Looking for stocks that can crush the market? These two companies look poised to be big winners.

The S&P 500 index includes roughly 500 large-cap U.S. stocks and is often used as the key benchmark for measuring the broader stock market’s performance. Over the last five years, the benchmark index has delivered a total return of 109%. Over the last decade, it has produced a total return of 257%.

Investing in an exchange-traded fund (ETF) that tracks that S&P 500 index is a great, low-risk investing move, but there are also stocks that are part of the index that will go on to produce returns that crush the index’s average. With that in mind, read on to see why two Motley Fool contributors think that buying these S&P 500 growth stocks and holding for the next five years would be a great move.

This tech giant still has room to run

Keith Noonan: With gains of roughly 22% this year, Amazon (AMZN 0.78%) stock has slightly underperformed the S&P 500 index’s total return of 23%. But there are good reasons to think that the tech giant will far outperform the benchmark index over the next half decade.

For starters, Amazon’s business continues to look quite strong. While the stock isn’t beating the S&P 500 in 2024’s trading as of this writing, the business has generally been serving up encouraging results.

Amazon’s revenue increased 10% year over year to reach $148 billion in the second quarter, and its operating income more than doubled year over year to $14.7 billion. Revenue for the company’s Amazon Web Services (AWS) cloud infrastructure business increased 19% year over year to reach $26.3 billion. Meanwhile, the company’s digital advertising business rose roughly 20% year over year to hit approximately $9.5 billion. The e-commerce-focused North American segment saw sales climb 9% to $90 billion, and the similarly structured international segment saw sales increase 7% to hit $31.7 billion.

Growth for the higher-margin AWS and digital-advertising units, along with margin improvements in e-commerce, have helped Amazon score strong profit growth this year. Its e-commerce business still delivers the majority of Amazon’s overall revenue, but there’s a good chance that cloud services and digital advertising will continue to account for a bigger portion of the overall sales picture. Increasing sales contributions from these higher-margin businesses should help push the company’s combined margins higher.

But it would be a mistake to underestimate the relatively slow-growing, lower-margin e-commerce business when it comes to assessing Amazon stock’s return potential over the next five years. While the potential for artificial intelligence (AI) to be a sales driver for AWS has already been baked into many forecasts, the potential for AI to have a transformative impact on the company’s online retail business still appears to be underappreciated.

With AI and robotics paving the way for increased automation of the company’s warehouse and delivery operations, some of the untapped profit potential of the tech giant’s massive e-commerce imprint could soon begin to be unlocked. If these unfolding tech trends start to meaningfully lower operating costs for the online retail business, Amazon stock is poised to soar.

This retail leader can keep crushing the market

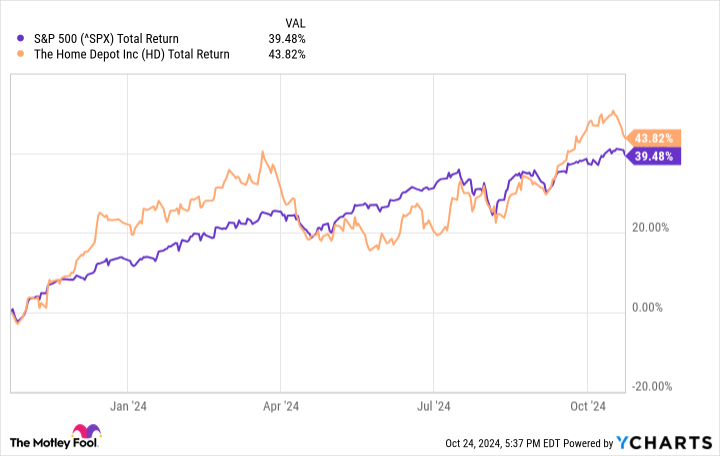

Jennifer Saibil: Home Depot (HD -0.94%) has been a market-crushing stock pretty much forever. It has gained close to double the S&P 500’s return over the past 10 years, and the longer you go back, the wider the gap becomes — it’s grown more than 3 times the broader market’s gain over the past 15 years.

If you needed any evidence of this company’s strength, it’s still outperforming the market over the past year despite major challenges. These challenges are external, and the market recognizes that, as well as how well Home Depot is coping with the situation.

The real estate market is under severe pressure due to high mortgage rates, and in general shoppers are steering clear of large, expensive items because of inflation. Home Depot reported a small sales increase in the fiscal second quarter (ended July 28) due to a recent acquisition and new stores, but comparable sales were down 3.3%. Average ticket declined 2.2%, but big-ticket items (over $1,000) were down 5.8%, and large products like kitchen remodels had “softer engagement.”

With interest rates starting to come down, the tide could start to turn. Home Depot is the largest home improvement chain in the world, with more than 2,300 stores and robust digital channels. It’s still incredibly profitable despite the downturn in comparable sales, and it’s generating growth where it can. The omnichannel component has become an important part of its business, and digital sales increased 4% year over year in the second quarter, with half of orders picked up in stores.

It’s pulling several growth levers. It’s opening new stores, with 12 expected for fiscal 2024, and it’s investing in acquisitions and improved services, especially for the pro segment. It’s well positioned to get back to growth as soon as the industry does, and there’s every reason to believe that it can continue to crush the market over the next five years and beyond.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jennifer Saibil has no position in any of the stocks mentioned. Keith Noonan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Home Depot. The Motley Fool has a disclosure policy.