This sports-centric streaming television company just faces a few too many hurdles, not the least of which is its limited marketing firepower resulting from its small size.

On the surface streaming-TV outfit fuboTV (FUBO -1.11%) looks like a winner. Conventional cable television is expensive, but streaming this same programming via a broadband connection is a more affordable alternative.

Each of Fubo’s pricing plans also offers access to more sports channels than you’ll typically get with traditional cable companies like Comcast‘s (NASDAQ: CMCSA) Xfinity or Charter‘s (NASDAQ: CHTR) Spectrum, tapping into one the top reasons consumers continue paying sky-high cable bills.

Despite its obvious marketability and a few competitive advantages, however, this live-streaming service also faces serious challenges. It’s possible — perhaps even likely — its stock isn’t going to be any higher in five years than it is now.

What the heck is fuboTV anyway?

It may seemingly compete with cable in the sense that it offers the same live network broadcasts, live sports, and other cable programming, but it’s distinctly different. Namely, in the same way that Disney‘s (NYSE: DIS) Hulu+Live and Alphabet‘s (NASDAQ: GOOG) (NASDAQ: GOOGL) YouTube TV do, Fubo digitally streams cable television’s usual programs using that subscriber’s existing broadband connection.

It also offers access to on-demand video, akin to Netflix (NASDAQ: NFLX) or Warner Bros. Discovery‘s (NASDAQ: WBD) Max (albeit it on a smaller scale than either). Notably, while there are clear similarities, fuboTV is not regulated by the FCC (Federal Communications Commission) as a cable company, helping to keep its costs down.

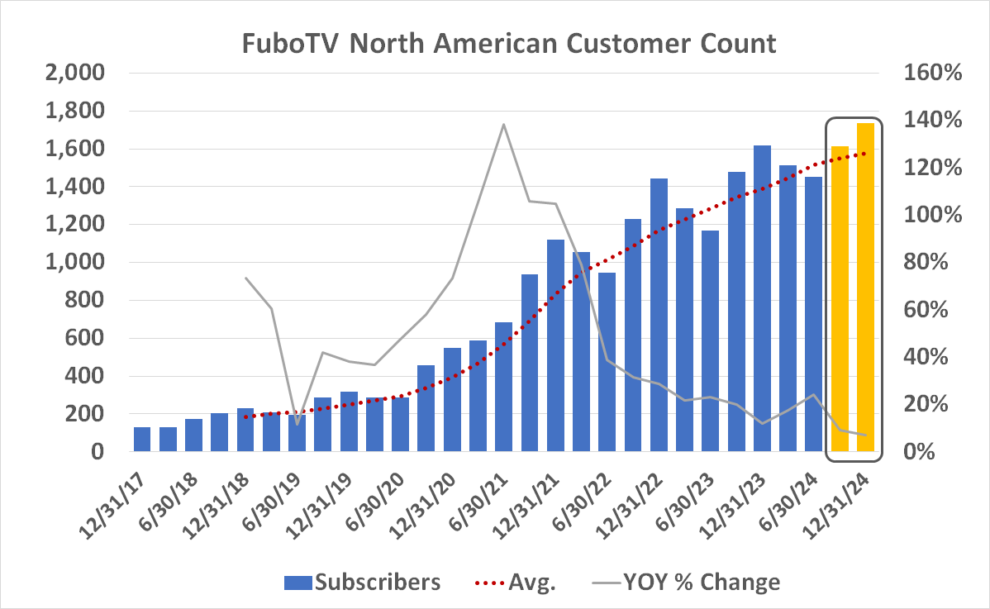

The sports-centric platform now serves over 1.8 million subscribers, 1.45 million of which are paying an average of $85.69 per month for access to its streaming alternative to cable television. (The other 400,000 “Rest of World” customers are only paying $7.02 for much-skinnier plans, leaving the company’s core service as the dominant breadwinner.)

Last quarter’s year over year customer-headcount growth of 24% for its flagship service accounted for most of fuboTV’s top-line growth of 26%, extending established trends.

