First published on Simply Wall St News

NVIDIA Corporation (NASDAQ:NVDA) has made 94% returns from a year ago, and 438% from three years ago. While the company is growing, investors wonder if the stock has further upside. In this article, we will compare the market valuation with the current and future earnings for NVIDIA, and see if potential earnings match the value.

NVIDIA’s P/E

With a price-to-earnings (or “P/E”) ratio of 63.5x NVIDIA may be sending very bearish signals at the moment, given that the semiconductor industry trades at about 25.7x earnings, while almost half of all companies in the United States have P/E ratios under 16x and even P/E’s lower than 9x are not unusual.

In general, there are two reasons for a high P/E ratio. One, that investors expect much higher earnings in the future, and the second, that the stock is overpriced.

One possible reason for this increase in price is the FED’s 2021 monetary policy, whereby increasing the money supply, they effectively devalued the dollar, leading to massive spikes in stocks (especially tech). If investors adopt this theory, then stocks are effectively in decline from their 2020 valuation relative to the US dollar.

View our latest analysis for NVIDIA

Keen to find out how analysts think NVIDIA’s future stacks up against the industry? In that case, our free report is a great place to start.

How Is NVIDIA’s Growth Trending?

In order to justify its P/E ratio, NVIDIA needs to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered an exceptional 123% gain to the company’s bottom line. EPS has also lifted 129% in aggregate from three years ago, thanks to the last 12 months of growth.

Accordingly, this has probably resulted in increased shareholder enthusiasm.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 21% per annum over the next three years. That’s shaping up to be materially higher than the 11% each year growth forecast for the broader market.

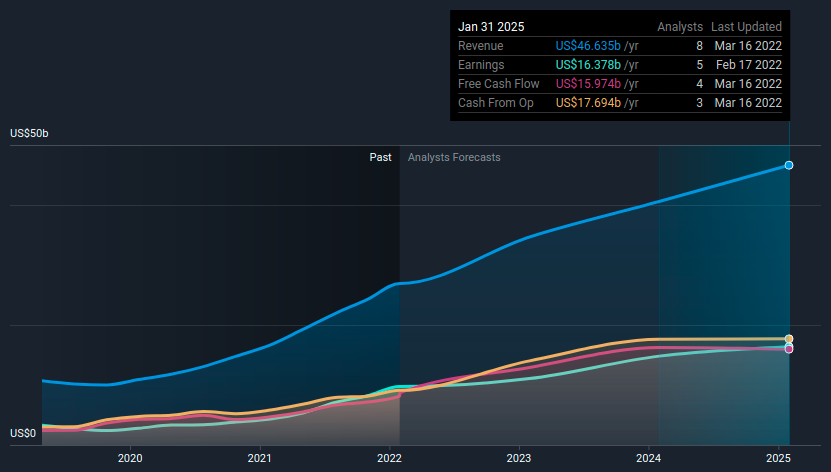

We can see what analysts expect in the chart below:

We see that analysts expect NVIDIA to reach US$46.6b in revenue, as well as US$16.4b in Earnings. By using these metrics, we can construct forward pricing estimates.

The forward P/E ratio for 2025 is 37x. This is still well above the industry median of 25.7x and implies that NVIDIA has to markedly increase future performance in order to justify the price. Additionally, forward earnings imply that investors will have to wait years before the earnings converge on the price – This may mean that they are losing on other opportunities elsewhere.

Reversing the math, in order for NVIDIA to justify the current price, the company would eventually have to post US$24b in earnings, a 144% increase in the income from today.

If we want to get a bit more specific, NVIDIA has to post US$48b earnings in 10 years in order to justify a present value (discounted at 7.5%) of US$612.4b at the industry 25.7x P/E today.

For investors that think that the company can attain that level of earnings in 10 years, the stock price is justified – which may very well be the case.

Pessimistic investors, on the other hand, will want to factor-in external factors and consumer demand saturation as arguments for an unrealistic valuation.

Key Takeaways

In order for NVIDIA to justify its current price, it needs to post US$24b in a few years, or US$48b in 10 years.

The current price is likely a mix between the increased performance of the company and 2021 FED monetary policy, which injected large amounts of cash that ended up in stocks – mostly technology.

The current 64x P/E is quite high, but dropped from 79x in 2021, indicating that either enthusiasm of financial liquidity is falling.

Before you settle on your opinion, we’ve discovered 1 warning sign for NVIDIA that you should be aware of.

It’s important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20x).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.