The stock has been falling since July.

The investing world can’t stop talking about Nvidia. The chipmaker was briefly the largest company in the world by market cap and has seen soaring profits due to the insatiable demand for its artificial intelligence (AI) semiconductor products. But this isn’t the only company benefiting from the AI revolution.

Enter Taiwan Semiconductor Manufacturing Company (TSM 4.13%), otherwise known as TSMC. The manufacturer of computer chips for Nvidia has seen its shares fall from their high in July after slower-than-expected revenue growth. Let’s see if this presents a buying opportunity for investors focused on the long-term potential of AI.

Building the world’s most advanced computer chips

Unlike legacy computer chip manufacturers such as Intel, Nvidia doesn’t make the chips it designs. The expensive manufacturing is outsourced to third parties that focus solely on manufacturing and assembling computer chips.

TSMC is widely regarded as the best in the world at making advanced computer chips and is a key supplier for Nvidia and many other semiconductor design firms. Without TSMC, the advanced chips from Nvidia don’t actually hit the market. It’s that simple.

This is known as the foundry semiconductor manufacturing model. TSMC solely focuses on building chips, while other companies design them.

With some of the smartest engineers in the world and decades of reinvestment in growth, the company now commands more than 60% of the foundry market. Sixty-seven percent of its revenue comes from the three-, five-, and seven-nanometer computer chip platforms. Smaller nanometers between transistors means more density, which equals higher performance computing.

Outside of China, the only company that has reached five-nanometer chips is Samsung. Therefore, if Nvidia or anyone else wants to manufacture the most advanced computer chips in the world, it has to go to TSMC.

TSMC continues to reinvest to extend this lead while diversifying geographically outside of its home market in Taiwan, which poses a geopolitical security risk due to escalating tensions between the U.S. and China. It’s investing a total of $40 billion to build manufacturing facilities in Phoenix to give itself a footprint in the U.S.

Passing on price increases for the AI boom

Nvidia’s products are hot commodities due to the AI spending boom. This has allowed it to greatly increase prices on its advanced semiconductor products in recent years. While we don’t have exact details, TSMC, in all likelihood, will have passed on its own price increases to Nvidia since Nvidia can’t go anywhere else for the most advanced chip production in the world.

Demand and price increases for advanced computer chips are the main reason TSMC’s revenue rose 128% during the past five years. It has made up for slowdowns across other segments of the business.

The second-largest segment — smartphone revenue — fell by 1% in Q2 from Q1. High-performance computing grew by 28% quarter over quarter and now makes up more than half of TSMC’s sales.

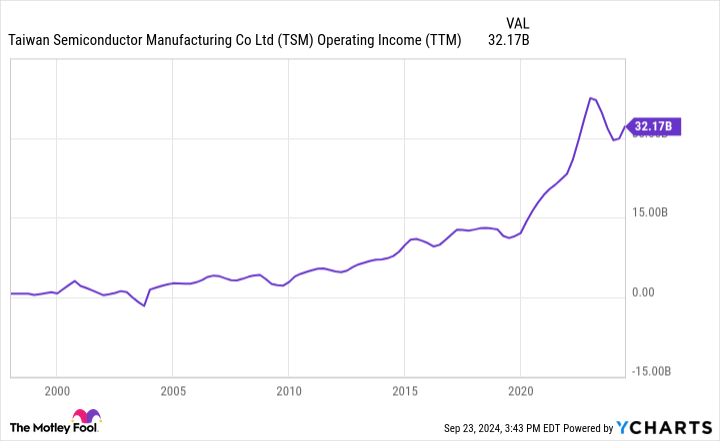

You can see this visually in a chart of TSMC’s long-term operating income. Since the pandemic, operating earnings have taken a step up and recently hit $32 billion during the past 12 months. A lot of this is due to price hikes.

TSM Operating Income (TTM) data by YCharts.

Is the stock a buy?

As mentioned in the opening section, investors have slightly cooled on TSMC stock after seeing its revenue fall slightly in August and July. Revenue in August decreased 2.4% from July, which has likely scared some people about the momentum of the AI boom.

However, I think investors need a longer-term perspective. Revenue was still up more than 30% year over year in the month, and that is with the second-largest revenue segment (smartphones) going through a rough patch.

Today, the stock has a market cap of about $800 billion. Net income during the past 12 months was roughly $30 billion and should march higher as more and more spending goes to accelerated computing products from the likes of Nvidia. Remember, TSMC is one of the only companies in the world that can build these chips.

At the current price, the stock trades at a price-to-earnings ratio (P/E) of 32. While a P/E over 30 is considered high, the company has minimal competition and a huge runway to reinvest during the next 10 years.

There’s still a lot of opportunity left in TSMC stock for those who buy and hold for the long term. This company’s earning should grow for many years to come.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.