Early trade in futures suggest stocks may finish the week very close to where they started. Bulls may be frustrated, but they should take it as a win.

It’s likely few would have thought the S&P 500 SPX, +0.76% could stay around the middle of its near-four month range when benchmark bond yields TMUBMUSD10Y, 3.990% have again burst above 4%. The last time yields moved up through that landmark in mid-October, the Wall Street equity barometer was about 10% lower.

And here to offer further comfort is Fundstrat’s head of research, Tom Lee. He says the market is ready for a strong eight week rally, a scenario that may catch out many investors because they remain nervous about “the understandable lack of clarity on inflation trajectory, Fed policy path, earnings risk and general heightened concerns about recession.”

Lee gives six reasons for his optimism.

Better inflation news. He reckons the last of the ‘hot’ inflation data was the fourth quarter unit labor cost numbers that came in up 3.2%. Next week will see the start of economic and inflation data for February, which Lee thinks will show softer inflationary pressures and a softer jobs market.

“This will reverse, to an extent, the somewhat alarming surge in inflation and jobs data of Jan (part seasonal, part noisy data),” Lee writes in a late Thursday note to clients.

Supportive Powell. The Fed chair will give his semi-annual testimony to the Senate Banking Committee and House Financial Services Committee, starting next week, and Lee expects Powell to reinforce the ‘data dependent’ message. That means the 25 basis point hike for the March Fed meeting will be cemented, “barring evidence of continued acceleration of inflation.” That should reduce rate uncertainty for the future, too.

Bonds rally. “The bond market will likely pivot dovish in March. The ‘hot’ Jan inflation data caused the bond market to price in higher odds of +50bp in March and April, and Fed speak seems to be pushing back against that — meaning, Fed is less hawkish than [the] recent move in bonds,” says Lee.

Falling VIX. “If the incoming data tilts the way we expect (“softer”), then bond volatility should fall, which supports a stock rally in March to April. This means VIX could fall, and a falling VIX is supportive of higher equity prices.”

The CBOE VIX VIX, -0.71% currently sits at 19.5, a fraction below its long run average of 20.

The market is NOT expensive. Arguing that stocks in general are overvalued is, Lee believes, the confirmation bias of bears waiting out on the sidelines.

“As highlighted earlier this week, ex-FAANG, the P/E (2024) of S&P 500 is 14.8X. And sectors like Energy are 10X and Financials 11X. These are not demanding valuations. And consider the fact that the U.S. 10-yr at 4.0% yield is an implied P/E of a bond of 25X. Yup. The bond market is still far pricier than stocks,” Lee contends.

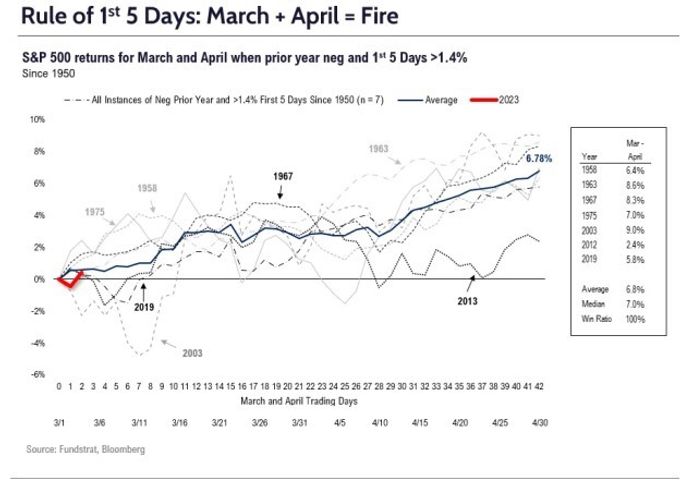

Seasonals are also supportive. Lee has crunched the numbers for the rule of first five days which market lore says that as goes the first five sessions of the January, so goes the year. He has applied that to the last seven times times when the first five days produced a gain of more than 1.4% and came after a down year, as was the case at the beginning of 2023.

“This composite implied market gains into Feb 16 and a consolidation through early March (3/7). 2023 is following this pretty closely. This same composite now implies March to end of April will be the strongest 8 week period for 2023 with a median gain implied of 7%,” Lee calculates.

That means if 2023 follows the same path the S&P 500 could reach 4,250 by the end of April.

Markets

A pullback in 10-year Treasury yields TMUBMUSD10Y, 3.990% is helping S&P 500 futures ES00, +0.43% gain ground. Gold GC00, +0.68% is up as the dollar index DXY, -0.36% dips in response to the easing U.S. interest rates.

