The company is putting up strong growth, but is weighed down by poor profit figures.

Roku (ROKU 2.53%) is a peculiar company. It is a streaming TV platform, a sector littered by big technology companies with close to unlimited budgets. And yet, Roku is the market share leader in the United States and increasingly growing in international markets such as Mexico. The company had no right to win in streaming, but today has 85.5 million streaming TV households playing 32 billion video hours a quarter.

The stock has not reflected this remarkable market dominance. Shares are actually down 57% in the past five years, likely due to investor skepticism around the platform’s profitability (or lack thereof). However, the past does not equal the future. Roku’s business keeps growing, and now its stock is trading at some of its cheapest levels in years.

Does that bode well for shareholders over the next five years? Time to dig into the numbers and find out.

Still riding the streaming TV transition

From a sector standpoint, Roku still has plenty of tailwinds at its back. According to Nielsen, streaming video still only accounts for 41% of TV viewing in the United States. Eventually, this number will get close to 100% in 10 to 20 years.

Of all TV watching in the United States, Roku accounts for a high portion of it. Historically, most of this viewing was on third-party streaming services such as Netflix.

Today, Roku has built up its own free streaming application called the Roku Channel, and it now has a 1.6% share of all TV watching in the United States. According to management, the Roku Channel is the third most popular application on the Roku platform, which makes sense, seeing these market share numbers and the fact that the application is not available anywhere but Roku. Roku Channel streaming hours grew 80% year over year last quarter.

More watching hours — especially on the Roku Channel — should lead to more top-line growth for Roku. And it has. Last quarter, Roku’s platform revenue grew 15% year over year to $908.2 million. This segment comes with high gross margins of 54.2% and is mainly driven by advertisements and promotional spending across Roku systems.

Steadily improving margins

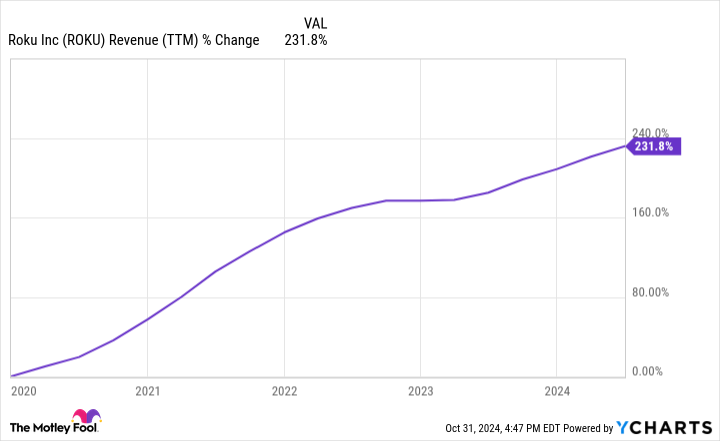

In the last five years, while Roku’s stock is down close to 60%, revenue has grown by a cumulative 232%. Top-line growth is not an issue with Roku — it is more the underlying profitability of its operations.

Operating income was -$600 million over the past 12 months and has been negative for multiple years now. However, in the last few quarters it has shown progress in improving its operating margin. In Q3, operating margin was -3%, which is close to break-even from a profitability standpoint.

Investors should look closely at Roku’s operating margin over the next few years. If it can keep growing revenue while expanding margins, the company will finally start generating a boatload of bottom-line profits.

ROKU Revenue (TTM) data by YCharts

Where will the stock be in five years?

Profit margin uncertainty will tell the story for Roku stock over the next five years. Revenue growth should take care of itself, given the tailwind in streaming around the world and its dominance in households across North America and Mexico.

Total revenue grew 16% year over year last quarter. I think 10% annual revenue growth is doable for Roku in the next five years. That would bring annual revenue to $6 billion five years hence.

But what will profit margins be? Given its consolidated gross margin of 45%, I think Roku will likely get toward 10% bottom-line profit margins once it reaches a larger scale. On $6 billion in revenue, that equates to $600 million in annual earnings.

Today, Roku stock trades at a market cap of $9 billion, which is a five-year forward price-to-earnings ratio (P/E) of 15. While cheap, it is not that much lower than the long-term market average. Unless Roku’s stock trades at a premium earnings ratio in five years, the stock won’t be much higher in five years based on these estimates.

Unless you think Roku can grow revenue faster than 10% annually or can expand profit margins to much higher than 10%, there is no reason to buy this stock. Forward returns don’t look promising over the next five years.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Netflix and Roku. The Motley Fool has a disclosure policy.