After the chipmaker’s massive run-up over the past two years, what’s the right move for investors now?

Nvidia (NVDA -0.01%) has been one of the best-performing stocks on the market over the past two years, and the catalysts that drove it higher are still present. But after its strong run-up, is Nvidia stock still a smart buy at its current level, or would those who hold shares be advised to sell and take some profits?

There are valid arguments for both views.

The sell argument: How long will this demand wave last?

Nvidia’s rise has been directly tied to the artificial intelligence (AI) arms race. Its primary products are graphics processing units (GPUs) — parallel processors that excel at handling large and complex computing tasks that are easily broken down into many smaller ones that can be handled independently and simultaneously. Connect GPUs in clusters and you end up with a computing platform that can process certain types of incredibly complex workloads at blistering speeds — and these are just the sorts of workloads that AI systems create.

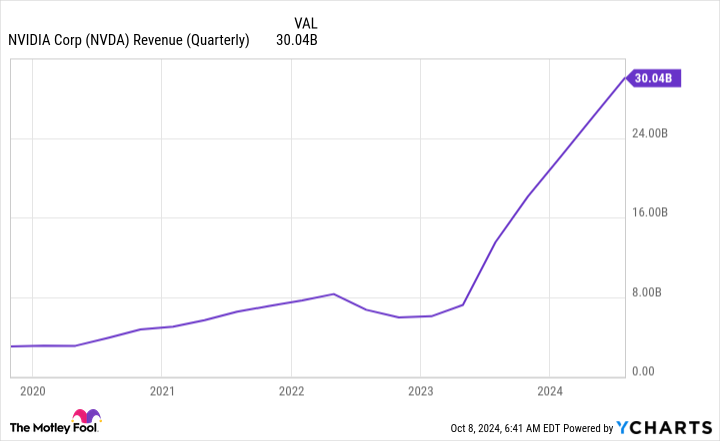

As AI companies and cloud computing providers rushed to get in front of the emerging demand for processing power, Nvidia’s sales went through the roof. In the past couple of years, quarterly revenues have often tripled on a year-over-year basis. However, its stellar growth is starting to slow slightly due to tougher annualized comparisons. This growth slowdown makes sense, but the bigger question is, can Nvidia maintain its overall sales at these levels?

Because companies are buying these GPUs to rapidly build their AI computing capacity, there is going to be a time when the demand will be satisfied. At that point, Nvidia’s sales may crater, as companies will only be buying replacement GPUs or making gradual capacity increases. This could be a huge problem for Nvidia, as its revenue levels in its latest quarters are far above where they have been in the past.

NVDA Revenue (Quarterly) data by YCharts.

This also highlights the cyclical nature of the chip business. Nvidia has gone through multiple boom-and-bust cycles in its life as a company. If AI-related demand wanes, investors could be in a rough spot.

But has Nvidia built up enough of a sales base to compensate for that cyclicality?

The buy argument: New technology will spur further demand past 2025

GPUs don’t last forever. They generally need to be replaced after about three to five years, which means that if the companies that have been building out their computing infrastructure recently want to maintain that processing power over the long term, they will have to regularly fork out massive chunks of money on new hardware.

We’re two years into the AI build-out already, and many companies are still scaling up their AI computing power, so 2025 will be another year of strong demand. That gets investors to 2026, at which point the natural replacement cycle starts for the GPUs that were purchased at the start of the generative AI era. But there could also be more reasons for companies to upgrade.

First, the semiconductor chips within these Nvidia GPUs are produced by Taiwan Semiconductor Manufacturing (TSM 2.71%). Taiwan Semi is always innovating on the process node front, allowing chip designers like Nvidia to create denser, higher-performance chips.

TSMC expects that its chips built using its next-generation N2 process node will be 25% to 30% more power efficient than prior-generation chips when configured at the same speeds. Energy costs are a huge operating expense for server farms, so some customers may choose to upgrade for that reason, regardless of whether they need more computing power or not. The N2 manufacturing lines aren’t expected to start production until 2025, which likely means Nvidia GPUs built on them won’t make their way to its customers in quantity until 2026.

Meanwhile, Nvidia is just launching its Blackwell architecture GPUs, which will replace the Hopper architecture upon which it has built its current top-of-the-line chips, and the improvements are astounding. Blackwell’s architecture is four times faster than Hopper’s, allowing AI companies to create more complex models faster.

The combination of all these factors points to demand remaining strong well past 2026. In other words, the market probably isn’t peaking any time soon. This is key, as Nvidia’s forward price-to-earnings ratio has already reached levels that are starting to look reasonable, at least relative to how fast it’s growing.

NVDA PE Ratio (Forward) data by YCharts.

Trading at 45 times forward earnings, Nvidia stock is far from cheap, but it’s putting up strong growth, so this valuation is acceptable.

Investors’ decisions about whether to buy or sell Nvidia stock today should be based on how they expect the company’s business to be faring in 2026 and beyond. There are enough catalysts out there that Nvidia’s growth should last far beyond 2026, and with the upgrade cycle, it should be able to maintain its newfound revenue levels.

As a result, I think Nvidia’s buy case is greater than its sell case today.

Keithen Drury has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.