Stitch Fix shares are down 97% from all-time highs.

During the peak days of the COVID-19 pandemic, people around the world increasingly adopted a work-from-home environment and began finding new ways to entertain themselves when duty wasn’t calling.

One such area was the stock market. Stocks across all industry sectors ebbed and flowed for reasons completely detached from reality. In many ways, the stock market became a digital casino, and many unsuspecting investors learned a hard lesson: Stocks don’t go up forever.

One stock that witnessed unparalleled highs during the pandemic’s height was online fashion retailer Stitch Fix (SFIX -1.09%). What was once a stock trading for $106 per share now sits at just $2.74 — down 97% from its highs.

Below, I explore the rise and fall of Stitch Fix and make the case for why I think the company is a solid acquisition candidate for the right partner.

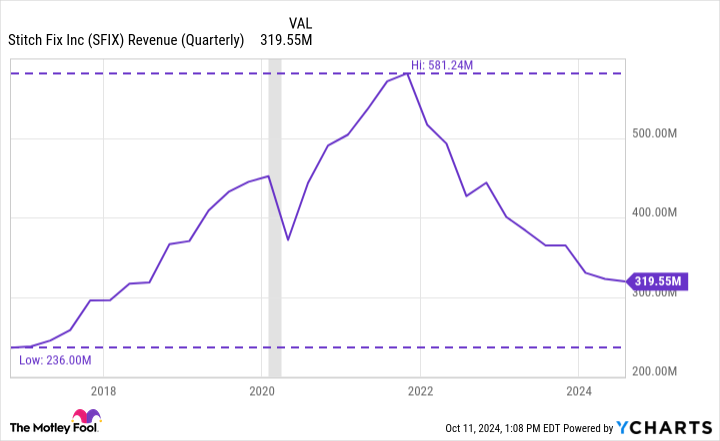

This chart explains it all

The chart below illustrates Stitch Fix’s quarterly revenue since going public. During its first few years as a public company, Stitch Fix consistently generated respectable levels of growth. In 2020, these trends completely kicked into a new gear.

SFIX Revenue (Quarterly) data by YCharts.

The gray shaded column in the chart represents the brief COVID-19 recession. While revenue initially dipped in early 2020, Stitch Fix bounced back spectacularly and witnessed record growth that lasted until the end of 2022.

What happened, and why has Stitch Fix continued to crater?

The simple explanation is that Stitch Fix offered a level of convenience that was tough to match during the peak days of COVID-19. While office buildings remained closed and brick-and-mortar retail outlets experienced declining foot traffic, demand for online platforms such as Stitch Fix took off.

In other words, Stitch Fix was well positioned during an otherwise once-in-a-lifetime event. Once the “new normal” slowly came into effect, people gradually integrated back into society — reviving old habits and shopping preferences.

In addition to the broader societal reopening, the macroeconomy has been battling stubborn inflation for a couple of years now. When the costs of goods and services rise, consumer purchasing power weakens. In turn, people need to make decisions about how and where they are spending money.

Discretionary businesses such as Stitch Fix are more of a luxury and not necessarily a need. The table below illustrates the churn in the company’s active clients over the last several years.

| Category | Aug. 1, 2020 | July 31, 2021 | July 30, 2022 | July 29, 2023 | Aug. 3, 2024 |

|---|---|---|---|---|---|

| Active Clients | 3.5 million | 4.2 million | 3.8 million | 3.1 million | 2.5 million |

Data source: Stitch Fix.

Clearly, Stitch Fix has struggled to retain customers, which is eating away at the company’s growth potential.

Why I think Stitch Fix will be acquired

A shrinking customer base and declining revenue trends go hand in hand. Where I think Stitch Fix really went sideways is in where management decided to allocate capital.

The company tried to differentiate itself from other online apparel storefronts by investing heavily in artificial intelligence (AI) and data science. The idea was that Stitch Fix would collect data on which pieces of clothing its customers purchased and returned in order to get a better sense of shopping patterns and consumer preferences. In turn, by getting to know the customer on a deeper level, Stitch Fix could theoretically leverage its database to drive more enhanced engagement from its users.

Such an idea is quite common on e-commerce platforms. This leads me to my list of potential acquirers:

1. Amazon: One of the most revolutionary ideas in this company’s history is its Prime subscription service. Prime members receive a multitude of benefits, including free shipping, access to a variety of streaming platforms, and early access to new products. I think Amazon has the ability to use Stitch Fix’s customer data in its online marketplace, and the service could represent an additional perk for Prime subscribers.

2. Urban Outfitters: I see Urban Outfitters as another logical candidate to acquire Stitch Fix. The company owns a number of storefronts, including Anthropologie, Free People, and, of course, Urban Outfitters. These stores offer a wide selection of apparel that appeals to several demographics, especially hotly contested Gen Z and millennials.

Furthermore, Urban Outfitters already has a subscription-based online clothing rental asset, called Nuuly. While it’s still early days for Nuuly, the segment’s traction has been quite good so far. I think Stitch Fix could serve as a complement to Nuuly, and broaden Urban Outfitters’ online presence.

Image source: Getty Images.

The bottom line

I think it will be hard for Stitch Fix to salvage itself. The company seems lost, and I’m doubtful that management can right the ship on its own.

With that said, there are some silver linings that shouldn’t be discounted. The company still serves millions of people and is collecting valuable data from its shoppers. I think a larger business such as Amazon may be able to better leverage this data and tuck the Stitch Fix platform fairly seamlessly into its ecosystem. Urban Outfitters also looks like an attractive potential partner, given its success with younger demographics and online clothing subscriptions.

To me, Stitch Fix is still a valuable asset, but it’s time for the company to consider a sale and partner with a larger enterprise.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Amazon. The Motley Fool has positions in and recommends Amazon. The Motley Fool recommends Stitch Fix. The Motley Fool has a disclosure policy.