Alphabet is a stock just waiting to go on a bull run.

Nvidia (NASDAQ: NVDA) has been a top-performing stock for the past two years, and all signs point toward it delivering once again in 2025. However, its growth is also likely to slow, and seeing the stock triple again is not likely in the cards. While I think Nvidia can (and likely will) deliver a market-beating performance, there’s another big tech stock that could outperform it in 2025.

What stock could possibly outperform the king of artificial intelligence (AI) investing? I think it’s Alphabet (GOOG -1.14%) (GOOGL -1.20%), and there are a few reasons why.

Multiple Alphabet business segments are crushing it

Alphabet is the parent company of Google. While it has multiple interesting technologies and different product lines, about three-fourths of its revenue comes from advertising. With the rise of generative AI, many investors were worried that a search engine like Google might become obsolete, but that hasn’t materialized yet. Furthermore, Google is leaning into this trend, and if a competing product finds some success, Google will likely copy it and launch it before its billions of users switch over.

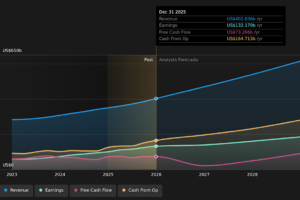

As a result, I think Alphabet will be just fine moving forward, and the results back it up. In Q3, Alphabet’s Google Search revenue rose 12.3% year over year. That’s solid growth from a mature business segment and gives Alphabet a steady platform to do other things with the rest of its business.

Most notably, Google Cloud, its cloud computing division, had a phenomenal quarter, with revenue rising by 35% year over year and delivering a 17% operating margin. This marks a notable growth acceleration from previous quarters, as Google Cloud grew its revenue by 29% in Q2 and 28% in Q1. Management points to its generative AI toolkit as a reason why it’s doing so well, as some of the tools it gives developers access to are unparalleled.

Although Google Cloud only makes up about 13% of the overall business, its growth boost is noticeable at the top level, as overall revenue grew 15% year over year. That growth, combined with various efficiency efforts and the effects of stock buybacks, allowed Alphabet’s earnings per share (EPS) to increase from $1.55 to $2.12 — a 37% rise.

The market loved this quarter, which is why the stock was up following the results. But with all due respect to Alphabet, this isn’t even close to the numbers Nvidia is putting up.

So, how can Alphabet outperform Nvidia in 2025?

Alphabet’s earnings multiple isn’t in line with the business performance

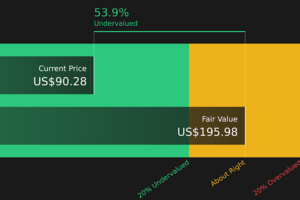

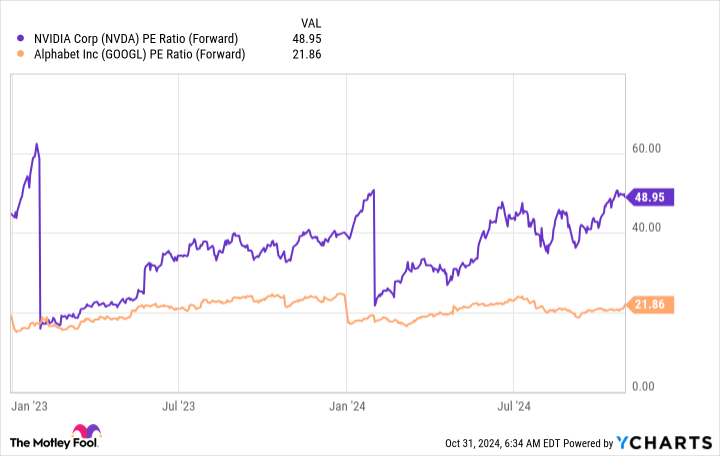

For many reasons, Alphabet doesn’t carry nearly the premium on its stock as Nvidia does. Right now, Alphabet trades for a mere 22 times forward earnings compared to Nvidia’s 49.

NVDA PE Ratio (Forward) data by YCharts

This is a huge price difference, and it shows how expensive Nvidia’s stock is and how cheap Alphabet’s stock is. In fact, Alphabet’s stock is actually cheaper than the broader market as measured by the S&P 500, which trades for 24 times forward earnings.

Compared to other big tech companies, Alphabet is also dirt cheap. Just take Microsoft, for example. In its Q1 FY 2025 (ending Sept. 30) results, EPS rose a mere 10%, yet the stock trades at 31 times forward earnings. Apple‘s best quarter since 2022 began saw 16% EPS growth, yet it trades for 30 times forward earnings.

Essentially, the market is saying Alphabet is a below-average company, which makes no sense considering that Alphabet’s EPS is growing much quicker than the average company in the index.

On the flip side, Nvidia’s growth is expected to slow down next year, with FY 2026 (ending January 2026) EPS expected to rise about 43%.That slowdown will come with a decreased valuation.

So, while Alphabet may not be growing as fast as Nvidia, the combination of Alphabet’s expanding earnings multiple and Nvidia’s likely decreasing multiple, it could boost Alphabet to the performance levels needed to outperform Nvidia in 2025. Whether or not it can outperform Nvidia in 2025, Alphabet is still one of the best values in the market today and an excellent stock to buy right now.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.