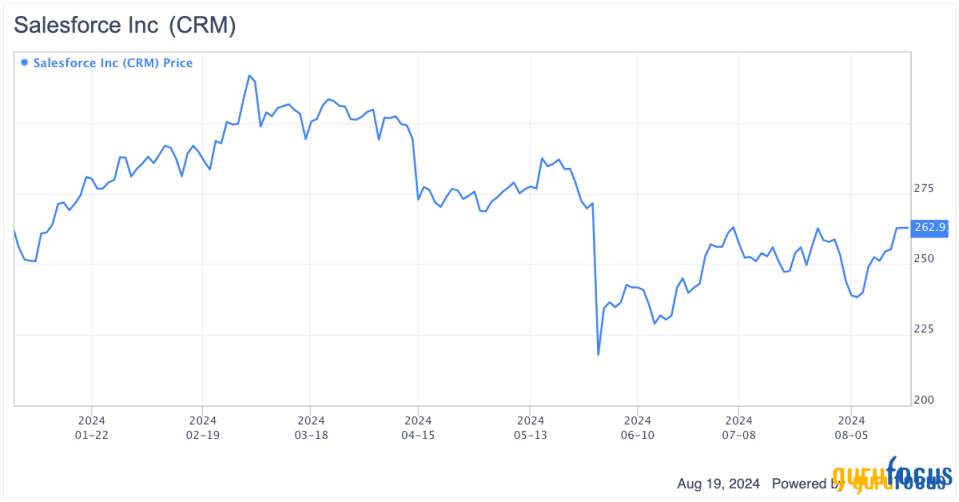

As the clear frontrunner in the customer relationship management software industry, Salesforce Inc. (NYSE:CRM) commands a dominant 21.70% market share. This year, the company’s stock has seen a mix of investor sentiment, leading to relatively stagnant movement. However, after the release of its first-quarter results, shares dropped by 20%.

Salesforce reported total revenue of $9.13 billion, an 11% year-over-year increase, but it fell short of consensus estimates by $13.40 million. Despite this setback, the stock remains up by approximately 2.70% year to date. I believe the post-earnings decline was an overreaction. The company’s fundamentals remain strong, and I see several positive indicators ahead.

As we enter the next supercycle of cloud computing, big tech and e-commerce, global companies are increasingly seeking ways to deepen connections with existing customers while expanding into new markets. Beyond being well-positioned to capitalize on growth in this evolving landscape, Salesforce has also become an even more attractive buy at its current price following the recent dip. Therefore, I remain quite bullish on the stock. In this analysis, I will outline the reasoning behind my outlook by examining Salesforce’s business model, evaluating its current fundamentals, exploring its strategic focus on leveraging artificial intelligence for future growth and assessing the stock’s valuation.

Dominance in the CRM market

Salesforce’s dominance in the CRM sector is particularly noteworthy in an industry poised for significant expansion, with a projected 13% compound annual growth rate between 2024 and 2031. The company’s comprehensive suite of cloud-based software, including the enterprise-focused Slack chat and productivity app, is bolstered by integrated AI capabilities designed to enhance analytics functions. With a massive total addressable market expected to reach $290 billion by 2026 (aligning with the 13% CAGR), I believe Salesforce is well-positioned to capitalize on this market growth through its diverse cloud offerings, increased cross-selling opportunities, CRM consolidation and resulting lower churn rates among its existing customer base.

Source: Salesforce Investor Relations

Strategic growth through M&A

One of Salesforce’s primary drivers of growth has been its strategic approach to mergers and acquisitions. Over the past several years, the company has made several high-profile acquisitions that have significantly enhanced its market position and expanded its product portfolio. In 2018, the acquisition of MuleSoft for $6.50 billion allowed the company to integrate more seamlessly with various applications, streamlining business processes. The $15.70 billion Tableau deal in 2019, one of the largest in the company’s history, further strengthened its data visualization capabilities, making it a powerhouse in the analytics space.

In 2020, Salesforce made another significant move by acquiring Slack for $27.70 billion, positioning itself as a key player in enterprise collaboration. The financial performance of the company over the last five years underscores the success of these acquisitions, demonstrating its ability to leverage M&A for growtha positive indicator for the future as well, especially given its strong balance sheet.

AI integration

Salesforce has made significant strides in developing its Data Cloud and multi-cloud offerings to unify customer data across platforms. However, it is clear the company does not yet possess the same robust ecosystem advantage as Microsoft (NASDAQ:MSFT) when it comes to monetizing AI in the short term. Salesforce CEO Marc Benioff has indicated that while the company is optimistic about the long-term potential of generative AI within its applications, these features may not significantly impact revenue until 2025 or 2026. Despite this, the company remains confident in the enterprise potential of its platform, given the massive amount of data it manages. However, the ongoing experimentation with AI solutions suggests monetization could be slower than anticipated, leading to a more gradual growth trajectory even for industry leaders like Salesforce.