The loss is shrinking too, from a little over $54 million in the second quarter of last year to a loss of just under $29 million for the three-month stretch ending in June.

Based on this current trajectory, the company’s still anticipating profitability at some point in the coming year. And, maybe it will work its way out of the red and into the black by then.

There are simply some risks here, however, that investors are underestimating.

Four concerns too big to ignore

The first of these risks is slowing subscriber growth.

Although last quarter’s 24% is impressive, it’s also well below fuboTV’s growth pace from just a couple years back. Moreover, it’s likely to continue slowing.

Within its second-quarter report, the company indicated that subscriber growth for its cable-television alternative would likely slow to only 9% (year over year) for the quarter currently underway, before slowing again to a pace of only around 7% during the final quarter of the year. Both would be the worst subscriber growth rates seen since the company as we know it launched. Meanwhile, the company’s “Rest of World” customer count isn’t projected to grow at all through the end of this year.

Data source: Fubo Inc. Chart by author. Customer-count figures are in thousands.

The prospect of being undercut also looms large.

You may already know that Fubo recently won a legal battle against ESPN parent Walt Disney, Fox (NASDAQ: FOX) (NASDAQ: FOXA), and Warner Bros. Discovery, preventing the trio from jointly launching a sports-only live streaming service — called Venu — that was priced at only $43 per month. FuboTV feared the offering could poach as many as 400,000 paying customers from its sports-focused service.

Now take a closer look at the details of the ruling. The injunction is being appealed, meaning Fubo could still soon be competing head-to-head with the powerhouse joint venture.

But even if Venu is successfully blocked, read between the lines. Something else like Venu remains a distinct possibility, even if each of these three studios and sports broadcasters are simply forced to launch their own stand-alone sports-streaming service. Any such platform poses at least some degree of threat to fuboTV, and the more there are, the bigger the collective threat.

Would-be investors will also want to know that while the company is paying down its debt, that effort is coming at a steep price for shareholders. Fubo also continues to issue new shares of itself in droves to pay its bills, diluting existing shareholders’ stakes as a result. Even if-and-when the organization swings to a profit there’s no assurance it won’t continue doing this as a means of funding growth.

FUBO Shares Outstanding data by YCharts

Finally, although it’s not currently considered a cable TV name and therefore not regulated as one, never say never. The FCC is entertaining the prospect, recognizing that at the time current rules were created digital streaming of video didn’t exist. If that happens, fuboTV’s operating costs will almost certainly increase, forcing it to price its service on par with conventional cable companies’ pricing plans.

Too much uncertainty for most portfolios

It’s not all bad. As was noted, fuboTV is inching toward profitability. Scale is helping, as is more cost-effective spending. Higher-margin ad revenue is growing particularly well, up 14% last quarter alone. It’s conceivable that the company could get and remain in the black.

The chances of Fubo ever truly thriving, however, still seem too slim for most investors to take the risk.

See, this company’s still competing directly against players with much deeper pockets — names like Alphabet or Disney — that aren’t necessarily in any hurry to see their live-streaming platforms turn a profit. fuboTV doesn’t have that luxury.

It also doesn’t have their scale. Hulu+Live boasts 4.4 million paying customers, for perspective, while Alphabet says there are now on the order of 8 million subscribers to its YouTube TV service. At the same time Fubo’s indirectly competing with entrenched cable television outfits like Charter’s Spectrum and Comcast’s Xfinity, both of which enjoy more marketing muscle and existing reach.

The best-possible five-year outcome here? In my opinion, maybe an acquisition of fuboTV by a larger media or tech company that believes it can do more with the young sports-minded streaming television brand. Unfortunately, even if that were to happen there’s no assurance it would happen at a compelling price above this stock’s current one.

Bottom line? Investors should consider shopping for lower-risk, higher-odds opportunities.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. James Brumley has positions in Alphabet and Warner Bros. Discovery. The Motley Fool has positions in and recommends Alphabet, Netflix, Walt Disney, Warner Bros. Discovery, and fuboTV. The Motley Fool recommends Comcast. The Motley Fool has a disclosure policy.