI hardware business that makes it a better growth stock to buy right now.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. The Motley Fool has a disclosure policy.