For more market updates plus actionable trade ideas for stocks, options and crypto, subscribe to MarketDiem by Investor’s Business Daily.

The buzz

U.S. economic data due for release on Friday include the final reading of S&P Global services PMI for February at 9:45 a.m., followed 15 minutes later by the ISM services report.

Fed speakers include Dallas Fed President Logan at 11 a.m. and Fed Governor Bowman at 3 p.m.

C3.ai shares AI, +2.80% are surging 18% in premarket action after the enterprise artificial intelligence software group delivered well-received results and upbeat forecasts. Wedbush raised its target for the stock from $13 to $24.

Marvell Technology Inc. stock MRVL, +1.92% is down nearly 9% after the chip company met expectations with results for its latest quarter but blamed inventory corrections for an outlook that came in below the consensus view.

The U.K.’s markets watchdog has launched an investigation into the London Metal Exchanges’ handling of a nickel market crisis last year which led it to cancel billions of dollars worth of nickel trades after prices surged.

Shares in various stocks under the Adani umbrella rebounded after Florida-based GQG Partners invested nearly $1.9 billion in the shares that had tumbled, following a report by U.S. short-seller Hindenburg Research late January.

German airline Lufthansa says demand by travelers is robust, helping its shares LHA, +5.96% take off.

Best of the web

Putin’s secret weapon on energy: an ex-Morgan Stanley banker.

You are not a parrot and a chatbot is not a human.

Scandal at South Africa’s Eskom: the CEO and the cyanide-laced coffee

The chart

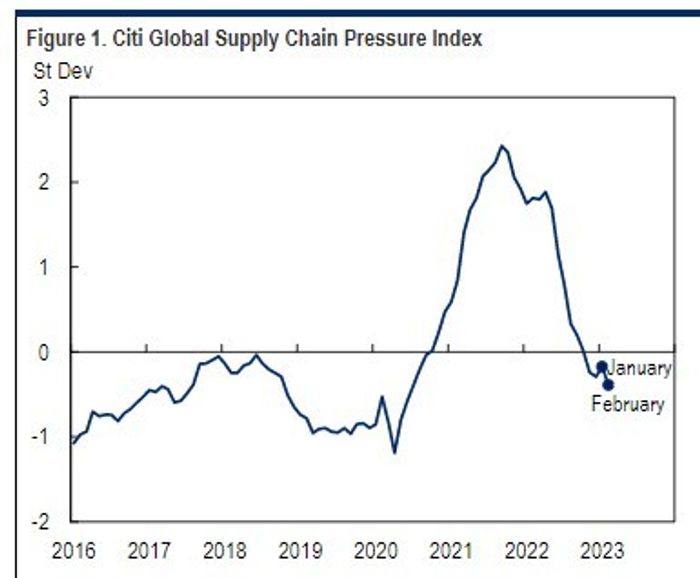

Here’s some good news from Citi’s global supply chain pressure index, which has fallen significantly since last May and is now just above the average level seen in the years before COVID, notes Nathan Sheets, the bank’s chief global economist.

“All three key components of the index—transportation costs, global purchasing managers indexes, and measures of inventory performance—show normalizing conditions. These dynamics suggest that pressures on goods prices are meaningfully reduced relative to last year and our modeling argues that core goods inflation could soon be running 1% or under in the U.S. and Developed Markets more generally.”

Sheets does also note, however, that the service sector is the source of much current inflationary pressures and “unless services inflation breaks far sooner and more forcefully than expected, many major central banks are likely to keep tightening policy in coming months.”

Top tickers

Here were the most active stock-market tickers on MarketWatch as of 6 a.m. Eastern.

| Ticker | Security name |

| TSLA, -5.85% | Tesla |

| BBBY, +4.00% | Bed Bath & Beyond |

| AMC, -7.15% | AMC Entertainment |

| XELA, +40.00% | Exela Technologies |

| GME, +0.22% | GameStop |

| TRKA, +17.66% | Troika Media |

| NIO, +2.94% | NIO |

| SI, -57.72% | Silvergate Capital |

| APE, -10.70% | AMC Entertainment preferred |

| AAPL, +0.41% | Apple |

Random reads

Living the tiny house lifestyle for free in Atlanta….

Terrible puns as Little Italy’s oldest cheese shop closes.

New gecko species found on Australian island.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton