NVIDIA(NasdaqGS:NVDA) is navigating a dynamic period marked by both impressive growth and significant challenges. Recent highlights include record-breaking revenue growth driven by the Data Center segment and innovative product launches, counterbalanced by increased operating expenses and competitive pressures in China. In the discussion that follows, we will explore NVIDIA’s core advantages, critical issues, growth opportunities, and key risks to provide a comprehensive overview of the company’s current business situation.

Navigate through the intricacies of NVIDIA with our comprehensive report here.

Strengths: Core Advantages Driving Sustained Success For NVIDIA

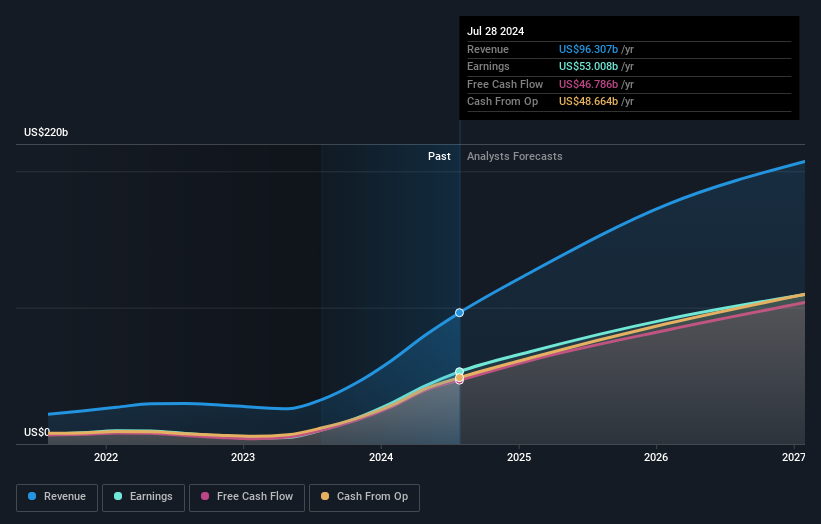

NVIDIA has demonstrated exceptional financial health, with record-breaking revenue growth. In Q2, revenue reached $30 billion, marking a 15% sequential increase and a 122% year-on-year rise. This performance is largely driven by the Data Center segment, which reported $26.3 billion in revenue, up 16% sequentially and 154% year-on-year. Additionally, the company boasts high gross margins, with GAAP gross margins at 75.1% and non-GAAP gross margins at 75.7%. The strong demand for NVIDIA’s products, particularly from frontier model makers and generative AI applications, further underscores its market leadership. Furthermore, innovative product launches like the NVIDIA H200 platform have bolstered its competitive edge, shipping to large CSPs, consumer Internet, and enterprise companies. NVIDIA’s seasoned management team, with an average tenure of 15.7 years, has been instrumental in steering the company towards these impressive achievements.

Weaknesses: Critical Issues Affecting NVIDIA’s Performance and Areas For Growth

NVIDIA faces several challenges. The company’s GAAP and non-GAAP gross margins were down sequentially due to inventory provisions for low-yielding Blackwell material and a higher mix of new products within the Data Center. Operating expenses also increased by 12% sequentially, primarily due to higher compensation-related costs. Additionally, the competitive market in China poses a significant risk, with Data Center revenue from China remaining below previous levels due to export controls. Furthermore, while NVIDIA is considered a good option compared to its peers with a Price-To-Earnings Ratio of 57.4x versus the peer average of 102.4x, it appears expensive relative to the US Semiconductor industry average of 26.9x. The stock is also trading above the estimated fair value of $94.06, suggesting potential overvaluation.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

NVIDIA has several promising opportunities to further enhance its market position. The expansion in sovereign AI, as countries recognize AI expertise and infrastructure as national imperatives, presents significant growth potential. The enterprise AI wave has also started, with enterprises driving sequential revenue growth in the quarter. NVIDIA plans to launch new Spectrum-X products annually to meet the growing demand for scaling compute clusters. Additionally, the demand for Blackwell platforms is expected to remain high, well above supply, into the next year. The company’s strategic alliances, such as the collaboration with Salesforce to develop advanced AI capabilities for the enterprise, further strengthen its competitive advantage.

Threats: Key Risks and Challenges That Could Impact NVIDIA’s Success

Several external factors pose risks to NVIDIA’s sustained success. The competitive market in China remains a significant challenge, with expectations of continued competitiveness. Economic factors impacting capital expenditures (CapEx) are also a concern, as debated by market analysts regarding the sustainability of CapEx investments by NVIDIA’s customers. Regulatory issues are another potential threat, as the company must maintain compliance with evolving regulations to sustain its market leadership. Additionally, significant insider selling over the past three months raises concerns about potential internal challenges. These factors could impact NVIDIA’s growth and market share in the long term.

Conclusion

NVIDIA’s impressive financial health and market leadership, driven by strong revenue growth and high gross margins, position it well for continued success, particularly in the Data Center and AI segments. However, challenges such as increased operating expenses, competitive pressures in China, and a higher Price-To-Earnings Ratio compared to the US Semiconductor industry average suggest potential headwinds. Despite these risks, NVIDIA’s strategic initiatives, including its expansion into sovereign AI and enterprise AI, along with strong demand for its innovative products, offer substantial growth opportunities. Investors should weigh these factors carefully, considering the stock’s current trading price relative to its estimated fair value and the broader industry context, to make informed decisions about the company’s future performance.

Taking Advantage

Already own NVIDIA? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks. Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.