Yields above 5% are difficult for investors to find, as very low interest rates and a bond boom have pushed yields lower.

If your main objective as an investor is to generate income while avoiding stock-market risk, an emerging-markets bond fund may not be what you would ordinarily consider. But the developed world is awash in cash, and debt with negative yields-to-maturity now exceeds $17 trillion, according to Bloomberg. Ten-year U.S. Treasury notes yield only 1.73% TMUBMUSD10Y, -1.90% and 30-year Treasury bonds TMUBMUSD30Y, -1.98% are yielding a measly 2.18%.

So emerging markets beckon, and sufficient diversification may put you at ease. The $517 million TIAA-CREF Emerging Markets Debt Fund TEDLX, -0.50%, which carries a five-star rating (the highest) from research firm Morningstar, held 256 investments as of Aug. 31. Morningstar has the fund’s performance in the ninth percentile among 252 emerging markets funds run by U.S. companies over the past three years, with the percentile ranking improving to five for one year and four for 2019 (through Sept. 24). The fund has been around for five years.

The TIAA-CREF Emerging Markets Debt Fund’s benchmark is the J.P. Morgan Emerging Markets Bond Index (EMBI) Global Diversified. The index is tracked by the $15 billion iShares J.P. Morgan USD Emerging Markets Bond ETF EMB, -0.29%, which makes for an ideal comparison.

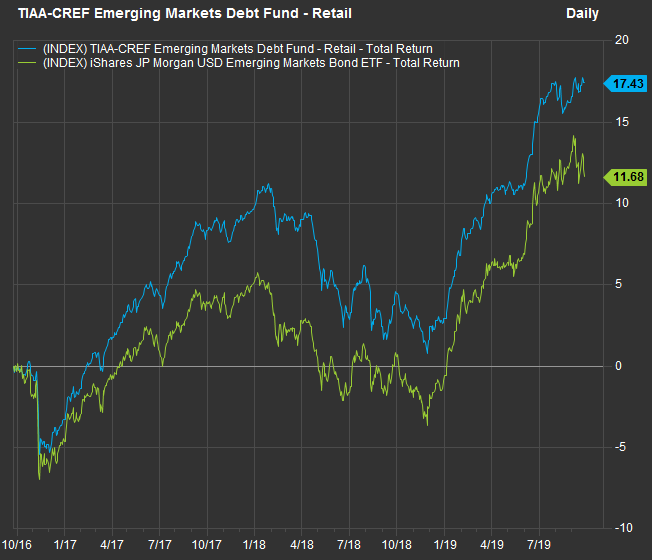

Here’s how the TIAA-CREF Emerging Markets Debt Fund’s total return compares with that of the ETF over the past three years:

FactSet

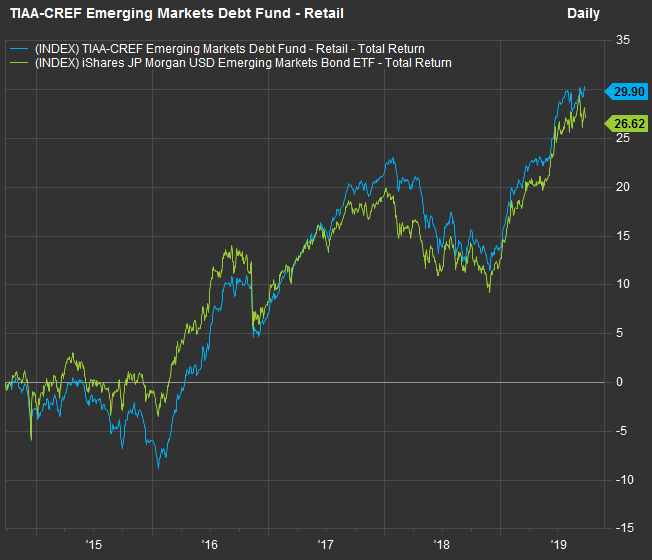

FactSet Here’s a chart showing returns from the fund’s establishment on Sept. 26, 2014, through Sept. 24 of this year:

FactSet

FactSet So the fund’s retail shares have outperformed the ETF significantly, especially over the past three years, despite an annual expense ratio of 0.99% of assets, compared with 0.39% for the ETF. For 12 months through Sept. 24, the fund returned 13.1%, compared with 12.1% for the ETF. Year-to-date through Sept. 24, the fund returned 14.1%, while the ETF was up 12.7%.

