(Bloomberg Opinion) — Apple Inc. is no stranger to causing sticker shock with its newest products. It’s about to find out whether it can create a similar reaction among U.S. corporate-bond buyers with its latest debt offering.

The technology giant is taking the rare step of issuing dollar bonds for the second time in the same calendar year. When Apple borrowed $8.5 billion in May, the 10-year portion priced at a yield that was 110 basis points more than benchmark U.S. Treasuries. The 10-year part of the new deal is being marketed at a spread of 75 basis points and seems destined to tighten from there. The average yield spread on double-A corporate bonds has narrowed by more than 50 basis points since Apple’s last offering, Bloomberg Barclays index data show, suggesting the iPhone maker could lock in a 10-year rate around 1.25%. To put that in context: Before this year, the U.S. government itself had never borrowed so cheaply.

At this point, few superlatives are left to describe the relentless rally in investment-grade bonds. As Bloomberg News’s Molly Smith reported, companies from Amazon.com Inc. and Google parent Alphabet Inc. to Visa Inc. and Chevron Corp. have all set record-low interest rates across the corporate yield curve. Chevron’s two-year debt priced with a 0.333% coupon; Amazon’s three-year securities offered 0.4%; and Visa’s seven-year bonds offered 0.75%, outdoing Alphabet’s 0.8%.

Apple’s all-in borrowing costs probably won’t be lower than those of Alphabet, which timed its deal perfectly and sold debt just before Treasury yields increased by the most in two months. But the fact that the iPhone maker is piling into a market already grappling with never-before-seen interest rates might be enough to start causing investors to bristle, particularly given the recent wave of encouraging economic data, such as U.S. initial jobless claims falling below 1 million for the first time since the coronavirus pandemic took hold. In theory, such a rebound would lead traders to rotate into riskier assets.

Then again, it’s not as if investors are shunning equities or high-yield bonds. Junk-rated Ball Corp., an aluminum-packaging company, issued $1.3 billion of 10-year securities at 2.875% earlier this week, the lowest ever for a U.S. speculative-grade deal with a maturity that long. Meanwhile, like much of the technology sector, Apple’s stock price is almost 40% higher than it was in February. The company plans to use debt proceeds at least in part to buy back shares and pay dividends.

The Federal Reserve is the elephant in the room, of course, even if Chair Jerome Powell has specifically said the central bank doesn’t intend to “run through the bond market like an elephant.” Its Secondary Market Corporate Credit Facility has bought $55 million in Apple debt across eight separate securities, according to a disclosure of purchases through July 29.(1) In the grand scheme of things, that’s not all that much, given that companies have sold almost $2 trillion of bonds and leveraged loans just this year. But the backstop effect matters just about as much as the actual amount it owns. As I wrote last month, given the company’s tendency to use the money it raises to conduct share buybacks, it’s not quite the Fed buoying Apple stock, but it’s awfully close.

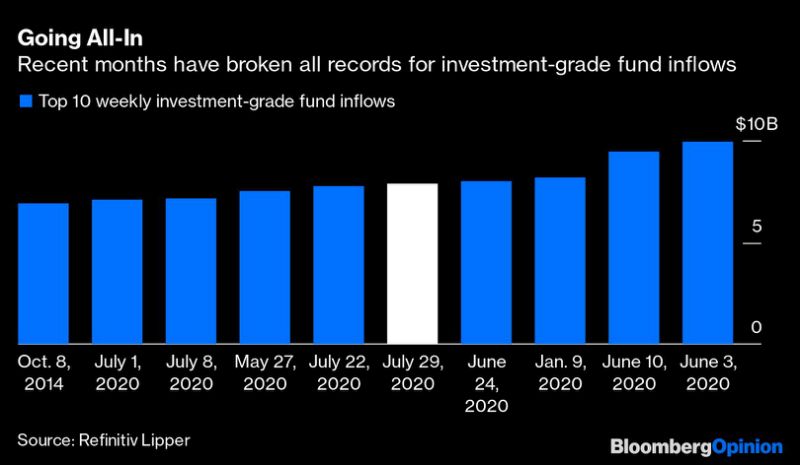

More important, the Fed’s facility creates the perception that there’s virtually no risk in holding investment-grade U.S. corporate bonds — it’s practically free money as long as it offers any sort of yield pickup relative to Treasuries. That’s why investment-grade bond funds have experienced consecutive weekly inflows over the past four months that collectively have exceeded $100 billion. Eight of the 10 largest inflows in history have have come during this streak:

I was asked on Bloomberg Radio earlier this week if there was an asset class I thought had run too far, too fast. It’s a tough question for anyone when gold prices soared above $2,000 an ounce and the S&P 500 Index exceeded its record close in just 175 days. I flagged investment-grade corporate bonds simply because these type of one-way flows make me nervous, given their propensity to create both virtuous and vicious cycles. I see the arguments for why there’s more room to run — remarkably, average corporate-bond spreads are still 39 basis points wider than their tightest levels from the past decade — and wouldn’t necessarily bet on the credit rally fizzling out, let alone sharply reversing its gains.

But at a certain point, investors in any asset class need to pause and take a breather. That process might not begin with Apple, but its bond sale is bound to splash yet another jarring interest rate across trading screens.

(1) For those interested, the specific CUSIPs are: 037833DV9, 037833AR1, 037833AK6, 037833CG3, 037833CM0, 037833DL1, 037833DT4, 037833BS8.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com/opinion” data-reactid=”48″>For more articles like this, please visit us at bloomberg.com/opinion

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”49″>Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.