(Bloomberg) — Tech mavericks who made buy-now-pay-later an option for shoppers worldwide are grappling with mounting losses and investor skepticism. Now big finance is on their tail.

Most Read from Bloomberg

British retail giants NatWest Group Plc, HSBC Holdings Plc, Barclays Plc and Virgin Money as well as Visa Inc. and Mastercard Inc. have recently launched new ways to spread the cost of purchases as they cater to the gradual shift from credit cards to the kinds of services offered by newcomers Klarna Bank AB, Affirm Holdings Inc. and Afterpay.

“Even though banks are just getting started, they are well positioned to scale fast,” said Dilnisin Bayel, a managing director who specializes in credit in Europe at Accenture Plc. “Although the concept of paying in installments is more than a century old, the real-time delivery of BNPL on any card is new and convenient for users. Banks have an opportunity to put their unique stamp on the offer.”

This growing competition adds to pressure on buy-now-pay-later providers, which allow customers to split online purchases via their own apps or an extra button on retailers’ checkout pages. After several years of rapid growth, rising borrowing costs risk eroding their margins just as soaring inflation makes credit more tempting — and more dangerous — for many customers across Europe and the US.

And investors, who viewed Klarna as more valuable than some of Europe’s banks last year, are rethinking their enthusiasm. Klarna’s latest fundraising in July slashed its valuation to $6.7 billion from $45.6 billion, while in the US, Affirm’s market capitalization has dropped more than 70% this year to $8.4 billion.

Traditional credit providers tend to have more funding and longstanding relationships with millions of customers, giving them a headstart in challenging the newcomers. They also have experience of the sort of regulatory clampdown that’s on the horizon for BNPL in the UK and elsewhere, with large firms encouraging stricter rules in future, to the chagrin of some startups.

There’s lucrative business at stake: Barclays, for example, made £541 million, or about 16% of its UK income, from its Barclaycard UK consumer lending arm in the first half of the year. To be sure, it’s smaller than its business lending or mortgage operations, but it would be painful to lose this customer base.

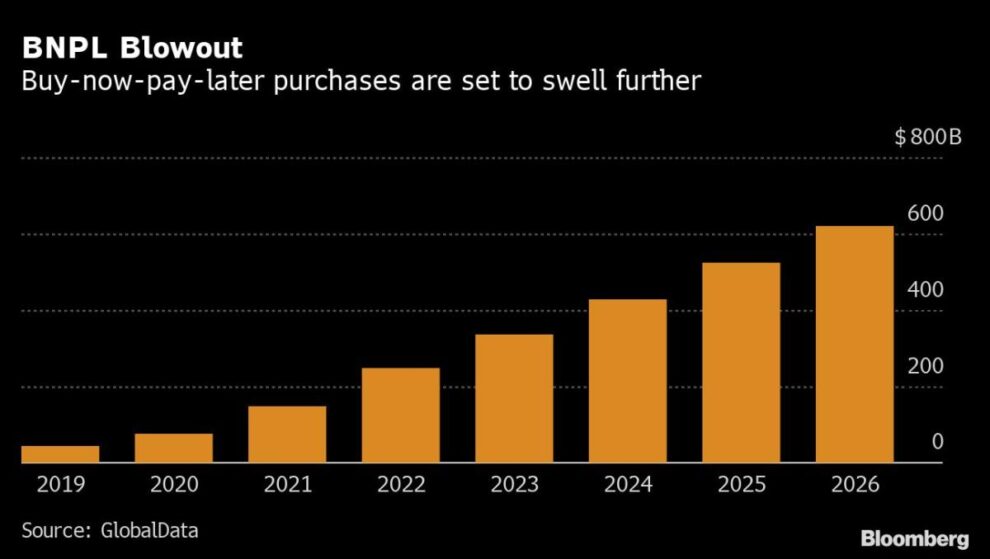

BNPL transactions reached about $147 billion in 2021, nearly doubling in a year to represent about 2.7% of global commerce transactions, according to GlobalData. The data firms believes this has room to rise to about 7.1% of global commerce by 2026. With more providers big and small joining the market, growth looks set to continue “especially in a macro-economic environment with inflationary pressures where consumers need to look for alternative sources of credit to cover living expenses,” said Jeff Tijssen, a partner at Bain & Co.

Bank On It

NatWest said in March it would enable its customers to spread payments over four installments — with no interest if payments are made on time, in line with many BNPL startups. It’s been followed by HSBC and Virgin Money. Barclays, which has offered financing at retail checkouts for years, teamed up with Amazon.com Inc. late last year to provide an installment option with the online marketplace.

Away from the established banks, fintechs Monzo and Revolut both have products in this space while Apple announced in June it will offer payments in four installments within its digital wallet, in partnership with Goldman Sachs Group Inc.

Also in the fray is payments giant PayPal Holdings Inc., which launched “Pay in 4” in August 2020, offering to spread the cost at 0% interest for purchases over £99. About 22 million consumers have now used the service globally.

BNPL is the fastest-growing online payment method in many economies, helped by the pandemic-era shift to internet shopping and new generations of tech-savvy customers, according to Patricia Partelow, managing director at EY’s financial services consulting business. On Tiktok and Instagram, influencers share referral codes and show off their shopping hauls bought entirely with BNPL credit.

“The rising popularity of BNPL also creates another risk for banks — losing access to millennial and Gen Z consumers attracted to this alternative form of financing,” Partelow wrote in an online post.

Yet as rates continue rising, both big lenders and new firms funded by venture capital will be tested and stressed, analysts believe. The latest plunge in fintech valuations means banks are also considering acquisitions to grow in this space, according to Mike Abbott, Accenture’s global banking lead. “This could be an opportunity for liability-rich banks to improve their long-term return on equity, balance their lending portfolios and reduce dependency on commercial (often real-estate-heavy) lending,” he said.

What Bloomberg Intelligence Says

Fintech and payments companies globally continue to face reality with share prices and private equity valuations rebasing lower, accelerated by a race to the bottom for margins in the heavily competitive space. As the need for cost cuts and slowdown in investment temper expectations, the relative performance and valuation hit of differing business models is increasingly stark.

Jonathan Tyce, BI banking analyst

Regulators, like banks, are playing catch-up. Under new rules planned in the UK, lenders would need to check loans are affordable for consumers and make sure advertisements are not misleading. Providers will also need approval from the Financial Conduct Authority — though regulation is unlikely before mid-2023.

Banks are used to the regulatory scrutiny that new providers are facing for the first time. “We’ve made it part of our lending criteria,” NatWest Chief Executive Officer Alison Rose said as she talked about BNPL in July. “We treat it almost as if it’s a regulated product because I think it’s about making sure it’s responsible lending.”

But this long track record with borrowers can also be seen as a drawback, if the banks use these relationships to encourage unaffordable borrowing, said Stella Creasy, a Labour MP who campaigned against payday lenders such as Wonga, which collapsed in 2018 after tighter regulations were introduced.

“At the moment it feels like what they are doing is getting people to put their expenses on overdraft without calling it an overdraft, without letting them know what the risks of taking on this form of credit is, what the consequences could be,” she said.

Most Read from Bloomberg Businessweek

©2022 Bloomberg L.P.