A decade after some of the nation’s largest U.S. banks helped to bring the financial system to its knees, a new kind of “too big to fail” risk may be emerging in a very different corner of the market: index funds.

Three index fund managers currently dominate ownership of shares of publicly traded companies in the U.S., and their control is likely to tighten in coming years, according to a June research report.

Concentrated ownership — what the authors refer to as the “Giant Three scenario” — means investors and policy makers need to keep a careful eye on the role of fund managers in upholding corporate governance, argue authors Lucian Bebchuk of Harvard Law School and Scott Hirst of Boston University in a working paper titled The Specter of the Giant Three.

The rise of so-called passive exchange-traded funds into a multi-trillion-dollar segment of the global financial system is one of the most consequential economic developments of the past 30 years, but some critics fear that the fast-growing industry has gotten too big for its own good.

Notably, Vanguard founder John C. Bogle, often credited with creating the first index fund in the mid 1970s, described the success of index funds as the perhaps the best innovation in modern financial history. But the geometric growth of index funds — which track the performance of products like the S&P 500 index SPX, -0.34% by holding the same securities and at the same proportion — has created unforeseen problems, conferring too much concentrated power among a select few.

“It seems only a matter of time until index mutual funds cross the 50% mark” of corporate ownership, Bogle wrote in a November 2018 op-ed in the Wall Street Journal.

Citing a September 2018 draft paper written by John C. Coates, Bogle said indexing may be reshaping corporate governance, tipping the power to a point where voting power will be “controlled by a small number of individuals.”

Investors have helped to drive the success of index funds because they offer an easy, and often low-cost, way to gain exposure to a diversified pool of assets.

The 50 largest stock ETFs together manage more than $1.8 trillion, the paper’s authors note, and only 7% of the assets in the 50 largest funds are managed by funds other than the Big Three.

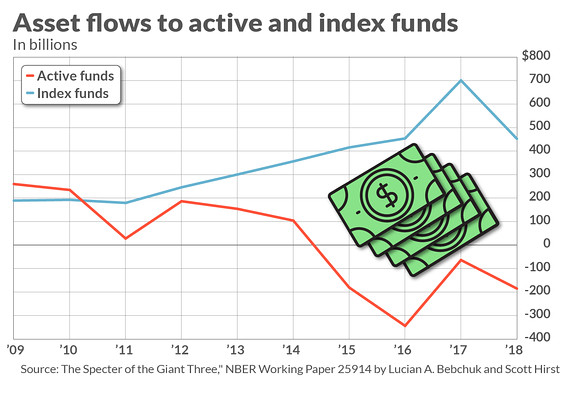

Over the last decade, more than 82% of assets flowing into investment funds, representing over $3 trillion in assets, have gone to the three largest index fund managers: BlackRock Inc. BLK, -0.94% Vanguard, and State Street Global Advisors, the investment arm of State Street Corp. STT, -1.14% Their share of inflows has only intensified over the second half of the decade.

See: How trillion-dollar stock-market index funds are vulnerable to manipulation

The “Big Three” now hold an average stake of more than 20% of companies in the S&P 500, the authors say. Shares that they own represent an average of about 25% of all shares that are voted in corporate elections, since institutional investors are more likely to take an active role in voting than are individuals.

That share could increase to about 34% in the next decade, the authors forecast, and to as much as 41% in two decades.

Related: Harley-Davidson bars media from annual meeting, but can’t hide poor performance

“I do not believe that such concentration would serve the national interest,” Bogle warned in his op-ed.

See also: Companies with unequal voting rights underperform shareholder friendly ones, study finds

“Our work on index fund stewardship focuses on the incentives that the Giant Three will have to be excessively deferential to corporate managers,” Bebchuk and Hirst wrote, adding that market observers and policy makers should prepare for a future in which “checks on corporate managers would be insufficient.”

In his op-ed, Bogle confessed that many of the solutions that have previously been suggested are unpalatable. It may be risky to leave so much voting power in the hands of institutional investors, he wrote, but corporate stock owners at least “care about the long term,” while smaller investors may not.

Still, he suggested, it’s time for federal legislation to make it clear that directors of index funds, and other large money managers, “have a fiduciary duty to vote solely in the interest of the funds’ shareholders.” It’s also time, he said, for national policies “that support high standards of governance,” to be determined by all kinds of stakeholders, including markets participants, academia, and politicians.

Read: Opinion: Tesla, Facebook and 3 others are the most undemocratic stocks on Wall Street