Can Roku follow in Netflix’s footsteps? The digital media expert is heading down an extremely lucrative road.

Media-streaming technology veteran Roku (ROKU 1.29%) has plenty of growth catalysts up in the air. The most important and promising is the opportunity to grow the business abroad.

For example, digital advertising is bouncing back from three slow years, the company is diversifying its client list, and the Roku platform’s home page ads provide a uniquely efficient marketing space. Roku is also in the early stages of integrating its ad services with The Trade Desk and its Unified ID 2.0 ad-tracking system.

And I haven’t even mentioned the Emmy-winning Roku Channel yet, which adds another eyeball-magnet revenue stream. This company is pulling every possible lever to ensure long-term business growth.

That’s all good stuff, but I’m only scratching the surface of Roku’s many growth-boosting ideas. Nothing compares to the most important strategy in Roku’s tool belt. It’s a big world out there, and the next era of Roku’s growth story will be written overseas.

The untapped potential of Roku’s global markets

International sales are not a big deal yet. Roku doesn’t even break out these sales in its quarterly earnings report but simply notes that non-U.S. sales account for less than 10% of total revenues.

But that will change over time. Of Roku’s long-lived assets, 17% are found in the United Kingdom and other foreign countries. These assets are data center installations preparing Roku for local streaming services and content production facilities. The company is building a large footprint in overseas markets, far exceeding the current revenue generation in those countries.

Furthermore, Roku is actively distributing its media player hardware through major retailers in Brazil, Germany, Mexico, and the United Kingdom and is in the early stages of monetizing its products and services in places like Canada and Germany. Roku is taking the international opportunity very seriously — and it’s just getting started with this long-term strategy.

Lessons learned from Netflix

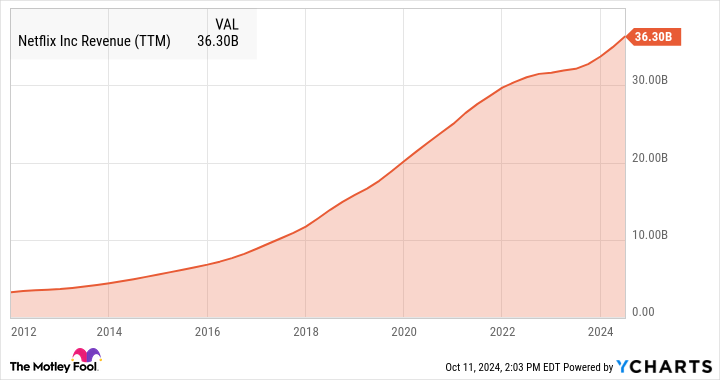

Roku isn’t the first media-streaming expert to explore the international growth avenue. The greatest example is Netflix (NFLX -1.03%), which started out with deeply American DVD-mailer and streaming services before going global in 2016. The worldwide expansion was a pivotal moment in Netflix’s history, opening the floodgates for torrential growth. It’s easy see this top-line acceleration with the naked eye:

NFLX Revenue (TTM) data by YCharts. TTM = trailing 12 months.

Soaring profits followed a few years later, and Netflix investors have pocketed a 4,430% return in 13 years. This is the role model Roku is emulating, with the added benefit of going global about a decade later.

Netflix’s early progress was hampered by low-bandwidth internet connections and unreliable credit card payment systems in many emerging economies. The issues haven’t gone away yet, but most countries have both decent internet access and better payment systems nowadays.

The number of people with internet access has more than tripled since 2012 in places like Thailand and Indonesia, according to Gapminder data. And based on Statista surveys, credit card usage is soaring in many previously underserved countries.

So, it’s easier to access streaming services in 2024 and simpler to collect subscription payments. Moreover, media streaming has evolved into a global phenomenon, and it’s only a matter of time before Roku becomes the leading platform for accessing news, information, and entertainment content. Roku is preparing to take advantage of this boom over the next decade and beyond.

Roku’s market trends and investment appeal

I can’t promise Roku investors will enjoy the same long-term gains as Netflix shareholders, but this stock certainly looks undervalued right now. Roku bears focus on weakness in the digital advertising market over the last three years, ignoring the brighter days that lie ahead with lower inflation. Meanwhile, Roku’s shares are changing hands at the rock-bottom valuation of 3 times sales.

I can’t wait to see Roku pushing the pedal to the metal on international expansion projects. The idea only makes more sense in a more stable global economy, and the worldwide cord-cutting trend is not slowing down. Roku’s stock may have gained 62% from last year’s lows, but it’s still a no-brainer buy in my book.

Anders Bylund has positions in Netflix, Roku, and The Trade Desk. The Motley Fool has positions in and recommends Netflix, Roku, and The Trade Desk. The Motley Fool has a disclosure policy.