(Bloomberg Opinion) — Russia’s most valuable listed company is testing the limits of corporate reinvention. Traditional lenders everywhere are adding payments apps and digital banking offerings to see off tech upstarts. State-owned giant Sberbank PJSC wants to go much further to become Russia’s answer to Amazon, Alibaba, Tencent and, well, Sberbank — all rolled into one. Watching long-time boss Herman Gref address investors this week in the Silicon Valley uniform of jeans, t-shirt and white trainers on a circular stage against a changing virtual background, it was hard to imagine this was once the Soviet savings monopoly, a monolith better known for bureaucracy and sullen service than tech prowess. In September, it dropped the word “bank” from corporate branding. Now, it aims to become one of the top three e-commerce players nationally by 2023 — delivering groceries and more alongside its regular banking, wealth management and insurance business.

The logic isn’t hard to understand. Facing limits on its reach abroad and low interest rates that could weigh on margins for years, Sberbank wants to make more of its clout at home, where almost two-thirds of Russians are clients. Rival state-owned lender VTB Group too has diversified, expanding into grain trading. Yet by stretching into everything from cloud services to food delivery, taxis and even in-house hardware, Gref is pushing not just Sberbank’s aspirations, but what Moscow overseers will allow. Oversight questions are growing, and political risk is building too.

Even if everything goes as planned, conglomerates often trade at a discount, suggesting they rarely deliver the value they should.

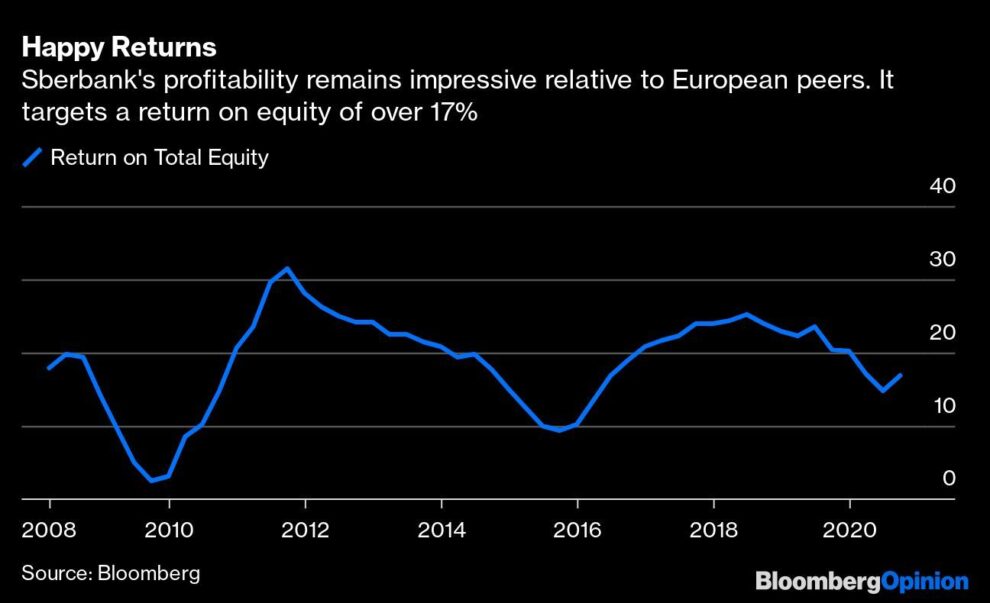

Sberbank has already seen a remarkable transformation even before this effort to compete head-to-head with the likes of its one-time partner Yandex NV. Over more than a decade under Gref, a liberal reformer and former economy minister, the bank has bolstered its bottom line, revived its operating systems and branch networks, weathered European and U.S. sanctions, and now a pandemic. Impressive, even if it has had to delay a 1 trillion-ruble ($13 billion) net profit target.

Sberbank’s banking app is the third most popular in Russia, as measured by monthly users, according to Gref. Clients are interacting with the lender more frequently. That’s good news, given engagement is a vital ingredient for any superapp-in-waiting. There’s the benefit of an extensive branch network too, in a vast country where actually making the deliveries has been a major brake on internet shopping.

Yet a state bank isn’t necessarily the right owner for many of these businesses. Yes, the race is open for online shopping dominance in Russia, a country where few international tech heavyweights have made headway. But e-commerce has a propensity to gobble up cash that may extend beyond the 4% of equity signaled by Sberbank for the three-year period. The bank has already spent some $2 billion on acquisitions and tech to build a non-banking business that includes online cinema Okko and media group Rambler.

Despite Gref’s reassurances otherwise, it’s unclear the bank can expand swiftly on all of these fronts without adding risk to the financial business where Sberbank still has room to grow in everything from loans to insurance. After all, banking will still account for roughly 70% of net operating income in 2023. Conglomerates elsewhere offer cautionary tales.

Russia’s cautious central bank has already warned about the risk of creating new monopolies and fretted about the rapid expansion into non-financial services. That may well translate into tougher disclosures standards or capital requirements. Sberbank, after all, holds nearly half of Russia’s retail deposits. It may have looked to Asian heavyweights for inspiration, but there it was big tech that drove the disruption, not the other way around. Most of those companies, like Grab or Gojek in Southeast Asia, have expanded through partnerships, rather than full ownership. The going hasn’t been smooth either, as Ant Group’s initial public offering showed.Finally, there’s Kremlin risk. Russia wants and badly needs digital innovation, but state coffers need dividends too. Sberbank says it will pay out half its earnings, and any sign of that sum shrinking finance tech experiments may prove politically costly. So too will any slip-up that hurts consumers.Tech is necessary, tempting and potentially accretive. It can also prove a distraction, with economic uncertainty ahead, for a major lender that still has room to grow within financial services. Watching Sberbank has reminded me of a conversation I had a year or so ago with an Uber executive. When I asked why superapps weren’t catching on faster outside Asia, he paused. Sometimes, he replied, just because you can, doesn’t mean you should.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.

For more articles like this, please visit us at bloomberg.com/opinion

Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.