U.S. companies that use nonstandard numbers to calculate executive compensation are overpaying their top managers, according to a new research report.

The working paper, “High Non-GAAP Earnings Predict Abnormally High CEO Pay,” by Nicholas Guest of Cornell University’s Samuel Curtis Johnson Graduate School of Management and S.P. Kothari and Robert Pozen at the Massachusetts Institute of Technology’s Sloan School of Management, finds that non-GAAP earnings, or those that do not conform with Generally Accepted Accounting Principles, exhibit a significantly positive relationship to CEO pay.

The study is based on GAAP and non-GAAP earnings and compensation data for S&P 500 SPX, +0.66% companies from 2010 to 2015.

“We hypothesize that large, positive differences between non-GAAP and GAAP earnings are associated with excessive CEO compensation,” the researchers wrote. ”That is, the compensation committee of the board of directors behaves as if large, positive non-GAAP adjustments to GAAP earnings warrant high levels of compensation.”

‘GAAP metrics are unreliable enough, so using non-GAAP metrics for compensation is really horrifying. This is a classic case of shoot the arrow at the wall and draw a target around it.’

For shareholders, that’s bad news, as it means managers are being compensated at unjustifiably high levels, in some cases even when the company is losing money.

Nell Minow, vice chairwoman at the corporate-governance advisory firm ValueEdge Advisors, said shareholders should be paying close attention to this trend.

“GAAP metrics are unreliable enough, so using non-GAAP metrics for compensation is really horrifying,” she said. “This is a classic case of shoot the arrow at the wall and draw a target around it.”

See: Disney heiress: Jesus Christ himself doesn’t deserve this much money

SEC rules require companies to report quarterly, annual or current financial numbers under GAAP. They are allowed to supplement those numbers with non-GAAP metrics, but they must give the standard GAAP numbers equal or greater prominence in their reporting and follow other SEC guidelines.

Many companies, for example, calculate EBITDA, or earnings before interest, taxes, depreciation and amortization, as a way to remove those costs. Some even offer an adjusted EBITDA number, which removes even more items, and can turn a loss into what looks like a profit. Non-GAAP earnings exceed GAAP earnings by an average of 23%, the report found.

For more than 20 years, market participants and regulators have been in a tug-of-war over these non-GAAP metrics, which are also described as “adjusted” or “pro forma” by some companies.

From the mid-1990s to early 2000s, these metrics were unregulated and found primarily in a few industries. After the accounting scandals of the early 2000s, including the one that caused the collapse of energy giant Enron, Congress passed the Sarbanes-Oxley Act in 2002. That act included a provision called Regulation G requiring companies to reconcile their alternative earnings numbers to the most directly comparable GAAP number.

By 2016, the use of non-GAAP metrics had become widespread again, prompting the SEC to issue updated guidelines that reminded companies of the rules. The SEC followed up with comment letters to the worst offenders, but companies still tried to find ways around the rules, as MarketWatch has reported in the past.

Read: ADT fined by SEC for skirting reporting guidelines

Of note: ADT is still using nonstandard metrics that turn its loss into a tidy profit

Also read: Blue Apron skirts standard-accounting rules to claim profitability

Companies typically argue that non-GAAP metrics are a better indicator of economic reality, or underlying performance, and they say they reflect the factors that are under their control in a way that GAAP earnings do not. But if that was the case, and “managers’ motivation were truly to help investors identify persistent performance,” then executives would consistently exclude items with positive and negative impact, the Cornell and MIT researchers wrote. However, other research has found that the majority of exclusions and adjustments are for items with negative impacts on earnings.

Read: Study: Earnings surprises are bigger, thanks to growing use of non-GAAP metrics

See also: Equifax wipes away cyber-breach charges to claim an earnings beat

The result is that executives often get bonuses even when a company has been reporting a GAAP loss for multiple quarters. In 2014-15, for example, about 28%, or $16.5 million, of overall CEO pay of $58 million at the botox maker Allergan Inc. AGN, -0.06% was granted for meeting non-GAAP earnings targets — the company had a net loss in that period.

The researchers told MarketWatch that 24% of the companies in their sample with the largest positive non-GAAP adjustments based them on negative GAAP net income.

Some companies were repeat offenders in adjusting GAAP losses to profits to achieve executive-compensation targets: for example, Vertex Pharmaceuticals Inc.’s VRTX, -1.26% reported losses that were converted to executive-compensation paydays via non-GAAP adjustments in 2013, 2014 and 2015. Salesforce.com Inc. CRM, -0.01% reported losses every year from 2011 through 2015, and yet its CEO compensation exceeded the study’s model for expected compensation by more than $5 million each year.

Read: Revlon shares slide 6.9% after report of material weakness in financial controls

In some instances, if the adjusted earnings number is not big enough to meet and beat bonus targets, the metrics are redefined annually, sometimes by just enough to clear a threshold. If the minimum or midpoint is not enough, the non-GAAP metric can be tweaked again by just enough to meet the maximum bonus target.

