Shares of Palantir Technologies (PLTR 11.14%) have had an amazing run over the last few years. The stock’s recent inclusion in the S&P 500 and strong financial results have sent the stock up 247% year to date, as of this writing.

There are a lot of reasons to like Palantir’s business. It is capitalizing on a booming market for enterprise artificial intelligence (AI) software with revenue growth accelerating this year. But with a market capitalization of about $135 billion, the stock is starting to overshoot a reasonable estimation of the company’s value based on its financial results.

Accelerating growth and impressive margins

Palantir’s revenue accelerated to a year-over-year growth rate of 30% in the third quarter, up from 27% in the second quarter. This growth exceeded management’s guidance by over four percentage points. It’s also impressive that Palantir is starting to see more balanced growth from commercial and government customers, which wasn’t the case a year ago when the commercial segment was growing much faster than its government business.

Palantir’s U.S. commercial revenue grew 54% year over year, while government revenue increased 40%. It was the strongest growth for the government segment in 15 quarters. In September, Palantir signed a contract worth nearly $100 million to expand its Maven Smart System across military services over five years.

Palantir is also adding tremendous value for commercial customers. It closed over 104 deals worth over $1 million last quarter. Companies are noting significant improvements to their operations. For example, Trinity Rail saw a $30 million boost to profits using Palantir’s artificial intelligence platform (AIP).

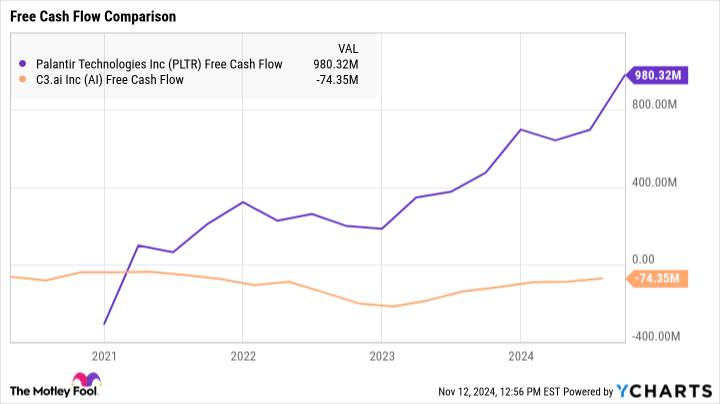

AI software is a competitive market with C3.ai being another viable alternative for companies looking for ways to improve productivity and workflows. But Palantir is not only growing faster than C3.ai, it is clearly able to price its product to earn a healthy margin. Its adjusted free cash flow was $435 million in Q3, bringing the company’s trailing-12-month free-cash-flow margin to 39% of revenue.

Data by YCharts.

The stock’s valuation is getting expensive

I never like to call any stock overvalued. Great companies have a way of proving skeptics wrong. Consider Amazon during the peak of the dot-com bubble when seasoned investors thought the stock was grossly overpriced. But even from its “overvalued” share price in March 2000, Amazon’s market cap has increased from $25 billion to around $2 trillion.

It’s worth paying a premium for Palantir, but no stock is worth ignoring valuation entirely. The stock’s $135 billion market cap is very high against its $2.6 billion in revenue and $980 million in free cash flow. Palantir has had a volatile trading history, and its high valuation puts it at greater risk of experiencing a pullback sooner or later.

I would focus on other opportunities and keep an eye on Palantir stock, at least until the business has grown enough to bring its valuation down from these peak levels.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. John Ballard has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Palantir Technologies. The Motley Fool recommends C3.ai. The Motley Fool has a disclosure policy.