Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you’d have done very well indeed. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So should Cronos Group (TSE:CRON) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let’s start with an examination of the business’ cash, relative to its cash burn.

View our latest analysis for Cronos Group

When Might Cronos Group Run Out Of Money?

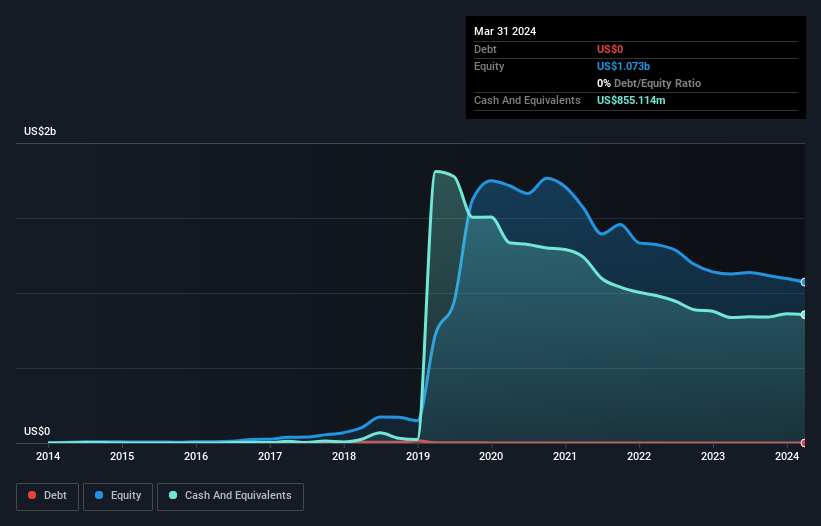

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. In March 2024, Cronos Group had US$855m in cash, and was debt-free. In the last year, its cash burn was US$2.0m. That means it had a cash runway of very many years as of March 2024. Importantly, though, analysts think that Cronos Group will reach cashflow breakeven before then. In that case, it may never reach the end of its cash runway. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Cronos Group Growing?

Given our focus on Cronos Group’s cash burn, we’re delighted to see that it reduced its cash burn by a nifty 98%. And it could also show revenue growth of 11% in the same period. It seems to be growing nicely. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Cronos Group To Raise More Cash For Growth?

We are certainly impressed with the progress Cronos Group has made over the last year, but it is also worth considering how costly it would be if it wanted to raise more cash to fund faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company’s cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year’s operations.

Since it has a market capitalisation of US$986m, Cronos Group’s US$2.0m in cash burn equates to about 0.2% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

So, Should We Worry About Cronos Group’s Cash Burn?

As you can probably tell by now, we’re not too worried about Cronos Group’s cash burn. For example, we think its cash burn reduction suggests that the company is on a good path. On this analysis its revenue growth was its weakest feature, but we are not concerned about it. There’s no doubt that shareholders can take a lot of heart from the fact that analysts are forecasting it will reach breakeven before too long. After considering a range of factors in this article, we’re pretty relaxed about its cash burn, since the company seems to be in a good position to continue to fund its growth. While we always like to monitor cash burn for early stage companies, qualitative factors such as the CEO pay can also shed light on the situation. Click here to see free what the Cronos Group CEO is paid..

Of course Cronos Group may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.