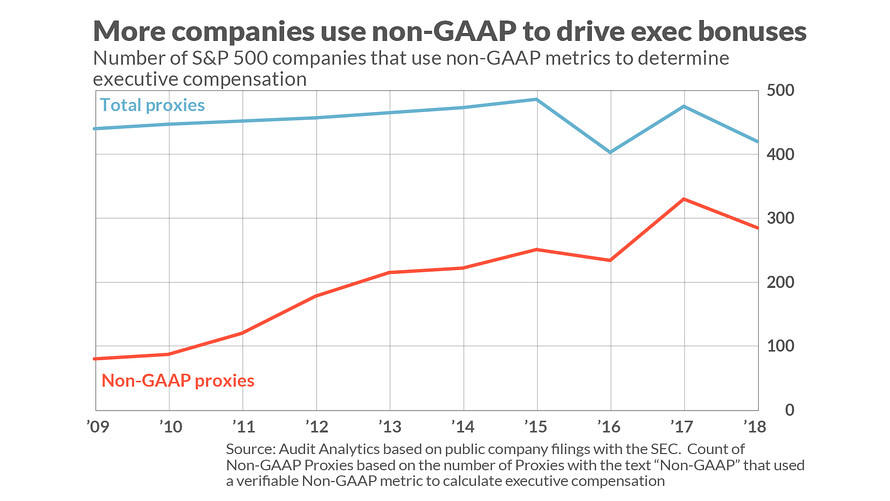

Research firm Audit Analytics estimates that nearly two-thirds of S&P 500 companies use non-GAAP metrics for compensation purposes.

“There is no requirement to reconcile metrics used for compensation purposes with GAAP, which complicates the analysis,” Olga Usvyatsky, vice president of research for Audit Analytics, told MarketWatch. “Other challenges to analysts and researchers are a lack of consistency and mislabeling.”

MarketWatch analyzed public companies’ recent use of metrics that adjust GAAP net income in earnings announcements and when calculating executive bonuses. Audit Analytics provided the raw data from 10-Ks and annual proxies filed with the SEC at the end of 2018.

MarketWatch’s analysis focused on companies that used non-GAAP metrics to convert net losses to income and to meet executive bonus targets, in 2018, often after adjusting the standard numbers again.

| Company | Ticker symbol | GAAP earnings $ | Earnings-release non-GAAP earnings $ | Bonus-calculation non-GAAP earnings $ | “Minimum” executive bonus earnings target $ | Proxy target executive bonus earnings $ | “Maximum” executive bonus earnings target $ |

| General Motors Inc. | GM, +0.97% | -3,864 | 12,844 | 12,800 | 6,800 | 12,700 | 14,000 |

| Transocean LTD | RIG, -0.23% | -3.097 | 1,218 | 1,420 | 1,180 | 1,360 | 1,540 |

| NRG Energy | NRG, -0.33% | -1.548 | 2,373 | 2,494 | 1,824 | 2,608 | 2,871 |

| EBay Inc. | EBAY, -0.41% | -1,012 | 2,163 | 2,170 | 2,030 | 2,130 | 2,300 |

| Tenet Healthcare Corp. | THC, -1.99% | -704 | 2,444 | 2,049 | 2,044 | 2,168 | 2,291 |

| Sempra Energy | SRE, +1.37% | 256 | 1,368 | 1,377 | 1,231 | 1,282 | 1,332 |

| Nasdaq Inc. | NDAQ, +0.88% | 999 | 1,148 | 1,196 | 1,116.7 | 1,186 | 1,231.7 |

| Best Buy Co. Inc. | BBY, -0.55% | 1,764 | 1.634 | 1,950 | 1,741 | 1,831 | 2,011 |

| Waste Management Inc. | WM, +1.21% | 2,636 | 4,006 | 4,007 | 3,713 | 3,965 | 4,084 |

| United Technologies Corp. | UTX, +1.87% | 4,552 | 5,315 | 5,300 | 4,600 | 5,100 | 5,600 |

| Walmart Inc. | WMT, +0.75% | 20,437 | 20,504 | 23,291 | 21,597 | 22,639 | 22,881 |

| Comcast Corp. | CMCSA, +0.63% | 22,714 | 28,062 | 28,100 | 27,370 | 28,009 | 28,230 |

Source: Audit Analytics based on public company filings with the SEC for the full year of 2018. Numbers are in millions.

“Directors should read this important paper,” said Rosanna Landis Weaver, program manager for CEO Pay at the nonprofit As You Sow. “It underlines the need for special vigilance on any non-GAAP figures. I hope this important work focuses directors’ attention on an important subject.”

The SEC adopted rules in 2011 requiring a so-called say-on-pay vote at least once every three years to give shareholders a voice on executive compensation and “golden parachute” compensation arrangements. The new rules were mandated by the post-financial-crisis Dodd-Frank Act and require companies to also disclose the results of the say-on-pay vote in the annual meeting’s proxy statement. Additional disclosure regarding whether, and how, companies consider the results of the shareholder say-on-pay vote is also required.

The MIT professor Pozen said there are companies that survive a say-on-pay vote against their executive compensation, “but they are outliers.” No one, he added, “wants to be in the 5% extreme group” on executive compensation.

So, what’s to be done to stop companies from overpaying underperforming executives?

The researchers suggest that the SEC could require that compensation committees give GAAP metrics “equal prominence” with non-GAAP metrics, exactly as is required in press releases concerning quarterly results.

In particular, they wrote, “the SEC might consider requiring compensation committee reports of all public companies to prominently disclose the amount of difference between the non-GAAP criteria used by the committee and the relevant GAAP numbers and provide a justification for why the committee chose to use non-GAAP criteria in setting executive compensation.”