Try to keep a healthy dose of skepticism — but these two companies could be on the brink of shocking investors.

Long-term investing requires optimism. This is why investing in turnaround opportunities is intrinsically dangerous. The danger to investors is the failure to properly assess the risks because they look at the opportunity through rose-colored glasses. Their optimism emphasizes the good possibilities instead of the bad ones and makes it harder to develop a balanced assessment.

Businesses sometimes perform poorly and need turnarounds. I’d say that’s the case with PayPal (PYPL -1.47%) and Advance Auto Parts (AAP -0.80%) right now. Of course, every struggling business institutes a turnaround plan at one time. Just as many fail as succeed.

Let’s look at the optimistic scenario for each of these struggling companies, but keep in mind what could go wrong as well. After a review, it might become clearer whether these two are on the brink of success.

How PayPal could quickly surprise

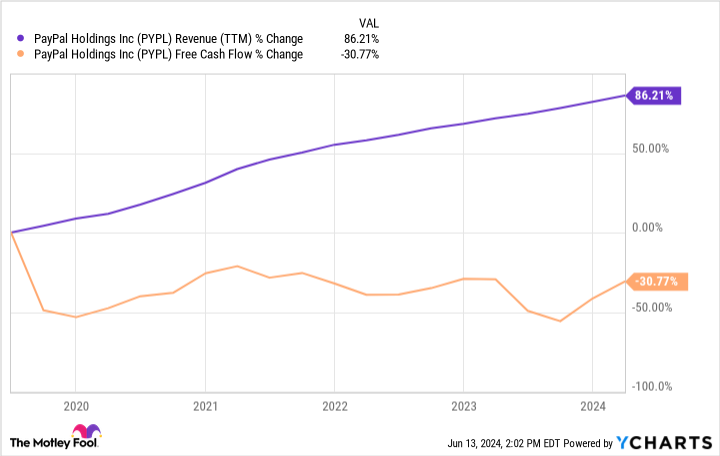

I can sum up PayPal’s problems in a single chart. While revenue has grown and is still growing, its growth has come from lower-margin opportunities. Consequently, revenue is up 86% over the last five years, but free cash flow is down.

PYPL Revenue (TTM) data by YCharts

On a free-cash-flow valuation basis, PayPal stock is quite cheap, trading at just 13 times its free cash flow. A more normal valuation, even for a low-growth company, is often between 15 and 20 times free cash flow. However, if PayPal can’t grow its profits — and it hasn’t been able to for some time now — then the cheap valuation is entirely befitting.

Investors seem to believe PayPal is a business in decline. But here’s one way the company could quickly improve the narrative: It just launched an advertising business. Digital advertising (unlike PayPal’s other efforts in recent years) is high-margin, and the platform still has hundreds of millions of active users for businesses to advertise to.

In October 2022, Uber Technologies made the same move by launching its dedicated ad platform, which quickly became a $1 billion business. It’s worth noting that PayPal hired Uber’s architect Mark Grether to build its own offering. Therefore, someone with a quality reputation is in charge and could make things happen quickly.

It’s also worth noting what happened to Uber’s free cash flow after launching a dedicated ad platform. I’m not saying that 100% of the profit growth came from ads. But the chart below starts the day Uber launched ads, and it suggests that ads were a powerful catalyst to profit growth. Now that potential catalyst is there for PayPal.

UBER Revenue (TTM) data by YCharts

How Advance Auto Parts is completely restructuring its business for profits

Just as I believe one chart sums up PayPal’s problems, so too can one chart sum up the big issue at Advance Auto Parts. The chart below shows that 20 years ago, the operating margins for Advance and competitor O’Reilly Automotive were in the same ballpark. But around 2013, margins started to slip for Advance and have never recovered. There’s a perfectly good explanation for this.

AAP Operating Margin (TTM) data by YCharts

In 2013, Advance acquired Carquest. In isolation, this wasn’t the problem. But as the publication Supply Chain Dive points out, Advance has basically operated two disconnected supply chains ever since the Carquest acquisition. That’s extremely inefficient, and it’s not surprising that the company’s profit margins slipped steadily, whereas margins for O’Reilly went higher and higher.

Fortunately for shareholders, Advance hired a supply chain expert when it hired new CEO Shane O’Kelly from HD Supply in August. As O’Kelly pointed out in the conference call to discuss financial results for the first quarter of 2024, the company has 38 distribution centers right now, and it only needs 14 — that’s not a typo.

I believe PayPal’s turnaround could be swift. In contrast, the turnaround for Advance would likely take longer. Completely consolidating an inefficient supply chain will simply take time. And it will cost money — the company expects $200 million to $250 million in capital expenditures in 2024 alone.

However, if Advance’s profit margins are truly down in the dumps because of an inefficient supply chain, then the future for investors is extremely promising. Consider that the company expects well over $11 billion in net sales this year. If it could boost its operating margin to 10% — which would still be half of the margin for O’Reilly — then the company would have over $1.1 billion in annual operating profit.

For perspective, Advance’s market valuation is only $3.8 billion as of this writing. If it pulls off its turnaround, then the stock has a path to doubling or tripling over the next several years, which would almost assuredly beat the returns for the S&P 500.

Of these two, PayPal’s turnaround might be easier and quicker. However, Advance stock could have higher upside, due to how cheap shares are right now compared to its potential.

Jon Quast has positions in Advance Auto Parts. The Motley Fool has positions in and recommends PayPal and Uber Technologies. The Motley Fool recommends the following options: short June 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.