These stocks offer incredible growth opportunities.

I don’t really think any investor should forget about Amazon, as if anyone could. Amazon has incredible future potential in e-commerce, artificial intelligence (AI), and more. Amazon stock is up 31% this year, and it’s the leading player in two of the world’s most important industries right now. Sixty-three out of 67 covering analysts call Amazon stock a buy, with the other four calling it a hold.

However, the staggering gains investors have benefited from in the past aren’t likely to be reproduced; Amazon is already a huge company, and as much potential as it has, it’s building on a huge foundation. Doubling or tripling its business at current levels is going to take longer than it did when Amazon was getting started.

Investors looking for supercharged growth are more likely to find it in younger stocks with massive growth opportunities. If you’re looking for a candidate for your portfolio, I have some ideas for you. Consider e.l.f. Beauty (ELF -2.02%) and Revolve Group (RVLV 0.56%), two young companies that are leveraging digital platforms to compete with industry leaders.

1. The new leader in cosmetics

The beauty industry has been dominated by a few giants for decades already, but the digital era is bringing down the hierarchy. Industry leader Estée Lauder has acquired luxury brands for years, concentrating its dominance, while L’Oréal, Revlon, and a few others have been the top names in mass beauty, also buying up the competition to consolidate. They have made for formidable competition and strong barriers to entry.

e.l.f. has carved out a niche by focusing on digital and social media and creating an omnichannel strategy that speaks to its young target market. It’s still a small outfit compared to its larger peers, with a fraction of their sales, but it’s growing much faster than almost any other cosmetics brand today. It has captured market share and moved up from the No. 5 spot to the No. 2 spot in mass cosmetic brand dollar share from 2022 to the most recent quarter, and its skincare business has increased 45% at the same time that the overall industry is up 1.2%.

In an economic climate that’s still under pressure, e.l.f. is demonstrating incredible resilience. Sales increased 50% year over year in the 2025 fiscal first quarter (ended June 30), and gross margin expanded by 0.8 percentage points to 71%. Operating income decreased, as did earnings per share (EPS), but both were positive and healthy, and management raised its outlook for full-year revenue, operating income, and EPS.

Here are how Amazon’s and e.l.f.’s sales growth stack up for the past four quarters:

| Metric | Q3 24 | Q2 24 | Q1 24 | Q4 23 |

|---|---|---|---|---|

| Amazon revenue growth | 11% | 10% | 13% | 14% |

| E.l.f. revenue growth | 50% | 77% | 85% | 76% |

Data source: Amazon and e.l.f. quarterly reports. E.l.f. quarters are Q1 25, Q4 24, Q3 24, and Q2 24.

Part of the reason e.l.f.’s earnings were lower is its acquisition of a new skincare brand, Naturium, which is already adding a lot to the business; it accounted for 16 percentage points of the first-quarter sales increase. This is short-term pressure for long-term gain, and management is expecting an increase in EPS for the full year.

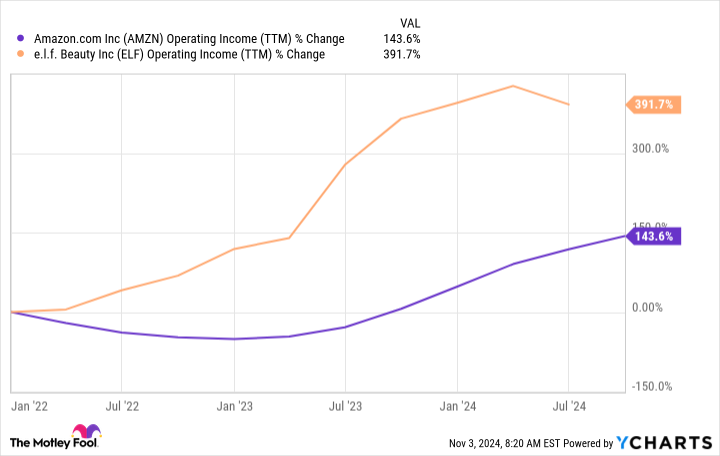

Its earnings how outpaced Amazon’s over the past three years:

AMZN Operating Income (TTM) data by YCharts.

e.l.f. is growing much faster than Amazon, but its stock trades at a forward one-year P/E ratio of 25, or cheaper than Amazon’s 33. With e.l.f. in high-growth mode, and plenty of market share to conquer, e.l.f. stock could be an incredible addition to a growth-oriented portfolio.

2. Taking over in fashion

Just like e.l.f. has leveraged its digital, social media-powered platform to become a leader in beauty, Revolve has developed an artificial intelligence (AI)-based platform to emerge as a strong contender in fashion. It also has a large social media presence and works with influencers and celebrities, and its all-digital business lends itself to profitability.

Like most retailers, it has struggled through inflation. It reaches a mass audience of fashion aficionados who are willing to pay full price for trendy clothing, and they’ve been cutting down. But the tide might be finally starting to turn.

Sales were up 3% year over year in the second quarter, the first year-over-year increase since 2022, and net income more than doubled from last year. As usual, the customer metrics tell the real story. Revolve continues to add active customers despite the challenging operating environment, with a 5% increase year over year, and average order value crept up 2%.

Part of the positive trends are due to a decrease in the return rate, which bodes well for the future. Management has made key strategic efforts to curb the return rate that at the same time elevate the shopping experience, like improving size guidance and focusing personalization on merchandise less likely to be returned. It also developed an internal search function that yields higher sales generation at lower costs.

Revolve’s sales are still a fraction of sales from apparel leaders like Gap and Nike, and as a smaller player with trends moving in its favor, it has much more room to grow. As inflation moderates and interest rates do gown, it’s likely to start reaching higher. It could also outperform as we get closer to the all-important holiday season.

Since Revolve has been experiencing massive pressure in the current operating environment, you’d have to go back to pre-inflation to see how it has edged out Amazon under better conditions:

AMZN Revenue (Annual) data by YCharts.

You would also have to imagine that it could go back there, and now that revenue is picking up again, it’s demonstrating signs that it can.

Revolve stock trades at a forward, one-year P/E ratio of 36, or slightly more than Amazon’s. It’s only a great deal if you can envision the potential in a few years from now, and if you can, you might see why it deserves that premium.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Nike, Revolve Group, and e.l.f. Beauty. The Motley Fool has a disclosure policy.