Salesforce’s Data Cloud allows organizations to ingest, unify and process data from various departments and third-party cloud solutions. Powered by an AI-driven data engine, it analyzes metadata in real-time, providing valuable insights to support sales, marketing and customer service workflows. I believe that Data Cloud will play a pivotal role in helping Salesforce sustain growth rates in the low double-digit range and maintain its dominant market share. The platform has already shown promising results, with 90% year-over-year growth and a projected contribution of $400 million in 2024. Although Data Cloud’s impact may seem relatively small compared to Salesforce’s nearly $40 billion top line, I expect it to become a crucial driver for protecting and maintaining its market-leading position in the long run.

Financial performance and outlook

In the first quarter, Salesforce reported a robust 11% year-over-year increase in revenue, reaching $9.10 billion, with subscription sales climbing 12% to $8.50 billion. While there was a minor dip in expected sales, the company still managed to beat earnings per share consensus by nearly 3%, underlining its strong profitability. Although the forecasted sales growth of 7% to 8% for the second quarter disappointed some investors, Salesforce maintained its annual growth forecast of 8% to 9%, providing reassurance about its future performance. On the earnings call, management highlighted the rapid growth of the Data Cloud, the fastest-growing product in the company’s history, positioning it as the next major growth driver.

Source: Salesforce Investor Relations

Further, Salesforce has demonstrated strong expense management, with non-GAAP operating margins expanding by 450 basis points year over year to 32.10%. For context, the margin in the same quarter two years ago was just 17.60%. While Wall Street has been focused on top-line growth, I believe the significant improvement in profitability is noteworthy. Additionally, current remaining performance obligations grew by 10% year over year to $26.40 billion, while free cash flow surged 43% to $6.08 billion during the quarter.

As a nearly $40 billion entity, it is expected that growth rates will eventually moderate rather than continue accelerating as if Salesforce were still a young, emerging software company. However, Salesforce’s expanding profit margins set it apart from faster-growing peers trading at similar multiples. Contrary to market concerns, I see no cause for alarm in its first-quarter revenue miss, which was a negligible $14 millionjust 0.15% of the company’s first-quarter revenue, almost invisible in the grand scheme. What matters most to me is that revenue continues to grow at a decent pace (as it is now), while demonstrating significant operating leverage, in order to drive earnings per share expansion. I anticipate the market will eventually shift its focus from top-line growth rates to the quality of Salesforce’s revenue and earnings base.

Salesforce continues to heavily invest in innovation and acquisitions while effectively managing its financial resources. The company has struck a balance between investing in innovation and returning capital to shareholders, as evidenced by the $2.20 billion in stock buybacks during the first quarter.

The balance sheet also remains robust despite significant investments, buybacks and dividends. The company ended the quarter with $17.70 billion in cash, $5 billion in strategic investments and $8.40 billion in debt, maintaining its strong net cash position. This financial strength is especially remarkable given the significant acquisitions the company has made in recent years, while still maintaining the capacity to pursue further growth through M&A.

To sum up the financial analysis, I see no reason to waver on my bullish stance toward Salesforce. The recent selloff appears to be mere noise, as the company’s fundamentals remain rock-solid and continue to improve. Its top-line growth is healthy, operating leverage is driving earnings expansion and its financial position is formidable.

Valuation perspective

Salesforce’s growth rate may not be astonishing at the moment, but its strong profitability significantly reduces the risk for investors. Currently priced at $263 per share, the stock is trading at a forward earnings multiple of 24.60, which is notably below the peer average of approximately 30. This discrepancy positions the stock as undervalued in the market.

Considering its net cash balance sheet and highly recurring revenue base, I believe a slightly higher multiple of 33 times earnings is justifiable. Given the company has historically traded at an average of 46 over the last five years, this adjusted multiple highlights the stock’s potential value. Using a 33 times earnings multiple, Salesforce’s intrinsic value would be around $352, indicating the stock is undervalued by about 34% at current levels. Even with a more conservative multiple closer to the peer averagesay 27Salesforce’s intrinsic value would still be approximately $288, suggesting the stock is undervalued by around 10%.

Additionally, a discounted cash flow model based on earnings per share without non-recurring items, using a WACC of 10% and a terminal growth rate of 4% post-initial growth phase, yields a fair value of approximately $308.

This provides a margin of safety of around 15% from the current price, indicating further upside potential. Salesforce’s current free cash flow yield, based on trailing 12-month free cash flow, stands at 4.84%. This yield surpasses that of a risk-free government bond, offering investors a more attractive return while also benefiting from Salesforce’s future growth potentialan opportunity that risk-free bonds do not provide.

In my view, Salesforce is a bargain with a minimum intrinsic value of $288 and an optimistic valuation reaching up to $352. Long term, the company has significant opportunities to expand and scale its software, cloud and data platforms, and the current valuation offers a solid margin of safety compared to other companies trading at similar multiples.

Conclusion

In summary, Salesforce’s position as a market leader in the CRM space, combined with its solid financial performance, strategic investments and attractive valuation, makes it a compelling investment opportunity. While the recent sell-off may have raised concerns among some investors, I see it as an overreaction given the company’s strong fundamentals and future growth potential.

Salesforce’s focus on expanding its AI capabilities, coupled with its proven ability to integrate acquisitions successfully, positions it well to capitalize on the next wave of technological advancements. With a robust balance sheet and a disciplined approach to capital allocation, I remain bullish on the stock and believe the current valuation presents a favorable entry point for long-term investors.

This article first appeared on GuruFocus.