If you buy and hold a stock for many years, you’d hope to be making a profit. Furthermore, you’d generally like to see the share price rise faster than the market. But Salesforce, Inc. (NYSE:CRM) has fallen short of that second goal, with a share price rise of 84% over five years, which is below the market return. Over the last twelve months the stock price has risen a very respectable 17%.

Since it’s been a strong week for Salesforce shareholders, let’s have a look at trend of the longer term fundamentals.

See our latest analysis for Salesforce

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

During five years of share price growth, Salesforce achieved compound earnings per share (EPS) growth of 30% per year. This EPS growth is higher than the 13% average annual increase in the share price. So one could conclude that the broader market has become more cautious towards the stock.

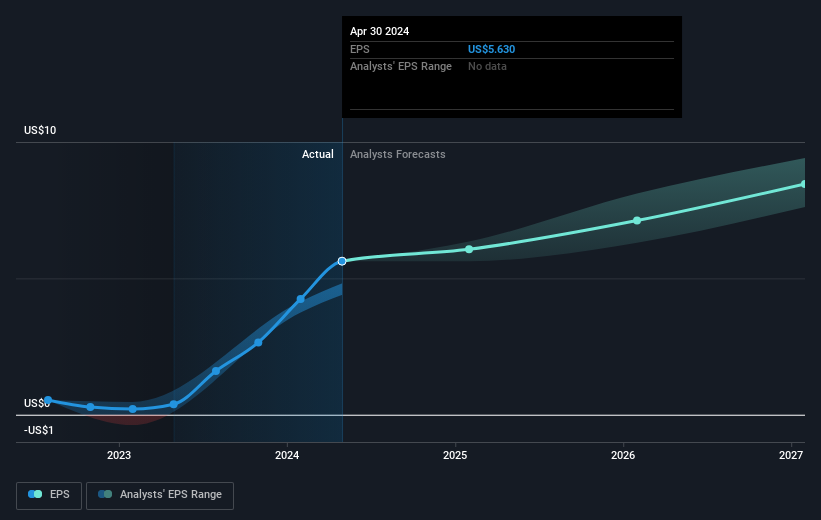

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

It’s probably worth noting we’ve seen significant insider buying in the last quarter, which we consider a positive. That said, we think earnings and revenue growth trends are even more important factors to consider. Dive deeper into the earnings by checking this interactive graph of Salesforce’s earnings, revenue and cash flow.

A Different Perspective

Salesforce’s TSR for the year was broadly in line with the market average, at 17%. That gain looks pretty satisfying, and it is even better than the five-year TSR of 13% per year. Even if the share price growth slows down from here, there’s a good chance that this is business worth watching in the long term. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider risks, for instance. Every company has them, and we’ve spotted 1 warning sign for Salesforce you should know about.

Salesforce is not the only stock that insiders are buying. For those who like to find lesser know companies this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]