Estimating home values—both in aggregate and for individual homes—is a notoriously complicated process. This is because homes are durable, complex goods, and each home is unique with respect to its location, features, or both. What’s more, homes are thinly traded, meaning very few of them transact in a given year. This makes finding good comparable home sales difficult, or even impossible, in some markets.

As a result, sophisticated measures of aggregate and individual home values have emerged to account for these difficulties. These include repeat-sales price indexes and median home value indexes, as well as home-value estimates for individual homes.

This isn’t normal

In normal times, generating accurate home- price indexes and individual home values is challenging enough. Add to this the unprecedented characteristics of a pandemic-distorted housing market, and the landscape for home valuation just got a lot trickier over the past 18 months. These distortions include:

- Housing inventory hitting record lows: Sellers’ fears of having sick strangers in their homes led to a quick reduction in the number of homes on the market, and this reduction was a catalyst in inducing a downward spiral of inventory. This also disincentivized future sellers from listing because they too then would have needed to buy another house, thereby exacerbating the inventory problem. As a result, inventory fell to the lowest level on record in January and February of 2021, according to the National Association of Realtors.

- Price growth accelerating to record highs: A desire to buy homes with offices, near natural amenities and in less-expensive areas fueled a large increase in new and reshifted demand in the housing market. Low mortgage rates also enticed the marginal buyer to make the move from renting to owning. The end result was the largest increase in home-price growth ever recorded in U.S. history at 19.7% year-over-year in July 2021, according to the S&P/CoreLogic/Case-Shiller Index.

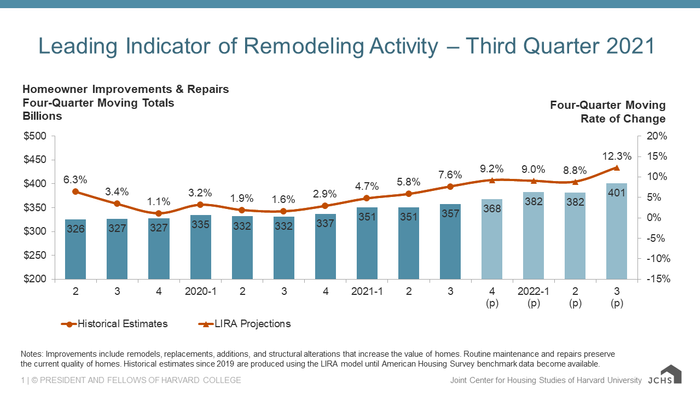

- Home renovation activity reaching near record levels: As a result of higher prices and lower inventory, many existing homeowners decided to renovate their homes as a substitute for selling and trading up. This is reflected in aggregate measures of home-renovation expenditures spiking during the pandemic. Inflation-adjusted expenditures rose to $312 billion in the first quarter of 2021, the third highest amount on record, according to the Harvard Joint Center for Housing Studies, sitting just below the fourth quarter of 2006 and the first quarter of 2007.

Distortionary effects

How have these distortions affected the landscape of home-value measurement?

First, home-value metrics that rely on listing prices will be using a much smaller number of listings, which would likely introduce volatility into those measures.

Second, rapidly accelerating (or decelerating, for that matter) home values mean measures that rely on lagged home sales as inputs might be slow to pick up inflection points in the market. These, however, are only likely to affect small area measures of home value first, since the sample size at the national level is probably still large enough to be immune to volatility and local-area slowness of home sales reporting.

Third, and the most serious impact, is that the rising level of home-renovation expenditures in the U.S. likely bias our home-value indexes and estimates. This is because all of the popular repeat home price indexes assume that there is little or no work done to a home between sales, and thus attribute 100% of the change in value purely to market conditions.

Now read this: Housing inflation is getting worse. Will Biden’s ‘Build Back Better’ program help renters and buyers?

While some individual estimates use listing descriptions of listed homes to guess the condition of the home, a very small share of the housing stock gets listed every year. A share small enough that, practically speaking, most individual home-value estimates also do not account for changing property conditions.

The impact is that existing home-price indexes likely overestimate home-price growth because some of the increase in value is actually coming from capital improvements, not market appreciation, while existing valuation models likely underestimate the value of off-market homes since they do not incorporate information on renovation activity. These biases open up a landscape ripe for improvement in the home-value index and estimate spaces.

Ralph McLaughlin is the chief economist at Kukun, an AI-powered property technology platform for homeowners and real estate investors that offers access to home data and analytics.

‘It’s really a toy’: How reliable is Zestimate, Zillow’s extremely popular home-valuation tool?

Real-estate investors are less optimistic about the U.S. housing market—here’s why