If you are looking to save a piece of your salary for retirement and are hoping to get some tax advantages for doing so, you typically have five options.

If you have a 401(k) or 403(b) at work, you could contribute before-tax salary deferrals to these plans. If the 401(k) or 403(b) has a Roth feature, you could make Roth contributions instead. Alternatively, if you are eligible, you could make a contribution to a traditional before-tax IRA or a Roth IRA. Finally, if your employer has a high deductible health plan, you could choose to make contributions to a health savings account (HSA).

This last option is often overlooked, yet it may be the most beneficial alternative. But first we need to start with the premise that HSAs can be used as an opportunity to maximize retirement assets.

Too many people merely think of these accounts as a way to pay for current medical expenses. However, if you can afford to pay for current medical bills out of pocket, you just might find that HSA contributions are the most beneficial way to accumulate retirement savings. The reason: the ability to make before-tax contributions, experience tax-free growth, and receive tax-free distributions provide the HSA with an advantage over using Roth 401(k) or Roth IRA contributions (both use after-tax contributions) or using traditional before-tax 401(k) or before-tax IRA contributions (both distribute funds that are taxed as ordinary income).

Two qualifications are needed before we take a closer look.

First, never leave matching money on the table if you are likely to become fully vested in these employer contributions. In other words, contribute enough to extract as much money from the employer as possible.

Second, strategic asset location will always be an important consideration. In other words, having some money to pull out tax-free can be a compelling option in retirement.

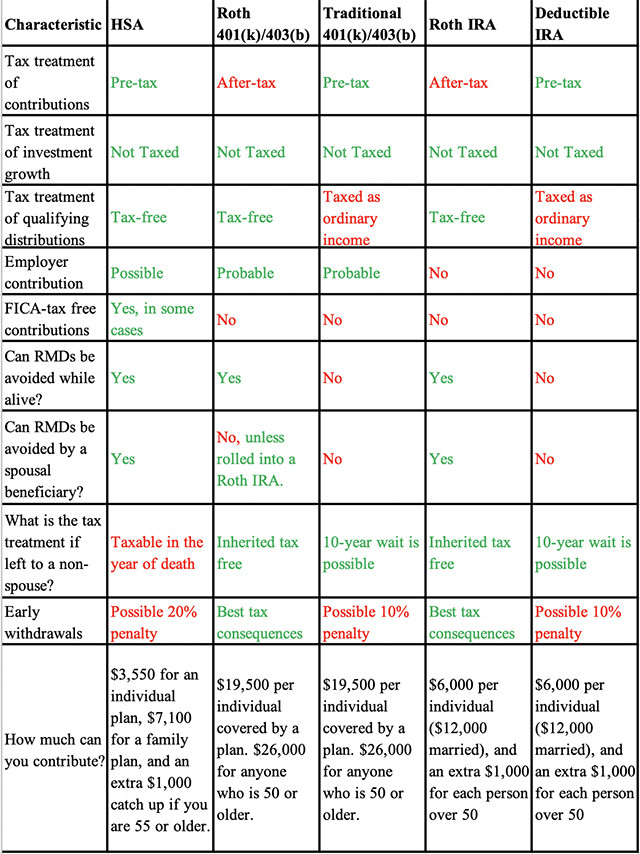

If you are considering using your HSA as a retirement account rather than a checking account to pay for current medical expenses, the next logical question is: Is the HSA the optimal place to put your money? The table below gives you the information you need to make this choice. The text that follows will clarify what it all means and provide context for your decision.

Beneficial tax treatment of contributions, growth, and distributions

The only option checking all three boxes is the HSA. The apprehension is that getting all three tax advantages comes with a price: using the money only for qualified medical expenses. The good news, however, is that you can use the money for past, current, or future qualifying medical expenses. Fortunately, the list of expenses is abundant, and it’s almost inevitable that you will encounter these qualified medical expenses. The list includes:

• Premiums, deductibles, and copayments for medical, dental, prescription drug, and vision expenses (that are medically necessary and not just cosmetic in nature)

• Premiums paid after age 65 for Medicare or an employer’s retiree medical plan (but not for a Medicare supplement plan)

• COBRA premiums

• Premiums for qualified long-term care insurance (up to age-based LTC premium levels)

• And a long list of prescription drugs and other items sanctioned in IRS Publication 502, but don’t count health insurance expenses that were taken as itemized deductions, and as rule of thumb, things bought in the front of the pharmacy don’t count (i.e., aspirin and other nonprescription drugs except insulin).

Why it all matters

Because of the triple tax advantage available for HSA funds these funds can be stockpiled and invested and provide a powerful tool in your retirement arsenal as illustrated in this example.

