The last several months have been rough for investors in Super Micro Computer, but better days could be on the horizon.

The developments surrounding Super Micro Computer (SMCI -4.64%) have become some of the most fascinating chapters in the broader artificial intelligence (AI) story.

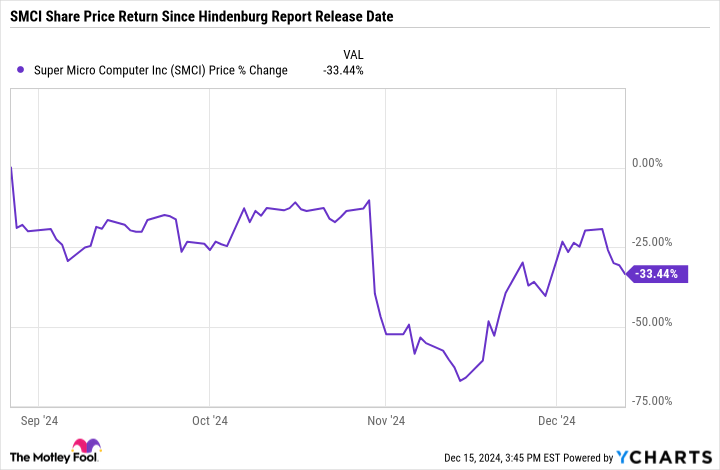

At its peak, shares of Supermicro were up over 300% earlier this year. However, beginning in August, shares entered a prolonged sell-off of epic proportions.

Over the last few months, it’s been a series of falling dominoes for Supermicro. Yet, what if I told you better days could be on the horizon?

I’m going to detail everything that’s happening at Supermicro and explain why the stock entered freefall. More importantly, I’ll also explore why Supermicro could be on the verge of a turnaround, and what that could mean for investors.

Taking a trip down memory lane

There have been so many ongoing storylines at Supermicro over the last few months that’s it’s legitimately difficult to keep up with all the hoopla. Below is an annotated timeline of each road bump Supermicro has encountered, and some details around the stock movement as a result.

- August: In late August, Hindenburg Research published a report alleging accounting malpractice protocols at Supermicro. Within one trading day of Hindenburg’s report becoming public knowledge, shares of Supermicro cratered by 19%. This was the first domino to fall. Exactly one day after the Hindenburg report was released, Supermicro filed an 8K announcing that the company “expects to file a Notification of Late Filing” for its 10K annual report.

- September: About a month after the Hindenburg piece, The Wall Street Journal reported that the Department of Justice (DOJ) was investigating Supermicro over its accounting controls, following a series of allegations touted by whistleblowers. The committees at the Nasdaq stock exchange also sent Supermicro a notice explaining that the company was at risk of being delisted from the exchange due to compliance reasons.

- October: On Oct. 30, it was revealed that Big Four accounting specialist Ernst & Young LLP (“EY”) resigned as Supermicro’s auditor.

- November: In mid-November, reports began swirling that Nvidia was re-routing some of its Blackwell order flow away from Supermicro. To add some context here, Supermicro specializes in the architecture for servers and storage clusters that house Nvidia’s graphics processing units (GPUs). Since Blackwell is expected to be a bellwether for Nvidia, Supermicro was well-positioned to benefit from massive tailwinds surrounding these GPUs.

Why better days could be in store for Supermicro

While accounting fraud is a serious allegation, I’d caution investors against hitting the panic button. It’s important to keep in mind that short sellers such as Hindenburg have a vested interest in seeing a stock price decline. Moreover, in light of all these road bumps, Supermicro has taken some respectable steps in order to address the issues head on and right the ship.

In late November, Supermicro announced the appointment of a new auditor firm, BDO USA, P.C. In the same press release, management also shared that the company had submitted a compliance plan to the Nasdaq to avoid delisting.

In early December, investors received positive news as the Nasdaq granted Supermicro’s “request for an exception” to remain listed on the exchange through Feb. 25, 2025. If Supermicro does not file its 10K by then, the company will fall out of compliance again.

Another announcement from earlier this month revolved around a Special Committee formed by Supermicro’s Board of Directors. Per the internal review, the Special Committee “determined that the resignation of the Company’s former registered public accounting firm, Ernst & Young LLP (“EY”) and the conclusions EY stated in its resignation letter were not supported by the facts examined in the Review.”

On the surface, it looks like Supermicro is finally getting some momentum back, and that the proactive steps from management could very well put the company on a path to turn things around.

Image source: Getty Images.

Is Supermicro stock a buy right now?

As the chart below illustrates, Supermicro’s forward price to earnings (P/E) multiple of 12.9 is well off prior intra-year highs and is essentially hovering around a low point. The current valuation picture, combined with some of the positive news outlined above, might cause you to think that Supermicro is an absolute bargain right now.

However, I think jumping to such a conclusion is more aligned with a “pigs get slaughtered” type of mentality.

SMCI PE Ratio (Forward) data by YCharts.

There are a lot of moving variables with Supermicro, and at this point, I think just about any piece of news (positive or negative) could cause the stock to whipsaw.

To me, there are just too many unknowns surrounding Supermicro at the moment. Investing in the stock is akin to throwing a dart at the wall or flipping a coin — it just isn’t for the faint of heart and likely is best avoided for now.