Wall Street loved Netflix’s Q3 earnings. Should you?

The streaming wars have been raging for years now, with some of the world’s biggest companies fighting for eyeballs. Amazon, Apple, and others are duking it out, spending billions pumping out content in an attempt to capture market share. The war is expensive. Although direct financial and viewership data is hard to pin down — many companies fold their TV divisions into larger segments — it’s clear that the economics aren’t working for many.

Few companies have a war chest the size of Apple, but the iPhone maker is reportedly reworking its strategy, trying hard to rein in its massive spending. The company spent at least $20 billion in the five years it has made original content — that doesn’t include the billions it spent licensing content as well, spending a whopping $500 million on movies from just three directors. Despite these numbers, it’s managed to capture just 0.2% of TV viewing in the U.S.

But it’s a different story for the streaming king, Netflix (NFLX 11.09%) — the company that launched a thousand streamers. Netflix pioneered the streaming category and everybody else is playing catch up. Here’s a closer look at its enduring success.

Netflix is raking in cash and beating expectations

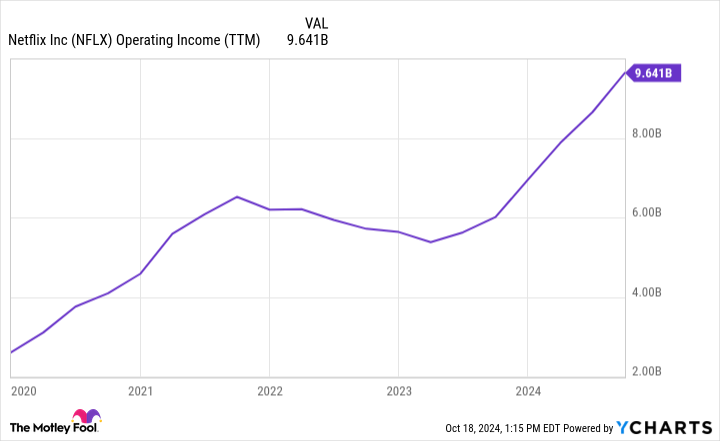

The streaming giant released its third-quarter earnings results on Thursday, Oct. 17 and Wall Street was impressed; it exceeded consensus estimates for both revenue and earnings per share (EPS). The market reacted to the news and shares are up about 10% as of this writing. While it’s no longer the only streamer turning a profit, it’s the only one that has reliably for years and on the scale it is. Walt Disney reported an operating income of $47 million for Q3 2024 for its streaming services, which include Disney+, Hulu, and ESPN+. Netflix’s Q3 operating income? Nearly $3 billion.

Take a look at the company’s steady rise in operating income over the last few years in the chart below.

NFLX Operating Income (TTM) data by YCharts

Tiered subscriptions are changing the game

Many of us remember the promise of streaming — premium content at a fraction of the cost of cable with no ads. Unfortunately for consumers, but fortunately for investors, that promise has been broken. Hulu helped pioneer the “ad-supported” model in which users choose between a low-cost tier that comes with ads and a premium, ad-free tier. Netflix introduced its ad-supported tier in late 2022 and it was an immediate boon for the company’s bottom line, as you can see in the previous chart.

An ad-supported tier allows for more users to join who would otherwise feel the service is too expensive and the numbers back this up: Ad-supported subscriptions were up 35% last quarter. On the income side, any potential loss from offering a cheaper tier is largely compensated for by ad revenue.

Netflix is still delivering hits

While many streamers are struggling to deliver shows that take off, Netflix is not. The company has had a string of hits recently with shows like Nobody Wants This and House of Ninjas — a show in Japanese that delivered a larger U.S. audience than Apple’s $250 million Masters of Air. The second season of the company’s smash hit Squid Game is set to release soon, as well as several other high-performing IPs. Netflix seems to be firing on all cylinders at the moment.

Incredibly, despite what might appear to be a market share that is approaching saturation, Netflix accounts for just 8.4% of TV watching in the U.S. There is a lot of room to run here. Now, the stock is trading at a pretty high premium — its price-to-earnings ratio (P/E) is currently sitting just shy of 40 — but I think its prospects easily justify it. Netflix is in the driver’s seat at the moment and has a huge amount of space to expand and plenty of wiggle room in pricing that can continue to boost sales. While the war is far from over, Netflix certainly has the upper hand.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Johnny Rice has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, Netflix, and Walt Disney. The Motley Fool has a disclosure policy.