With people on the move again, it’s time for investors to take a closer look at ride sharing, an increasingly popular way to get around.

“There’s pent-up demand to see family and friends. Offices, restaurants and bars are reopening. And even airports are seeing improved traffic,” Uber Technologies Inc. UBER, -1.03% CEO Dara Khosrowshahi said earlier this month.

We already see this change in the numbers. Ride volumes at Uber and Lyft Inc. LYFT, +0.69% grew each month in the first quarter, with March showing the steepest recovery, points out J.P. Morgan analyst Doug Anmuth.

“We expect there is still much more to come,” Lyft CEO Logan Green said earlier this month.

Besides reopening, both companies are plays on this big-picture trend: Less interest in car ownership, in favor of ride sharing. That’s because ride sharing “offers the appeal of more flexibility at a lower cost than traditional car ownership,” says Green.

Both Uber and Lyft will benefit. But let’s look at some key metrics to see which one may benefit more.

Key metrics

Relative size and sales growth

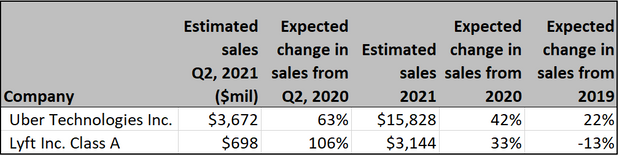

As economies reopen, both companies will show robust growth. But Uber seems to have an advantage. Uber sales are expected by analysts to grow 42% this year compared to last year, according to consensus estimates. Lyft is expected to increase sales by 33%.

Now let’s zoom out for a broader view, skipping over 2020 and next year, to compare 2019 to 2023. Anmuth at J.P. Morgan expects Uber sales to go up 104% to $132.7 billion in 2023 from $65 billion in 2019. Lyft sales will rise 50% to $5.4 billion in 2023 from 2019 sales of $3.6 billion, he predicts. Again, Uber seems to have the edge.

Next, the sales data show that Uber is much bigger. In fact, Uber is the largest on-demand ride-sharing provider in the world (outside of China). Analysts expect Uber to post $3.6 billion in sales for the second quarter, compared to $698 million at Lyft.

Size matters because of the network effect. As the number of drivers increases, the quality of service improves, which attracts more users, which attracts more drivers, and so forth. Uber’s size also means it has more user data, which is valuable as a tool for growing sales. This also helps it gain market share. Uber already has about 30% global market share and it will continue to gain share in the U.S. and globally, says Deutsche Bank analyst Lloyd Walmsley.

But there is plenty of room for both companies to grow because the ride-share market is worth about $452 billion in annual sales (ex-China), says Morningstar analyst Ali Mogharabi.

Cash and free cash flow

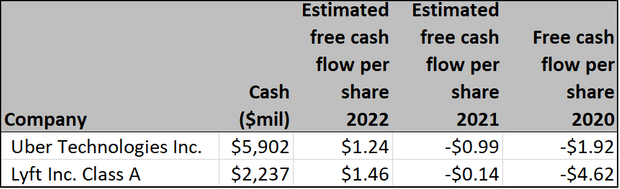

As the numbers above demonstrate, both companies are expected to see big improvement in cash flow this year and next. But Lyft will post a bigger swing, according to analyst estimates, and it will produce more cash flow per share next year. Lyft has the advantage in cash flow growth.

Both companies hold a lot of debt — $9.8 billion at Uber and $1 billion at Lyft. But they each have lots of ready cash as well, or $5.9 billion at Uber and $2.2 billion at Lyft. Cash and growing cash flow are important because they give the companies more freedom by reducing dependence on the capital markets.

Diversification

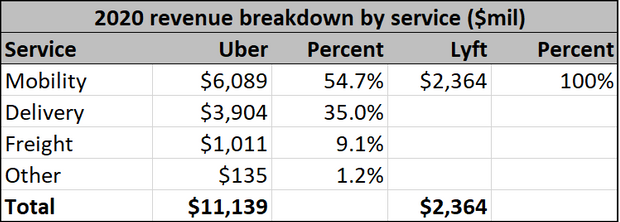

Besides rides, Uber offers food delivery via Uber Eats and freight-shipping services for businesses. It’s also expanding into grocery, convenience store, and alcohol delivery, notes Anmuth. Uber has over 700,000 restaurant partners. Uber Eats accounts for 6% of gross bookings, and the company projects big growth over the next five years.

“The potential remains enormous,” Khosrowshahi has said. So far, at least, reopening has not hit food delivery too hard.

In contrast, Lyft is only in ride share. It’s not in food delivery or logistics.

