As of this writing (Feb. 25), there are only three companies with a market capitalization over $3 trillion: Nvidia, Apple, and Alphabet. Microsoft once boasted a $3 trillion valuation, but over the last month, its share price has slid enough to knock the Windows maker out of the exclusive club.

Further down the list of trillion-dollar stocks is Meta Platforms (META 1.29%), which is currently valued around $1.6 trillion.

I’m going to break down how Meta is transforming its advertising empire thanks to AI. From there, I’ll make the case for why Meta could potentially achieve a $3 trillion market cap within the next two years.

Image source: Getty Images.

How is Meta using AI?

At the core of Meta’s AI roadmap is a new machine learning product called Advantage+. Advantage+ helps marketers automate their ad campaigns, streamlining ad creation and demographic targeting.

The core idea is that AI helps marketers get a better sense of which ads resonate with different customer types. From there, advertisers can strategically allocate their budgets across Meta’s family of apps — Facebook, Instagram, and WhatsApp — depending on what they are trying to sell and to whom.

One thing to know about Advantage+ is that it is a relatively new product that Meta constantly iterates and to which it adds new features. For this reason, management tends to provide sporadic updates on the progress of Advantage+.

Meta Platforms

Today’s Change

(-1.29%) $-8.50

Current Price

$648.51

Key Data Points

Market Cap

$1.6T

Day’s Range

$638.13 – $649.33

52wk Range

$479.80 – $796.25

Volume

1M

Avg Vol

16M

Gross Margin

82.00%

Dividend Yield

0.32%

During the third quarter, Meta CFO Susan Li shared that Advantage+ had reached a $60 billion annual revenue run rate. While a new headline figure was not revealed during the fourth-quarter earnings call, Meta’s management shared just enough to imply that its AI efforts are continuing to pay off.

In Q4, Meta’s video generation tools, which are part of the Creative suite underneath the Advantage+ umbrella, hit a $10 billion annual revenue run rate. Growth from this specific segment outpaced the increase from overall ad revenue by 3x quarter over quarter.

In addition, Meta’s next-generation attribution tool drove a 24% increase in incremental conversions compared to the company’s standard model. This new attribution feature has already achieved a multi-billion-dollar annual run rate since its launch seven months ago.

Understanding Meta’s valuation

In 2024, Meta spent $39 billion on capital expenditures (capex). Last year, the company accelerated its spend by 85%, bringing total capex to $72 billion. During the Q4 earnings call, management revealed that Meta could spend up to $135 billion on capex this year — nearly double the amount compared to 2025 levels.

I bring this up because despite the company’s progress on the AI frontier, I think most investors still do not understand how Meta is deploying artificial intelligence. Hence, investors are focusing on the effects that rising AI infrastructure costs will have on free cash flow more than anything else. These dynamics are reflected in Meta’s valuation.

Meta currently trades at a forward price-to-earnings (P/E) multiple of 21 — essentially in line with its three-year average. In my eyes, Meta’s forward P/E reflects some degree of uncertainty driven by skepticism over the company’s rising infrastructure budget.

Can Meta reach a $3 trillion valuation?

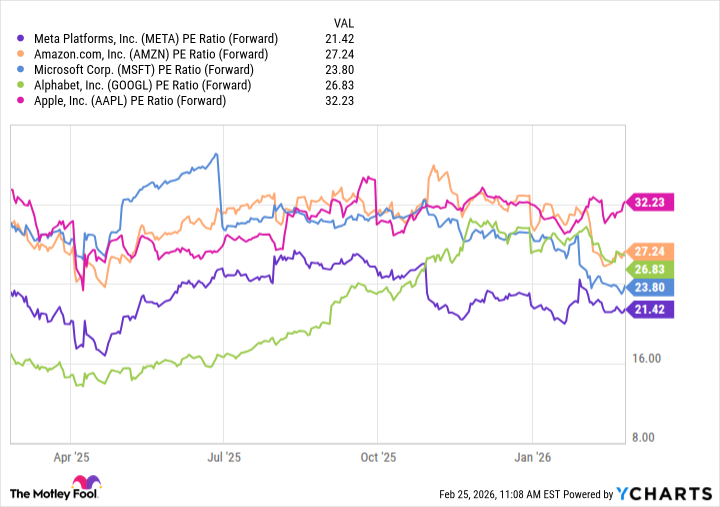

As the chart below shows, Meta is valued at a significant discount relative to its hyperscaler cohorts based on forward P/E. I think there are two factors at play here.

Data by YCharts.

First, Meta’s discount likely reflects its reputation as a glorified advertising platform, rather than a pure play AI specialist. Second, while Apple may not be known for its AI efforts, the company is able to sustain a premium valuation thanks to its ability to generate robust cash flows year after year. While Meta has also done this, investors don’t appear to be giving the company the same level of credit.

For this year, Meta’s consensus earnings per share (EPS) estimate among Wall Street analysts is $29.60. Analysts are forecasting EPS to grow 16% in 2027 to $34.34.

In order to reach a $3 trillion valuation, Meta’s forward P/E would need to expand significantly, falling in the range of the mid-30’s. Admittedly, this is a tall order.

I think Meta can still achieve this level of growth over the next couple of years, though. As the company continues to roll out AI-driven features across its ecosystem, I think the return on investment from Meta’s infrastructure spend will become increasingly obvious as the company commands robust unit economics.

As Meta transitions from a social media advertising platform to a more comprehensive AI services business, investors may begin to change their perception of the company and start valuing it more in line with other leading AI developers.

For this reason, I think Meta stock looks like a compelling buy-and-hold opportunity at its current price point, as meaningful AI-driven valuation expansion could be in store.

Add Comment