The S&P 500 (^GSPC -0.39%) is sitting on a gain of 28% in 2024, which follows a 26% return in 2023.

Back-to-back annual gains of at least 25% have only happened once since the S&P 500 was established in 1957. The index rose by 33% in 1997 and then by 29% in 1998, fueled by the dot-com bubble, which drove stock valuations to dizzying heights.

There is nowhere near as much exuberance in the stock market today, but the technology sector is driving the S&P higher once again thanks to emerging themes like artificial intelligence (AI). If the index does end 2024 with a gain of at least 25%, here’s what history suggests could happen next.

More upside might be around the corner

The S&P 500 soared by 21% in 1999, adding to its incredible gains from 1997 and 1998. That suggests another strong year in 2025 isn’t out of the question, but history doesn’t always repeat.

There was a level of irrationality during the dot-com boom that isn’t present today. Investors were flooding into internet companies even if they had no revenue — and many didn’t even have a concrete business plan.

Pets.com was one of the biggest failures of that era. It raised $82.5 million from investors during its initial public offering in 2000, and it was bankrupt just nine months later.

The stock market is on a much firmer footing this time around. Nvidia is leading the AI revolution, and not only does it generate truckloads of revenue, but it’s also highly profitable. According to Wall Street’s average forecast (provided by Yahoo!), Nvidia is on track to deliver $129 billion in revenue during fiscal 2025 (which ends in January) — an increase of 111% from the prior year.

Here’s the point I’m making: Predicting the end of a speculative frenzy (like the dot-com bubble) is practically impossible, so the fact the S&P 500 rose in 1999 isn’t a good indication of what could happen in 2025. However, the S&P could deliver a positive return next year because the largest companies in the index are generating so much growth.

2025 won’t be 1999, but valuations are definitely stretched

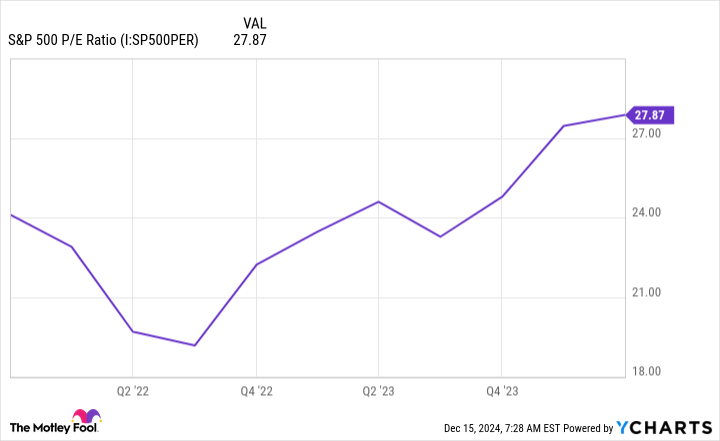

This is the challenging part when it comes to generating further gains immediately after two strong years. The S&P 500 currently trades at a price-to-earnings ratio (P/E) of 27.9, which is a 54% premium to its long-term average of 18.1.

S&P 500 P/E ratio; data by YCharts.

But valuation metrics are not reliable timing tools, because markets can remain expensive for much longer than investors expect. During 1999, the S&P 500 actually reached a P/E of 34, meaning the index continued to climb despite being significantly overvalued relative to its historical average (although it eventually crashed during a three-year span from 2000 to 2002).

Therefore, investors shouldn’t rush to sell their stocks just because the market looks expensive today. In fact, there are some real tailwinds that could drive further returns from here.

First of all, the U.S. Federal Reserve is cutting interest rates. That reduces the yield on risk-free assets like cash and Treasury bonds, which makes growth assets like stocks appear more attractive, even at elevated valuations. Plus, lower rates let companies borrow more money to accelerate their growth, and their interest cost also falls, boosting their earnings.

Second, AI should remain a catalyst for some of the biggest companies in the S&P. According to Morgan Stanely, four companies — Microsoft, Amazon, Alphabet, and Meta Platforms — will spend a combined $300 billion on AI infrastructure during 2025 alone.

They are spending that money because they expect to earn a significant financial payoff in the future. But in the shorter term, that spending will benefit chipmakers and suppliers of data center components like Nvidia, Advanced Micro Devices and Broadcom, which will contribute to more gains in the S&P 500.

Image source: Getty Images.

Volatility could rock the stock market next year

Politics might be something for investors to keep in the back of their minds as we enter the new year. The incoming Trump administration will introduce economic policies very different from the Biden administration’s, which could spark short-term volatility as markets adjust.

During Trump’s previous term, he imposed tariffs on steel and aluminum imports from almost every country in the world. Some countries, including China, retaliated with tariffs of their own, and investors were fearful of a potential trade war. That was a key reason the S&P 500 almost slipped into a bear market during 2018.

Since it appears tariffs are at the top of Trump’s agenda once again, I won’t be surprised to see the S&P 500 temporarily move lower after he takes office on Jan. 20. However, that might be a blessing in disguise if it brings valuations down to more reasonable levels, because it would create a buying opportunity for long-term investors.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.