Twilio is struggling on account of weak customer spending, but it is hoping that AI could become a savior.

This has been a terrible year for Twilio (TWLO 0.20%) investors so far, as shares of the company have fallen 20%. The cloud stock’s negative returns are in stark contrast to those of the broader technology sector, which has been heading higher this year following a stellar 2023, driven by catalysts such as artificial intelligence (AI).

Weak spending by customers on its products has been a big reason behind Twilio’s poor stock market performance in 2024. The company, whose services allow organizations to connect with their customers through multiple channels such as text, voice, and video, has been reporting anemic growth in recent quarters.

Twilio’s results for the first quarter of 2024 were no different. The stock witnessed a sell-off on account of its mixed quarterly guidance. Now Twilio is trying to leverage AI to help boost its growth — but will the adoption of this technology be enough to turn its fortunes around? Let’s find out.

Sluggish customer spending is weighing Twilio down

Twilio reported Q1 revenue of $1.05 billion, an increase of just 4% from the year-ago period. However, the company’s focus on keeping costs in check and its share repurchases led to a much stronger year-over-year growth of 70% in its non-GAAP earnings to $0.80 per share. Twilio’s numbers beat consensus estimates of $0.60 per share in earnings and $1.03 billion in revenue.

However, Twilio’s Q2 revenue guidance range of $1.05 billion to $1.06 billion was lower than the Wall Street estimate of $1.08 billion, and it points toward just 1% to 2% growth from the year-ago period. Twilio is forecasting $0.66 per share in earnings in the current quarter, ahead of the $0.62 per share consensus estimate.

The company’s guidance makes it clear that Twilio is having difficulty attracting more customers, while its existing customers aren’t opening up their wallets either. The company finished Q1 with 313,000 customers, an increase of 4% from the year-ago period. Meanwhile, its dollar-based net expansion rate came in at 102%, a sign of weak customer spending.

The dollar-based net expansion rate compares the spending by Twilio’s customers during a quarter to the spending by those same customers in the year-ago period. A reading of more than 100% suggests that Twilio’s existing customer base either increased its usage of the company’s products or adopted additional services. However, this metric has barely remained above the 100% mark in the past four quarters.

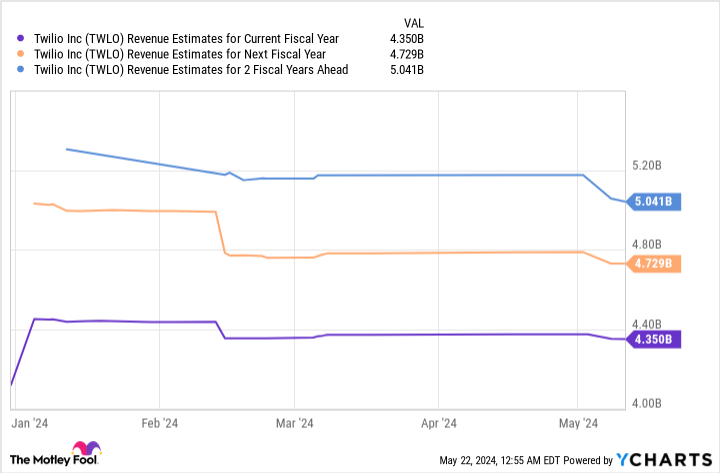

Not surprisingly, analysts are expecting Twilio to finish 2024 with a revenue jump of just 5% to $4.34 billion. The picture for the next couple of years doesn’t seem too bright, either.

TWLO Revenue Estimates for Current Fiscal Year data by YCharts

Analysts have reduced their revenue expectations for 2025 and 2026, as evident from the chart above. However, Twilio is counting on the growing adoption of AI within the cloud communications market to kick-start its growth again.

Counting on AI to fuel growth

Twilio management discussed the company’s AI-specific product development moves at length on the latest earnings conference call. CEO Khozema Shipchandler remarked that Twilio has “made progress on a number of our AI products,” such as its Agent Copilot, which improves the efficiency of customer service agents by providing them “actionable insights for each customer interaction, automating and enhancing agent productivity while reducing resolution times.”

The CEO also added that the adoption of Customer AI — Twilio’s large language model (LLM)-powered customer engagement platform, which uses real-time customer data to help companies deliver more personalized services to customers and drive improvements in sales conversion — is also gaining steam.

The good news for Twilio is that the adoption of AI in the contact center market is set to increase at an annual rate of almost 26% over the next five years, according to Mordor Intelligence. So the company’s growth may pick up the pace in the long run. However, investors should note that Twilio is competing with bigwigs such as Microsoft and Amazon, which have been aggressively rolling out AI-focused services on their cloud computing platforms.

For instance, Microsoft’s Azure Communications Services targets the same market that Twilio caters to. Microsoft’s application programming interfaces (APIs) help its clients connect with their customers through multiple channels such as text, voice, chat, and video. Earlier this year, Microsoft announced that Azure Communications Services can be integrated with its Azure AI services, giving the tech giant’s customers access to the kind of AI-powered customer relationship tools that Twilio is offering.

So it remains to be seen if Twilio can compete with deep-pocketed rivals such as Microsoft and take advantage of the adoption of AI in its end market. That’s why investors would do well to wait for signs of an acceleration in Twilio’s business before thinking of buying the stock.

Of course, Twilio stock is cheap right now, with a price-to-sales ratio of about 2.7 — which is lower than the U.S. technology sector’s sales multiple of 7.3, but a big reason behind that cheap multiple is the company’s tepid growth. If Twilio’s sales fail to pick up on account of weak customer spending and competition from bigger companies, the stock could remain under pressure, which is why investors would do well to avoid Twilio until and unless it steps on the gas.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Microsoft, and Twilio. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.