The broader diversification gives Uber an edge because it has more avenues for growth. It also makes it more attractive for drivers to work with Uber, since they have the fallback of food delivery on the same platform when ride demand declines. And there are benefits of cross-selling to customers.

The bottom line: In diversification, Uber seems to have the edge.

International reach

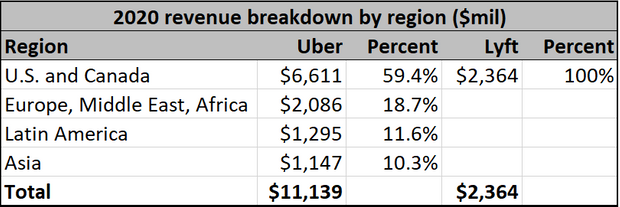

Uber also has much better international reach. This matters because during economic rebounds, many foreign economies grow faster than the economy in the U.S. Uber is in more than 70 countries — mainly in the U.S. and Canada but also in Latin America, Europe, the Middle East, Africa and Asia. It gets 30%-35% of its revenue from outside North America. Lyft serves fewer riders in part because it is focusing mainly on the U.S. market. Here again, Uber has the advantage.

Lyft says it may expand its international offerings, and Lyft bulls might argue that the lack of an international presence merely creates an opportunity for bigger growth than at Uber, which has already rolled out its service abroad.

Valuation

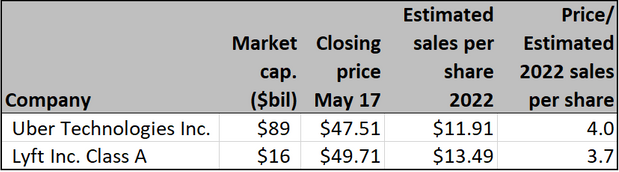

Lyft looks cheaper, based on forward price-to-sales estimates (see above).

But by Morningstar’s “fair value” analysis, Uber looks cheaper. Uber trades 40% below Morningstar’s estimated fair value of $67 per share. Lyft trades 21% below Morningstar’s estimated fair value of $61. At Morningstar, “fair value” means where the stock should trade now based on expected medium-term earnings growth.

Both companies look cheap, relative to other tech companies. For example, J.P. Morgan analyst Anmuth has year-end price targets for Uber of $74 and $72 for Lyft. That’s only around five times its 2022 sales estimates, compared to eight times for their internet marketplace peers, he says.

Next, growth-oriented tech companies like Alphabet Inc. GOOGL, -0.56%, Amazon.com Inc. AMZN, -1.37%, Apple Inc. AAPL, -1.48%, Facebook Inc. FB, -0.75%, Netflix Inc. NFLX, -0.75%, DoorDash Inc. DASH, +0.42% and Etsy Inc. ETSY, -2.78% trade for current price-to-sales ratios of five to 10 or higher. This suggests Uber and Lyft shares could be a lot higher in two years, given that these two ride-share companies trade for 3.7 to 4 times expected 2022 sales now.

Analysts’ opinion

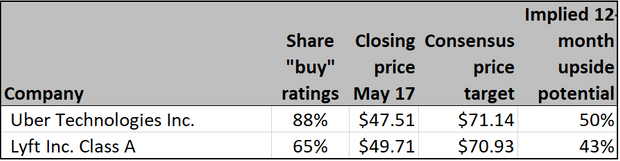

The majority of Wall Street analysts are bullish on these two ride-share companies. That’s a positive. The analyst skew favors Lyft, since there are more analysts remaining to turn positive and drive clients into the stock. One-year price targets — which aren’t always accurate, of course — suggest gains of 50% for Uber and 43% gains for Lyft over the next 12 months.

“Lyft remains a Top Pick in 2021, and as a pure-play ride-share business, our favorite recovery idea,” says Anmuth. He has an “overweight” rating on Uber.

Challenges

The biggest near-term problem for both companies is a shortage of drivers. But higher prices are offsetting that to some degree. The decline of COVID-19 and the increasing vaccination rate will help improve driver availability. So will company incentives, and the decline in generous federal subsidies to unemployed workers in September.

“Once the disincentive of enhanced unemployment benefits expires in early September, drivers will respond quickly,” says Deutsche Bank analyst Lloyd Walmsley, who has a “buy” rating on the stocks.

Medium-term, both companies face public policy risks, or the forced reclassification of gig workers as full-time employees.

“We think they are more than priced-in at current levels,” says Mogharabi at Morningstar.

Michael Brush is a columnist for MarketWatch. At the time of publication, he had no positions in any stocks mentioned in this column. His stock newsletter is Brush Up on Stocks. Follow him on Twitter @mbrushstocks.