(Bloomberg Opinion) — The world’s second-largest sovereign wealth fund is playing a dangerous game.

China Investment Corp. aims to have as much of 50% of its portfolio in alternative assets by the end of 2022. That means the $941 billion fund is diving deeper into illiquid investments including real estate, infrastructure, hedge funds and private equity just as such trades are becoming increasingly crowded. CIC will also be diminishing its exposure to public markets that have rebounded strongly this year. For all the jitters over weakening global growth and the trade war, U.S. stocks are nudging record highs again and the MSCI World Index has climbed 17% in 2019.

It’s little wonder that CIC is seeking ways to juice returns. The Beijing-based fund reported a 2.35% loss on overseas investments for last year as global equity markets tumbled, according to results posted Friday. That was the fourth unprofitable year for the international portfolio since CIC’s creation in 2007, when the fund was carved out of China’s then-ballooning foreign exchange reserves.

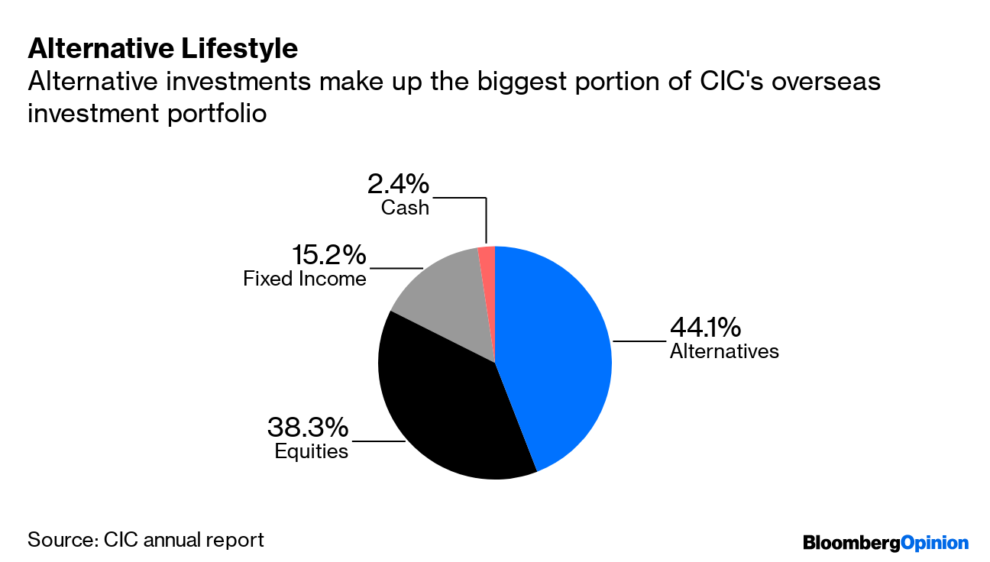

CIC already has the among the highest proportion of investments allocated to alternative assets among state-owned global money managers, according to data from Sovereign Wealth Research, a unit of IE University in Madrid. At the end of December, the ratio stood at 44%, equal to Australia’s Future Fund. Singapore’s GIC Pte had 19% of assets in alternative investments. The share for Norway’s Government Pension Fund Global, or GPFG, was just 3%.

GPFG proposed changes to its mandate last month to allow it to buy stakes in unlisted companies after missing out on investments such as Spotify Technology SA. Norway’s government has repeatedly declined to let the sovereign wealth fund, the world’s biggest, enter the global private equity market because of concerns over transparency and management costs.

Every investor would like to get his or her hands on the next hot unicorn in the hope that it will turn into another Facebook Inc. or Amazon.com Inc. once it goes public. That task isn’t getting any easier, though. The presence of behemoths such as SoftBank Group Corp.’s $100 billion Vision Fund (and a second fund of similar size) have made the competition for lucrative investments more intense. And in any case, unicorn IPOs haven’t been doing so well lately, as my colleague Tim Culpan noted earlier this year.

Three years ago, CIC had 46% of its overseas portfolio in publicly traded equities and 37% in alternatives. By the end of last year, the roles had reversed, with the share in stocks down to 38%. The fund’s international portfolio accounts for 34% of its assets.

The Chinese fund faces hurdles that may impede its goals. CIC has lost key managers over the past two years, undermining the talent pool that’s necessary for successful hedge-fund and private-equity investing. In addition, China’s overseas acquisitions are facing tougher scrutiny amid rising trade tensions with the U.S. Marquee acquisitions such as the $13.8 billion purchase of Blackstone Group LP’s European logistics business Logicor in 2017 are likely to be harder to come by in future.

Chairman Peng Chun struck a gloomy tone in the fund’s annual report, noting that “protectionism and unilateralism will continue to spread, geopolitical conflicts will recur, trade tensions will intensify, global economic momentum will weaken” and international capital markets would become plagued with uncertainties.

CIC has cited volatility for wanting to reduce its exposure to public equity markets. That overlooks the fact that stocks are at least more liquid and easier to exit. There are also questions over the fund’s timing. In 2012, CIC posted losses after the commodities cycle peaked. Back then, bulking up in fixed income would have been a better bet. This move into alternatives may be another ill-timed wager.

To contact the author of this story: Nisha Gopalan at [email protected]

To contact the editor responsible for this story: Matthew Brooker at [email protected]

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com/opinion” data-reactid=”59″>For more articles like this, please visit us at bloomberg.com/opinion

©2019 Bloomberg L.P.