This AI stock has delivered impressive gains in 2024, and it could pop higher following its upcoming quarterly report.

Artificial intelligence (AI) has played a central role in lifting semiconductor stocks over the past couple of years, which is evident from the tremendous 131% spike in the PHLX Semiconductor Sector index during this period. The good part is that the proliferation of this technology is set to drive stronger growth in this market, as AI adoption moves from data centers to edge devices such as smartphones, personal computers (PCs), and automotive applications, among others.

For instance, the market for chips used in smartphones is expected to jump from $104 billion in 2023 to $146 billion next year. PC semiconductor spending, on the other hand, could jump to $107 billion in 2025 from $89 billion last year, while automotive market chip spending is forecast to jump to $104 billion next year from $79 billion last year. Meanwhile, spending on semiconductors deployed in AI servers and data centers is set to jump from $78 billion in 2023 to $136 billion next year.

For investors looking to capitalize on all these fast-growing semiconductor end markets that have received a big boost thanks to AI, Taiwan Semiconductor Manufacturing (TSM 2.71%), popularly known as TSMC, seems like an ideal bet.

The foundry giant serves all the verticals discussed, and the latest news from the company reinforces the fact that AI is turning out to be a solid growth driver for the company. Let’s look at the reasons why.

TSMC is on track to deliver yet another terrific quarterly report

TSMC has just released its sales data for September, and the company has reported an impressive year-over-year increase of almost 40% in its monthly revenue to 251.8 billion New Taiwan (NT) Dollars. If we add the monthly revenue for July, August, and September, TSMC’s Q3 revenue would come in at almost 760 billion NT Dollars, an impressive jump of 39% from the same period last year.

That number is higher than analysts’ Q3 revenue estimates of 748 billion NT Dollars. So, TSMC seems set to exceed Wall Street’s expectations when it releases its third-quarter results on Oct. 17. Analysts have been forecasting $1.80 per share in earnings from the company, a jump of 40% from the same period last year, but the better-than-expected revenue growth is likely to translate into stronger bottom-line gains.

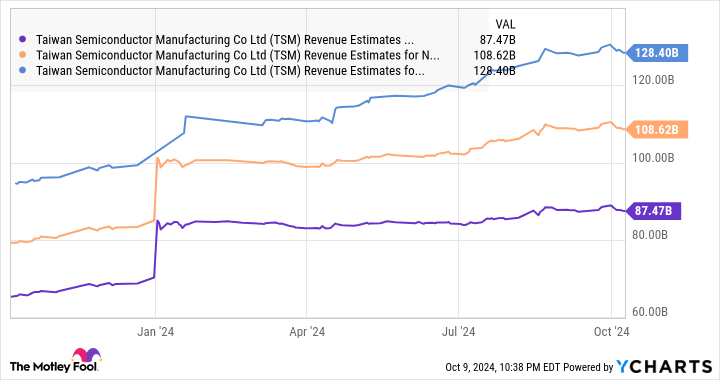

Another thing worth noting is that TSMC’s revenue in the first nine months of 2024 increased by 32% from the same period last year. This means TSMC is well on course to outpace the 26% revenue growth to $87.2 billion that analysts are expecting the company to deliver in 2024. More importantly, TSMC is expected to sustain healthy growth levels over the next couple of years as well.

TSM Revenue Estimates for Current Fiscal Year data by YCharts

However, don’t be surprised to see TSMC’s revenue growth outpacing Wall Street’s expectations. That’s because the company is one of the most important pick-and-shovel plays in the massive AI space. It manufactures and fabricates chips for a range of fabless chipmakers such as Nvidia, AMD, Qualcomm, Broadcom, and Marvell Technology.

Even better, chipmakers with fabrication plants of their own, such as Intel, are also turning to TSMC to capitalize on the latter’s advanced chip manufacturing processes to produce more efficient, powerful chips. But that’s not where TSMC’s AI-related opportunity ends. The company also manufactures chips for Apple, putting it in position to make the most of the growth in AI smartphone sales.

Now, a closer look at the customers discussed will make it clear that TSMC is one of the best ways to play the AI chip boom in different sectors. Nvidia, AMD, and Intel, for instance, are trying to make the most of the opportunities available in AI accelerators. Nvidia is running away with this market right now, making chips using TSMC’s process nodes to deliver faster performance and lower power consumption than rivals.

Qualcomm, AMD, and Intel are present in the AI-enabled PC market. Similarly, Qualcomm and Apple present avenues through which TSMC can tap the smartphone space. And finally, Marvell and Broadcom allow TSMC to tap into another fast-growing niche of AI semiconductors in the form of custom AI chips. Simply stated, it doesn’t matter which of these companies wins more market share and ends up dominating their respective niches — TSMC is most likely going to be the ultimate winner.

That’s why TSMC’s advanced packaging technology that’s used for producing AI chips is sold out until 2025. As a result, the company is expanding its capacity to produce AI chips a year ahead of the original schedule, according to Morgan Stanley. This should ideally allow TSMC to make more chips, fulfill more orders, and deliver stronger growth in revenue and earnings.

Buying the stock before Oct. 17 is a no-brainer

This discussion makes it clear that TSMC is carrying terrific momentum going into its Q3 earnings report that’s due on Oct. 17. There is a strong chance that it will beat consensus estimates and also deliver stronger-than-expected guidance for Q4, all of which could give the stock a nice shot in the arm.

TSMC stock has jumped 77% this year already, and it looks all set to end the year on a strong note. Given that this AI stock is trading at an attractive 22 times forward earnings even after its outstanding run this year, buying it looks like a no-brainer right now considering that it seems built for more upside.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom, Intel, and Marvell Technology and recommends the following options: short November 2024 $24 calls on Intel. The Motley Fool has a disclosure policy.