Example: Arthur and Katie are married, both 74 years old, and retired. They need to put a new roof on their house ($25,000) as well as replace their aging furnace and central air unit ($20,000). They had saved receipts from when they were covered by an HSA at work and during that time, they paid $50,000 out of pocket over 10 years for qualified medical expenses. Because they contributed to the HSA for 10 years ($50,000) and invested the money wisely, the HSA account currently has $80,000 in it. Arthur and Katie can take $45,000 from their HSA account to pay for the roof and HVAC costs because HSA funds can be used to “reimburse” their medical expenses incurred before retirement regardless of the fact that this occurred many years before the withdrawal. In addition, they can then use the remaining $35,000 to pay for current medical expense and future medical costs as they occur. Because of proper planning, using tax-free HSA money will enable them to remain in their expected tax bracket even when they have large expenses. This means they may pay lower taxes and it also means they may pay lower Medicare Part B premiums.

Employer contributions

As was stated before it is imperative to contribute to any plan that enables the employer to tack on funds conditioned to your contribution. However, once you have secured the 401(k) match, your next step will be to contribute to the HSA to get any employer funds possible and to be in a position to take advantage of the Arthur and Katie scenario.

FICA-tax

HSAs are the only vehicle that allows contributions to be made FICA-tax free. This only occurs, however, if the contributions are made through a cafeteria plan (this is a common situation). If there is no cafeteria plan involved, the contributions are tax deductible even if you use the standard deduction (but not FICA-tax free).

RMDs while alive

HSAs and Roth IRA money have the advantage of being able to avoid required minimum distributions (RMDs) while you are alive. However, Roth and traditional 401(k) money, as well as traditional IRA funds, are subject to RMDs. Note, however, one mitigating factor for Roth 401(k) money is that you can avoid having to take RMDs from the Roth 401(k) money by rolling the money into a Roth IRA.

RMDs after death

If the spouse is the beneficiary, then HSAs and Roth IRAs have the advantage of avoiding RMDs for your widow. On the other hand, before-tax and Roth 401(k) plans as well as traditional tax-deductible IRAs will be subject to the required minimum distributions based on the spouse’s age. (Once again, a rollover from a Roth 401(k) to a Roth IRA may be in order.)

There is one critical drawback to HSA funds compared with Roth or before-tax 401(k) funds and Roth or before-tax IRAs when the beneficiary is not the spouse. If this is the case, HSA funds need to be distributed (and taxed) in the year of death and the funds from the remaining options can stretch tax savings for the nonspouse beneficiary for up to 10 years after the year of death based on new rules brought about under the recently enacted SECURE Act. However, an easy way to circumvent this potential HSA disadvantage is to make sure the husband and wife spend their HSA funds while they are still alive.

Premature withdrawals – The rules for withdrawals are as follows:

• HSA – As long as the funds are used for qualified medical expenses there is no tax and no penalty regardless of what age you are and how long ago you started contributing to the HSA account. In some ways this constitutes an HSA advantage over the other options because you can take money out ordinary income tax-free and penalty free. On the other hand, money withdrawn before age 65 that does not pay for qualified medical expenses is subject to ordinary income tax and a 20% tax penalty! This will constitute a huge disadvantage for HSA accounts since the other early distributions are not taxed as heavily.

• Before-tax 401(k) and IRA accounts – Any distribution after age 59½ is taxed as ordinary income and no penalty tax applies. These distributions can be used for any purpose…so the “age 59½ and unlimited use” advantages loom large over the “age 65, only for qualified medical expenses” rules. In addition, even though a pre-59½ distribution is subject to ordinary income tax and a 10% penalty may apply, there are plenty of exceptions to the 10% penalty.

• Roth 401(k) and Roth IRA accounts – Eligible distributions from these plans are not taxed as ordinary income and are not subject to a tax penalty. Eligible distributions require you to have established the account 5-years ago and be age 59½ (or be made on account of death or disability). This can be a huge advantage over the other accounts! What’s more, it is not even so bad for ineligible early distributions from these accounts because only the earnings are subject to ordinary income tax and a 10% penalty.

Putting it all together

Despite the fact that the HSA has compelling advantages over the other options for retirement savings you need to carefully address the downside to HSAs as a retirement accumulation tool. The first disadvantage is that the money can only be used for qualified medical expenses. This constraint does not apply to the other options. The second obstacle is that at death the HSA money left to a nonspouse beneficiary is immediately taxed to the beneficiary (or if left to the estate, the HSA must be taxed on the tax return for the year of death). The before-tax options have a longer window to delay taxation at death and the Roth options will be distributed tax-free. The third drawback is that premature nonmedical withdrawals from an HSA have a 20% penalty tax before age 65 and the traditional before-tax 401(k) and IRA options only have a 10% penalty tax before age 59½. Also, Roth 401(k) and Roth IRA premature distributions also have big advantages over the HSA nonmedical premature distributions.

However, if you can navigate the “medical-expenses only” issue (by stockpiling receipts for medical expenses you paid out of pocket), the “nonspousal death” issue (by making sure the HSA is spent before the second spouse dies), and if you can hold off from taking the money out early, then the HSA contribution option may be right for you because of the triple income-tax advantages, the FICA tax advantage, and the RMD advantages that exist while you and your spouse are alive.

In any case, however, an HSAs should not be used as the exclusive means to fund retirement. So as a starting point it may behoove you to contribute the maximum amount allowed to your HSA each and every year and to invest these funds for retirement rather than use them to pay current medical expenses.