In a recent research note, Oppenheimer analyst Rick Schafer laid out the bull case for buying Nvidia (NVDA) stock — why he rates it “outperform” and expects Nvidia shares to nearly double to $300 over the next 12 months. (To watch Schafer’s track record, click here)

As Schafer tells it, Nvidia’s software and chips have made the company essential to the “AI ecosystem,” giving Nvidia management “unique visibility as they develop products in lockstep with cloud hyperscale customers.” The company’s central position in AI also helps to make available to Nvidia multiple levers that it can pull, to keep its growth going despite the Fed’s efforts to slow the economy. These include not just AI (artificial intelligence), but also chips used data centers (DC), and of course the company’s flagship gaming chips business as well.

Granted, in the near term, Nvidia will likely hit some speed bumps. In particular, COVID-19 lockdowns in China and lost demand for semiconductors due to the Ukraine/Russia conflict are likely to subtract about $500 million in revenues that Nvidia would otherwise have booked in Q2. This will result in an absolute, sequential decline in gaming revenues in the quarter. Networking revenues will also probably face “constraint” in the quarter. Finally, Schafer discussed the elephant in the room — cryptocurrency mining — noting that a decline in the price and demand for Ethereum may “materially” affect whatever (still unknown) portion of Nvidia’s revenues derive from GPUs sold and repurposed by its customers for cryptocurrency mining.

On the other hand, data center revenues are expected to climb sequentially in Q2, and by Q3, Schafer sees Nvidia beginning to fire on all cylinders again. “NVDA’s platform of CPU, GPU, DPU” (respectively, central processing units, graphics processing units, and data processing units) “and software work together to enable an accelerated computing ecosystem,” explains Schafer, helping to sustain sales. Additionally, in Q3 the analyst sees Nvidia releasing its long-awaited new Ada Lovelace GPU chips for gaming.

The H100/Hopper GPU is also expected to ramp production in Q3, “extending NVDA’s AI training/inference lead.” And Schafer believes that this Hopper GPU, alongside the Grace CPU superchip, will drive “the next wave of AI applications including Digital Twins (virtual worlds), transformers and large language models capable of interpreting context/meaning.”

In the near term therefore, gaming revenues and GPU sales will probably help to lead Nvidia stock higher this year. Longer term, though, sales of chips to develop AI applications may turn out to be the strongest card in Nvidia’s deck.

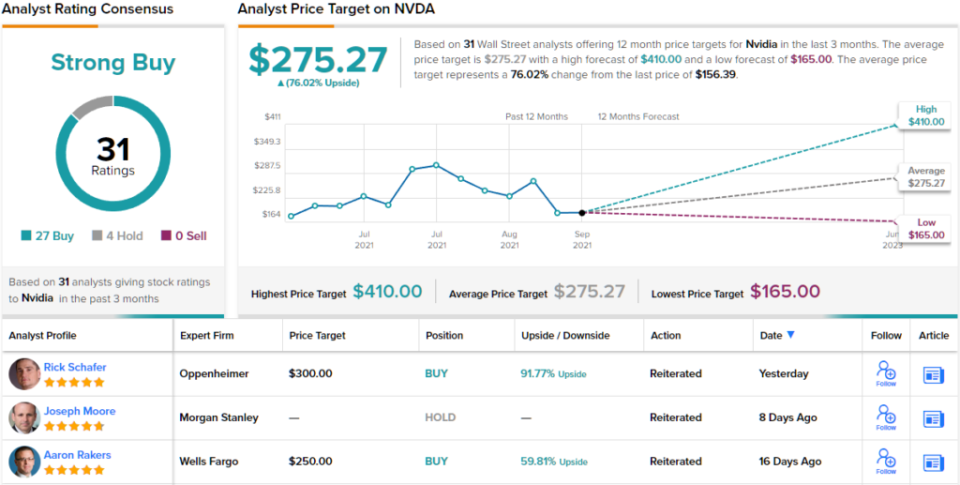

Overall, Wall Street would tend to agree with this bullish outlook – as shown by the 27 to 4 breakdown in recent reviews, favoring Buys over Holds and supporting a Strong Buy consensus view. NVDA is trading for $156.27 and its $275.27 average price target implies an upside of 76% in the next 12 months. (See NVDA stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.