Knowing when to buy is critical to maximize returns.

Deciding when to purchase a stock is perhaps an investor’s most challenging decision. This is especially true with newly public, unique companies in high-growth industries, like Arm Holdings (ARM -0.41%). Arm Holdings stock has more than doubled since its initial public offering (IPO) around nine months ago, and many investors are eager to own this company. But is now a good time?

Several factors make timing purchases difficult:

- We all assume, intellectually, that the best time to buy is when the market or stock falls, but most people have difficulty pulling the trigger when the time comes because they fear further losses.

- Newer companies and tech companies are notoriously difficult to value. Traditional metrics like price-to-earnings (P/E) ratios may be great for some established names but are often of little value to today’s up-and-comers. Since going public, Amazon‘s average P/E is well over 200 (and only this year has dropped to a more reasonable 50), but the stock is up 6,700%.

- You may not have funds available when opportunity knocks. Life is expensive these days, and most people aren’t sitting on a pile of cash waiting for their favorite stock to plunge.

Luckily, there are strategies to help. First, let’s see what makes Arm so enticing.

What does Arm do?

Semiconductors make computing possible. They are components of central processing units (CPUs) and graphics processing units (GPUs), deeply embedded in daily life. Case in point, Arm-based CPUs power 99% of the world’s smartphones, and Nvidia‘s spectacular results are fueled by its advanced GPUs and components used by data centers.

However, there is a key distinction: Arm doesn’t manufacture chips; it designs advanced “architecture” and receives royalties and license fees from the tech companies that use the technology in their products. For instance, an Arm customer that sells smartphones pays Arm a royalty for each phone sold. This distinction is one of the things that makes Arm an attractive company and stock.

Is Arm stock a good buy now?

Since Arm does not manufacture chips, it is spared a lot of expenses and investment in property and equipment. Manufacturing facilities are expensive; ask other semiconductor companies. To illustrate, the globe’s largest manufacturer, Taiwan Semiconductor Manufacturing, has a gross margin of around 50% and a free cash flow margin near 20%, while Arm’s margins run near 95% and 30%, respectively. This makes Arm’s business model extremely attractive because a larger percentage of cash goes right into the company’s pocket as revenue grows. Revenue hit $928 million in the fourth quarter of fiscal 2024, ended March 31, on 47% year-over-year growth. For the full fiscal year 2024, the company produced $3.2 billion in sales and expects $3.8 billion to $4.1 billion in the upcoming fiscal year.

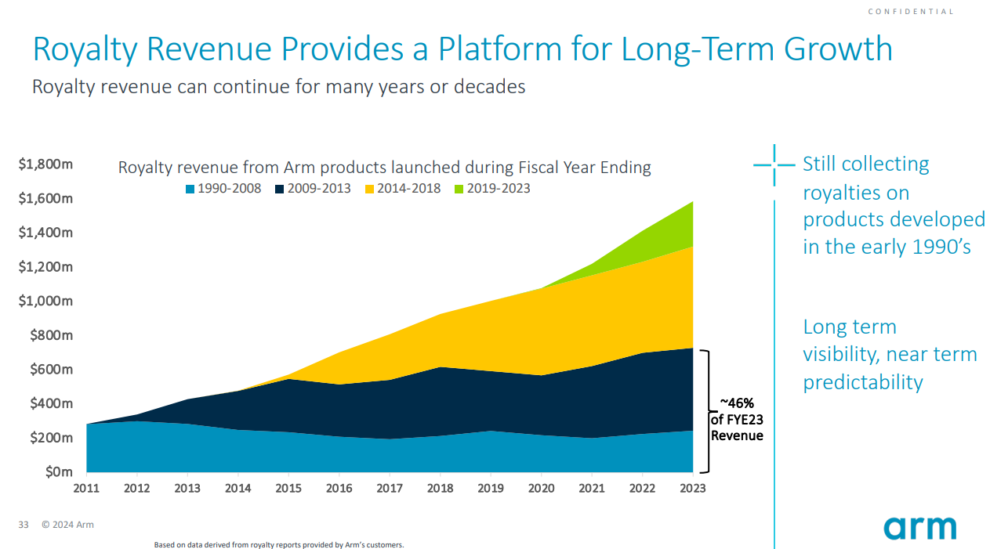

Another reason that Arm’s model is attractive is because it still collects royalties from products produced more than 30 years ago, as shown below.

Image source: Arm Holdings.

This means two things. First, the new, advanced designs don’t cannibalize sales of prior designs because they have different applications, like artificial intelligence (AI), cloud, and advanced automotive systems. Second, royalties from decades-old designs are almost all profit now because the research and development costs already happened.

Arm is a terrific company to own for the long run. The big question is whether to buy now or wait for a pullback after the stock’s precipitous rise, as shown below.

By most traditional metrics, Arm stock looks overvalued. However, the company’s long-term potential and growth performance are critical, as with Amazon.

Here are three methods to buy the stock while minimizing the risk of overpaying.

- Buy a little, and wait for a drop to buy more. You will make some money if the stock price increases and only have a little exposure if it drops. The drop will be an opportunity to lower the average trade price. The downside is that you would only have a small position if it doesn’t dip significantly.

- Be patient. Buying the dip means the investor waits patiently for a significant pullback and then pounces. The drawback, of course, is that the stock may not cooperate. For instance, if the stock moves up another 40%, a 20% correction is still well above the current price.

- Dollar-cost averaging (DCA) is a terrific risk-mitigation strategy in which the investor buys consistently over time, for example, $200 per month. DCA allows the investor to take advantage of ebbs in the stock price without much guesswork and timing.

Arm Holdings is a terrific company with an enviable business model in an excellent industry. But these stocks don’t come cheap. Jumping in head first is a risky strategy. Consider one of the more cautious ways to buy above.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Bradley Guichard has positions in Amazon, Arm Holdings, and Nvidia. The Motley Fool has positions in and recommends Amazon, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.