Microsoft’s stock has underperformed the S&P 500 this year, and that could continue into next year.

Artificial intelligence (AI) has reenergized many businesses, allowing tech companies to enhance existing products and services and find new ways to grow their operations. Investors have been eager to jump on stocks that are taking advantage of these opportunities. Tech giant Microsoft (MSFT 0.51%) is an excellent example of that.

Its growth has accelerated in recent quarters as new AI-infused products are resulting in stronger sales and profits. Today, the company has a market cap of $3.1 trillion as investing into AI appeared to pay off for the business, at least for now.

But if you take a closer look at the company’s recent earnings report, there is a trend you’ll want to keep a close eye on. Because if it continues, it could lead to trouble for the tech stock in the near future.

Profit growth is slowing

A big challenge for many companies involved with AI these days is they are spending aggressively to not just grow their new AI initiatives but to also promote and market them. And the payoff isn’t always evident to investors.

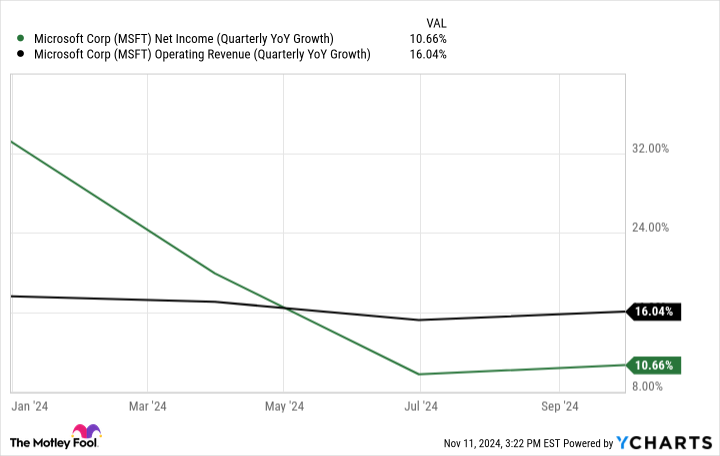

In Microsoft’s most recent earnings report, for the period ended Sept. 30, its bottom line grew by around 11%. That’s slower than in previous periods, and it’s also slower than revenue increased.

MSFT net income (quarterly YoY growth), data by YCharts; YOY = year over year.

There are warning signs that the company’s AI may not be all that impressive. Salesforce CEO Marc Benioff has compared Microsoft’s AI product, Copilot, to an assistant the tech giant introduced in the 1990s, Clippy, which gained a reputation for being more intrusive than helpful.

And according to a recent CNBC survey, roughly half of companies that said they are using Copilot are either on the fence about whether to deploy it to all their employees, or they are still testing the product. It hasn’t been the slam-dunk offering that investors and analysts may have been hoping it would be.

Microsoft’s stock could look even more expensive if its growth rate declines further

Microsoft’s stock is trading at around 35 times its trailing earnings, which isn’t terribly expensive given that the average stock in the Technology Select Sector SPDR Fund is at a multiple of nearly 42 right now. But tech stocks have been at inflated valuations due to their strong earnings numbers this year, and should they slow down, there could be a correction around the corner for these highly valued stocks — and Microsoft is no exception.

Technological research company Gartner previously forecast that many companies may end up abandoning AI projects as they struggle to prove that the initiatives are worthwhile. Gartner believes that as many as 30% of generative AI projects will end up abandoned by the end of next year.

With a possible recession on the horizon and companies scaling back unnecessary expenditures, AI investments could come under fire and be easy targets for cost reductions.

Should that happen, Microsoft may face even greater headwinds next year, and that could be problematic because it may result in an even slower earnings growth rate. Investors already appear to be apprehensive about the stock: Its year-to-date gains as of Monday were just 11% — well below the S&P 500‘s impressive 26% increase in value this year.

Should you buy Microsoft?

If you’re looking for a stock to hold for at least a few years, Microsoft can still be an excellent investment. The business is robust and has many different segments, including gaming and cloud computing, which can ensure it continues growing over the very long haul; this isn’t just an AI stock.

But given its inflated valuation and the growth expectations that come with such premiums, investors who want to buy the stock should be prepared for a possible correction in the near term. This isn’t a cheap stock, and there isn’t much margin of safety — if any — right now.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.