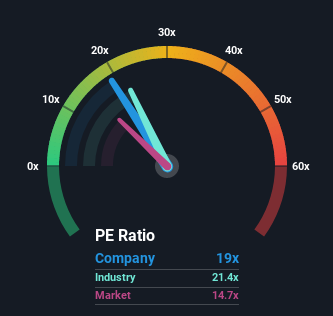

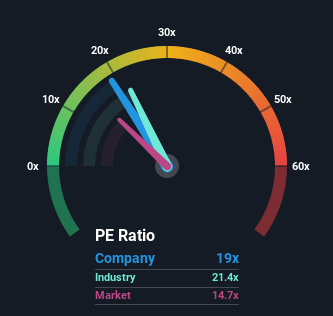

When close to half the companies in the United States have price-to-earnings ratios (or “P/E’s”) below 14x, you may consider Alphabet Inc. (NASDAQ:GOOGL) as a stock to potentially avoid with its 19x P/E ratio. Nonetheless, we’d need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

While the market has experienced earnings growth lately, Alphabet’s earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Alphabet

Want the full picture on analyst estimates for the company? Then our free report on Alphabet will help you uncover what’s on the horizon.

How Is Alphabet’s Growth Trending?

Alphabet’s P/E ratio would be typical for a company that’s expected to deliver solid growth, and importantly, perform better than the market.

Retrospectively, the last year delivered a frustrating 3.2% decrease to the company’s bottom line. Even so, admirably EPS has lifted 120% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 11% each year over the next three years. With the market only predicted to deliver 9.0% each year, the company is positioned for a stronger earnings result.

With this information, we can see why Alphabet is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We’ve established that Alphabet maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn’t great enough to justify a lower P/E ratio. It’s hard to see the share price falling strongly in the near future under these circumstances.

A lot of potential risks can sit within a company’s balance sheet. You can assess many of the main risks through our free balance sheet analysis for Alphabet with six simple checks.

If these risks are making you reconsider your opinion on Alphabet, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here