Supermicro’s stock has mismatched expectations.

Stock splits have been fairly common among companies associated with artificial intelligence (AI). This is because they have performed so well over the past year-and-a-half that their stock prices have reached a level where a split is a good idea.

One company that has recently joined this club is Super Micro Computer (SMCI 1.39%), commonly known as Supermicro. It announced a 10-for-1 stock split effective Oct. 1, which will take its stock price from around $630 to $63 per share.

While the stock split is exciting news, I think there is an even better reason to buy the stock now before the split occurs.

Its data center products have been in huge demand

While Nvidia may get all the headlines because it is associated with the AI infrastructure being built out, many more companies are benefiting from the same tailwinds. Supermicro is one of them as its products, ranging from data center hardware to complete racks, are in high demand.

While many companies provide similar products to Supermicro’s, they stand out among the competition for two reasons. One, Supermicro’s servers are highly configurable and can be tailored to suit a workload of any size. Two, Supermicro’s servers are more energy-efficient than the competition, which is a huge consideration because energy input costs are significant over the life of the server.

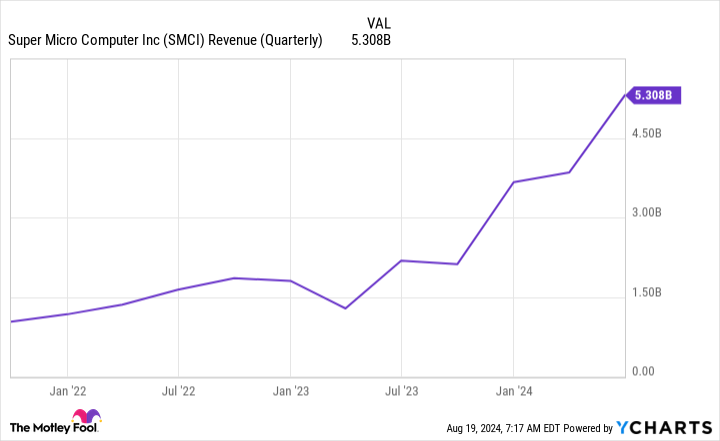

These advantages have caused Supermicro’s revenue to explode over the past year, and more growth is slated to occur as well.

SMCI Revenue (Quarterly) data by YCharts

Looking ahead to its fiscal 2025’s first quarter (ending Sept. 30), management expects $6 billion to $7 billion in revenue, ranging from 183% to 230% growth. For fiscal 2025, it anticipates $26 billion to $30 billion in revenue, which would be 74% to 101% year-over-year growth.

That is significant progress and a huge reason to invest in the stock right now. At the end of fiscal 2023, Supermicro had a long-term annual revenue goal of $20 billion. And at the end of fiscal 2023’s second quarter, this target was only $10 billion.

Clearly, this market is rapidly expanding, and the appetite for Supermicro’s products is growing alongside it. However, this target has once again been raised in its most recent results to an astonishing figure of $50 billion in annual revenue. That’s a massive upside from its current projections, and I think it is a phenomenal reason to own the stock, as Supermicro has consistently reached its long-term targets.

However, following its Q4 2024 earnings announcement, the stock plunged 20%. This seems like an odd reaction, but that’s because another important metric saw some weakness.

The stock is priced fairly cheap compared to peers

While revenue growth is important and grabs headlines, investors must also see growing profits. Supermicro’s margins plunged in Q4 due to new product launches, and that weakness is expected to last for most of fiscal 2025. However, this drop is short-sighted thinking because if Supermicro recovers its margins by the end of fiscal 2025, it will represent a massive value opportunity.

SMCI PE Ratio (Forward) data by YCharts

Right now, the stock trades at 18.4 times forward earnings. Compared to most stocks in the market, this figure is pretty cheap. It also indicates 72% earnings growth over the next year.

Supermicro’s management has already projected 74% revenue growth on the low side, so its earnings would have to stay at this lower state for the entire year for the current valuation to make sense.

This disconnect represents a strong buying opportunity for the stock, and a patient investor could see a satisfying return from an investment if Supermicro’s margins recover over the next year.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.