The fund has other share classes, with lower expense ratios, available through distribution channels. The retail shares have a $2,500 minimum and no sales charge.

The fund quotes a 30-day yield of 5.08% for the retail shares, with a 12-month distribution yield of 5.71%. These compare to a 30-day yield of 4.29% and a 12-month trailing yield of 5.41% for EMB.

The fund can be considered a high-yield fund, as 59% of the portfolio was in bonds rated below BBB as of June 30. About 56% of the bonds in the ETF are rated BBB or higher.

Reasons for outperformance

Katherine Renfrew and Anupam Damani, the fund’s managers at TIAA subsidiary Nuveen in New York, explained in an interview Sept. 24 how the fund is differentiated from its benchmark index and EMB.

Corporate bonds made up nearly half of the portfolio as of Aug. 31. That’s in sharp contrast to the benchmark index and EMB, which are limited to government securities issued in U.S. dollars in emerging markets. That said, EMB is still diversified, holding about 480 bonds issued by more than 50 countries.

Renfrew focuses on corporate debt, while Damani handles sovereign debt.

Nuveen

Nuveen Renfrew named Petróleo Brasileiro PBR, +0.42% — better known as Petrobras — as an example of a corporate issuer she has been particularly interested in, as Brazil continues to move past the money laundering scandal that came to a head during the administration of former President Dilma Rousseff, who was removed from office in August 2016.

Renfrew also named Fibria Celulose and Suzano Papel e Celulose SUZ, +2.96%, two paper manufacturers, as “very well-established” Brazilian debt issuers of interest. “Brazil is one of the largest countries for issuing corporate debt,” she said.

Brazilian sovereign and corporate debt made up 6.4% of the fund as of June 30, accounting for its highest country exposure.

Active approach

Renfrew stressed that active management can lead to more opportunities for gains on the sale of debt securities previously scooped up at bargain prices.

When discussing Venezuela, where the fund hasn’t been invested since last year, Damani said the fund had profited at times when it purchased the country’s bonds at very low prices.

“One way to think about it was the prices were so low that every coupon payment made up a very large amount of your total return,” she said. “So a lot of investors were just playing the ‘next coupon game.’ ” (Most bonds feature interest payments twice a year.)

Nuveen

Nuveen Damani pointed to new opportunities in frontier countries, especially those that are part of International Monetary Fund programs, “that provide liquidity and policy-support anchors.”

Those include Ukraine, “which has a new government in place with an anticorruption mind-set,” she said. Investments in Ukrainian sovereign or corporate bonds made up 3.4% of the fund’s portfolio as of June 30.

Another frontier country of increasing interest is Pakistan, which also has a new government and has signed on to an IMF agreement under which the country was required to “make the currency more flexible and depreciate it, which they did,” Damani said. Egypt has also “done extremely well under the guidance of the IMF program.”

Citing the IMF’s importance in establishing credibility with investors, Damani named Ecuador, which issued 10-year bonds in June yielding 9.05%.

Renfrew said she and Damani work with a team of 16 analysts to identify credit opportunities and manage risk.

Emphasizing the active nature of their risk-management style, Damani said the portfolio’s annual turnover can be over 100%, although it tends to run between 60% and 80%.

“Over two decades we have seen it all,” Renfrew said. “It is a tricky market. If we have strong views we can exercise them.”

Don’t miss: Index funds may hold more danger than you realize — here’s a way to cut your risk

Create an email alert for Philip van Doorn’s Deep Dive columns here.